Iran, Urea and Wheat

The Snapshot

-

Escalating unrest in Iran threatens urea supply from a country that accounts for around 10% of global trade, lifting fertiliser price risk for Australian growers ahead of seeding.

-

Geopolitical risk alone can drive higher urea prices through insurance, freight and supply-chain disruptions, even without physical production shutdowns.

-

US tariffs on countries trading with Iran could force global buyers into alternative supply pools, increasing competition for the same fertiliser sources Australia relies on.

-

Rising fertiliser prices at this point in the season may pressure input budgets and influence nitrogen application decisions on farm.

-

Any conflict involving Iran could also push oil prices higher via the Strait of Hormuz, potentially providing some upside support for Australian wheat prices.

The Detail

The instability in Iran might feel half a world away, but it could have an impact on Australian grain producers as we head towards seeding.

The streets of Iran are full of protestors, with many reported to have been killed. Donald Trump has just announced a 25% tariff on any country which trade with Iran. The US is looking at military options in the region.

All of this can affect the terms of trade for our farmers.

Fertiliser markets are particularly sensitive to geopolitical shocks because supply chains are highly concentrated and production is capital-intensive. Urea plants cannot be switched on and off quickly, and any disruption to gas supply, labour availability, or export logistics can have an immediate impact on global availability. Australia, as an import-dependent country, means price signals often move well before physical shortages emerge, compressing the decision window for growers and increasing the risk of paying peak prices during critical purchasing periods.

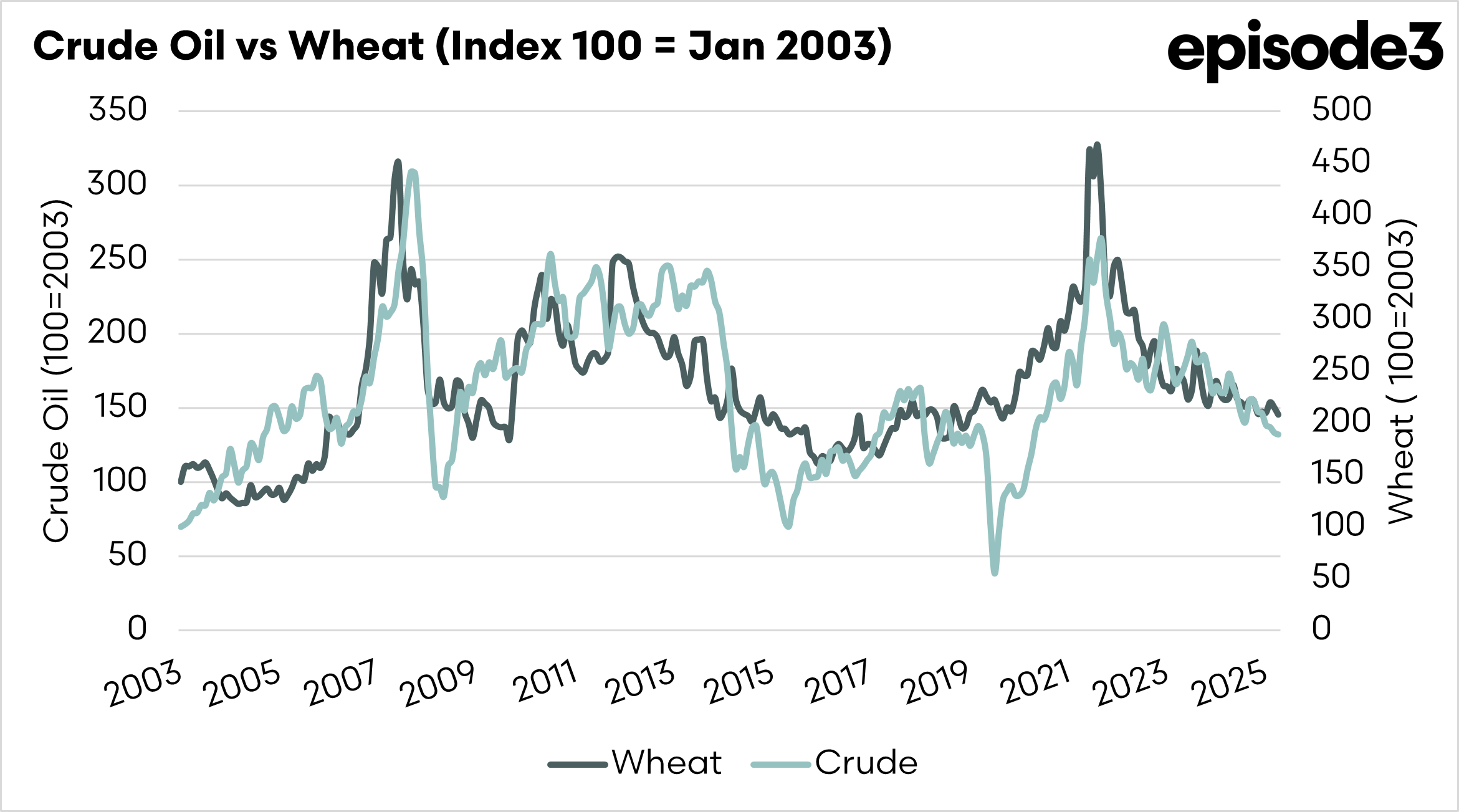

Political instability and riots in Iran could materially affect global urea markets. Iran is a significant urea exporter, accounting for around 10% of global urea trade. If

Escalating unrest raises the risk of plant disruptions, labour shortages, or energy rationing, all of which could curtail output. Even without physical shutdowns, heightened geopolitical risk can restrict exports, raise insurance and freight costs, and slow shipping through the region. Markets tend to price in these risks quickly, meaning urea prices can rise on uncertainty alone, tightening availability for import-dependent countries.

Iranian urea largely serves price-sensitive importing regions, meaning any disruption forces those buyers into the same alternative supply pools that Australia depends on. This creates a cascading effect where relatively small disruptions can trigger price moves as buyers compete for replacement tonnes in a market with limited short-term flexibility.

The Trump tariffs on countries that continue to engage in trade with Iran could also prompt our competitors, who may buy from Iran, to purchase from alternative sources, from which we also purchase. This tariff could effectively curtail the supply of urea from a nation that accounts for around 10% of global trade.

The tariff risk also introduces behavioural changes across global trade flows. Even countries not directly targeted may reduce exposure to Iranian supply to avoid secondary sanctions, compliance risks, or reputational concerns. This can further reduce effective supply, even if the Iranian product remains technically available.

In markets, perception often matters as much as reality, and risk-averse buyers can accelerate tightening conditions simply by stepping back from contested origins.

We don’t have to look far back in history to see the impact of uncertainty in Iran. Last June, there was military action between Israel and Iran, and bombing runs by US forces on Iran.

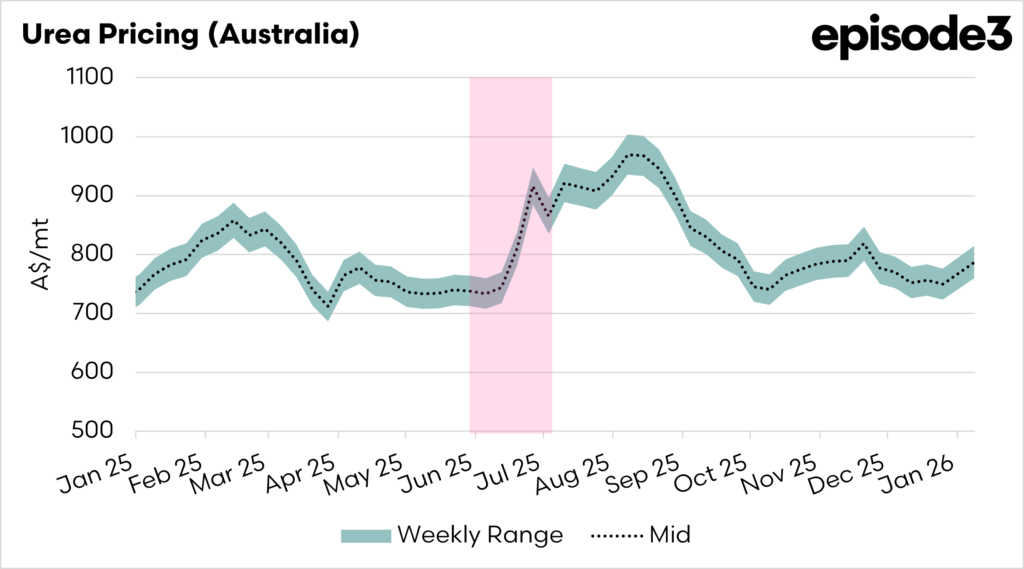

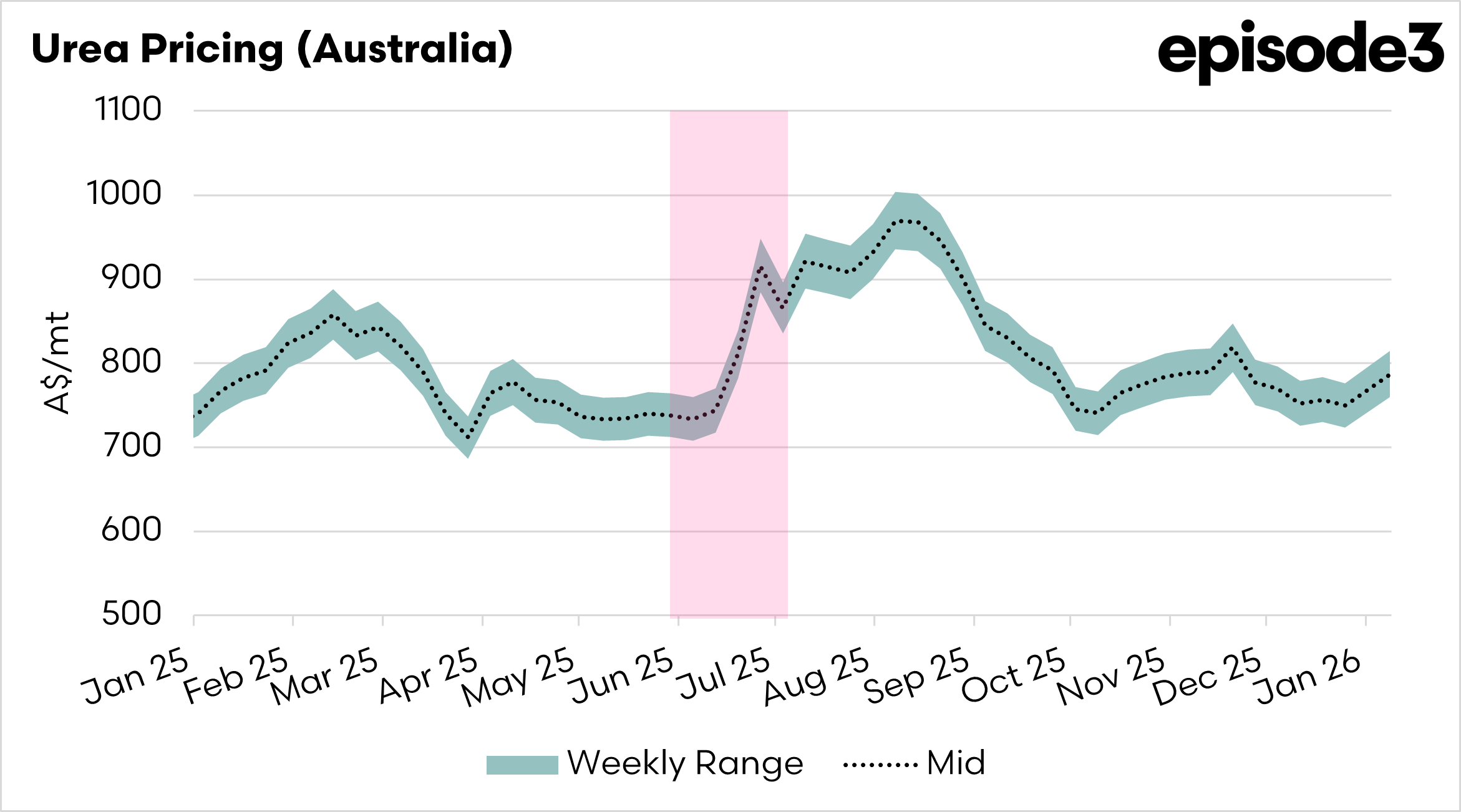

The chart below shows our urea fair pricing model, this is the cost of buying and landing within Australia. I have highlighted the period when events in Iran caused the market to rally, driven by higher energy costs and the curtailment of urea production in the region.

In recent weeks, urea prices have risen due to increased demand from India. If instability in Iran escalates, we could see urea prices rise dramatically.

For Australian growers, the timing of these price movements is particularly challenging. Fertiliser purchasing decisions are being made as geopolitical risk rises, limiting the ability to wait for clarity. Higher prices at this stage of the season can materially affect input budgets, gross margins, and nitrogen application strategies, prompting some producers to reassess rates or timing to manage risk.

The big question will be what happens in Iran. If the government collapses, will the recovery be quick or slow? The longer the recovery, the more the pain.

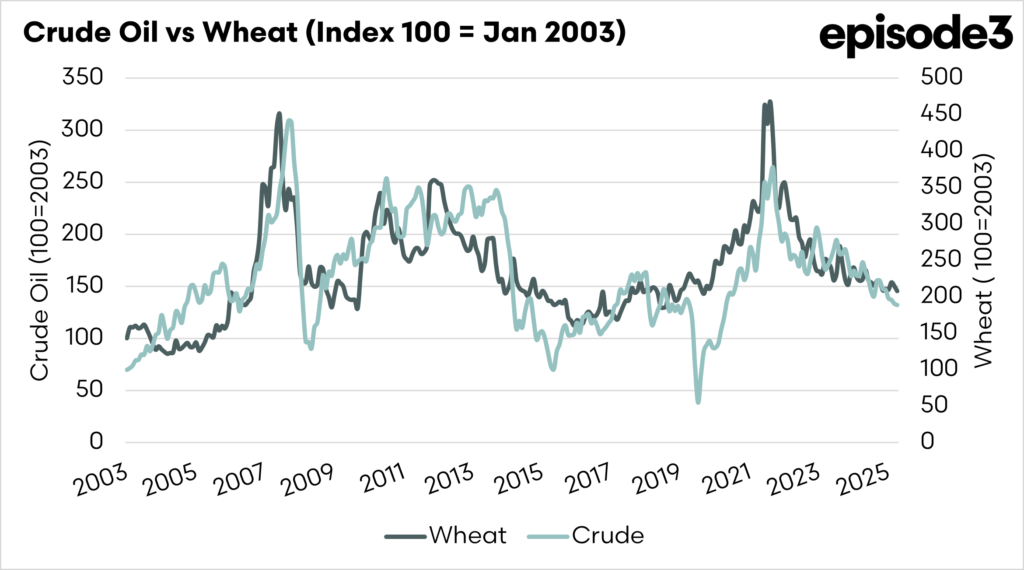

On the flip side, a conflict in Iran could be positive for grain prices. Iran controls the Strait of Hormuz, a shipping lane responsible for nearly 20% of global oil trade.

The market is already reacting, with oil prices hitting seven-week highs due to fears of supply chain risks.

Our wheat pricing tends to be strongly linked to energy markets, so a rise in crude oil prices could positively impact wheat pricing in Australia.

The situation in Iran is evolving, and we need to monitor developments.