A more promising end to 2025 for sheepmeat processors

Sheep Processor Trading Conditions Model

The final months of 2025 delivered a reminder that recovery in sheep processor margins is rarely a straight line. What had looked like a steady improvement through October and November was reshaped once updated export data and December market movements were factored in. The revised figures show that trading conditions in November were not as strong as initially indicated, before a firmer December lifted sentiment again. Even so, the broader takeaway for the year is that processor margins remained under sustained pressure compared with the previous season.

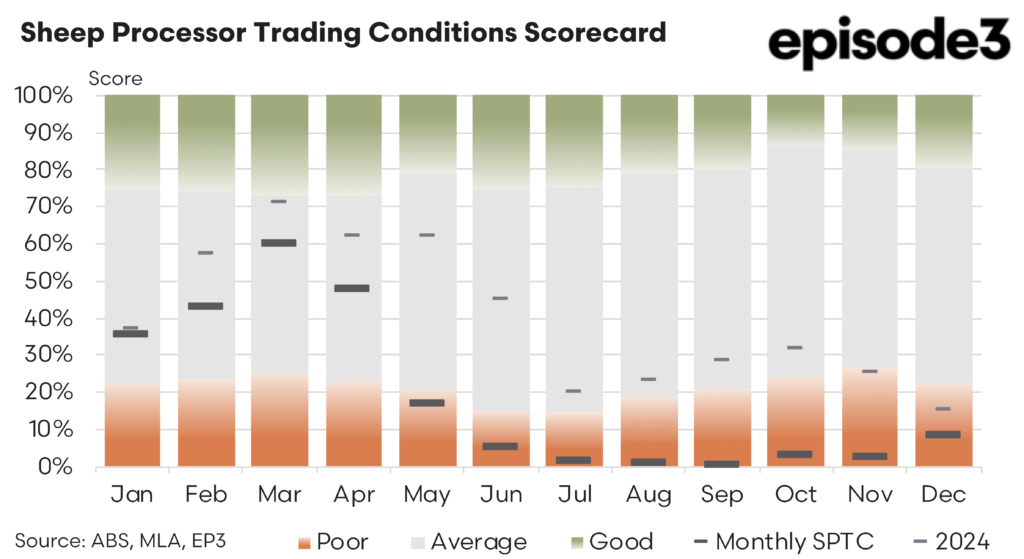

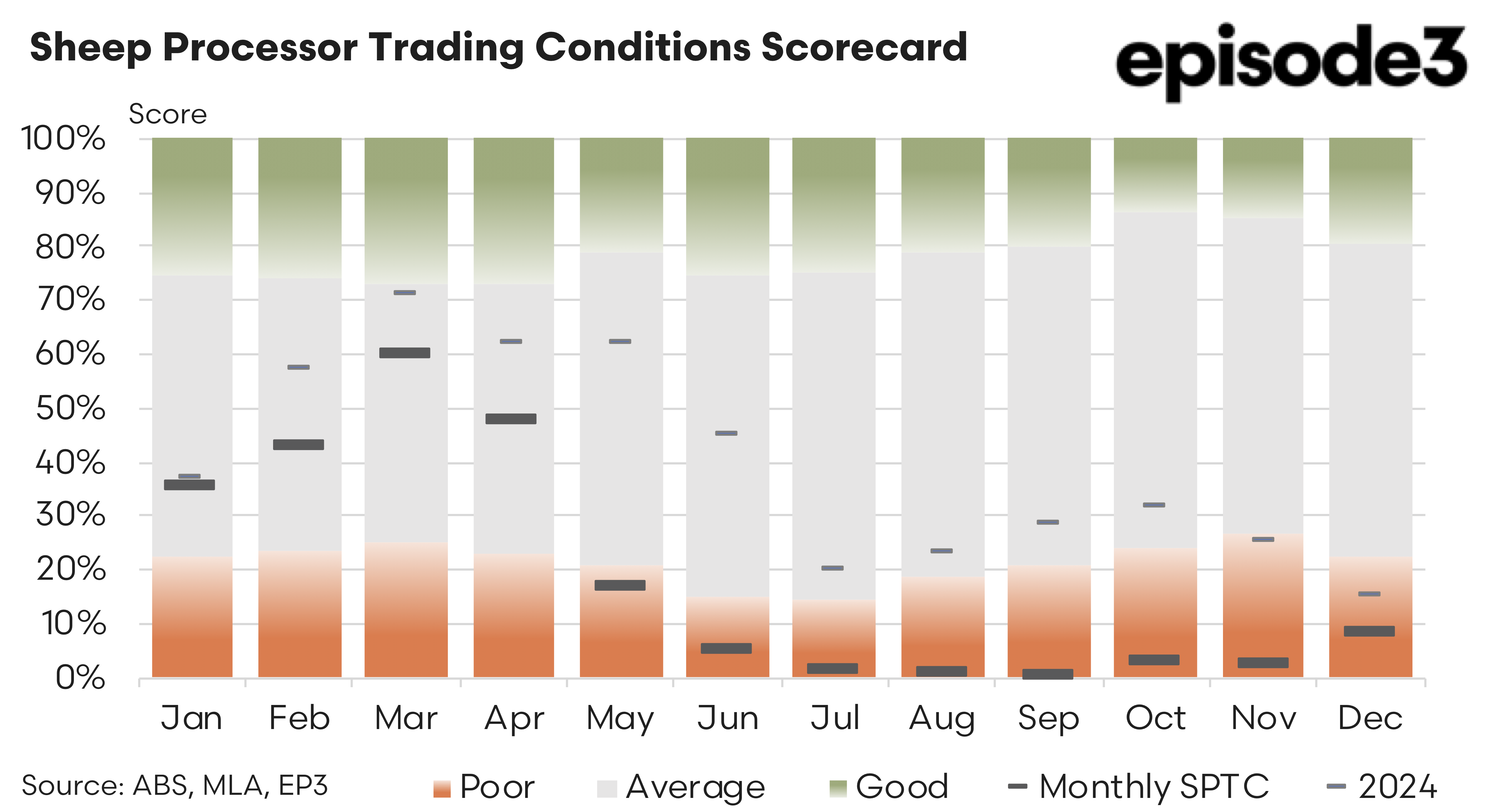

Updated export values for November saw the Sheep Processor Trading Conditions (SPTC) index revised down. The initial estimate of a seven percent index for the month has now been recalculated at two percent, reflecting softer realised export returns across several key destinations. While still positive, the revision highlights how sensitive processor margins are to relatively small shifts in export prices. For a sector operating on tight spreads between livestock procurement costs and saleable product values, a few percentage points either side of expectations can materially alter the monthly outcome. In practice, this translated into a weaker-than-first-reported margin outcome for November.

December provided a more constructive result. The SPTC index for the month came in at eight percent, a clear improvement on the revised November figure and a sign that processors were able to recover some ground heading into the end of the calendar year. Export values in December showed firmer outcomes in several markets, particularly Malaysia and the United States, which helped offset a small decline in prices to China and the UAE. The combined effect was a slight lift in the overall average export value compared with November.

Domestic cost movements also played a role. Livestock procurement costs were relatively stable through the late spring period, though the underlying trends differed between categories. Mutton values edged higher slightly, while lamb prices were marginally softer over the key comparison window. These movements did not dramatically alter the cost base, but they provided some incremental relief on the procurement side of the ledger. Retail lamb prices in December also recorded a small increase, suggesting that domestic market conditions were broadly supportive, albeit not a major driver of processor margins.

The revised November figure and the stronger December outcome reinforce the notion that processor trading conditions are improving only gradually. The late-year performance shows that while the sector has moved off the lows experienced earlier in the cycle, margins remain highly sensitive to export price volatility and to any changes in livestock procurement costs. The eight percent reading for December 2025 represents a modest but meaningful improvement and indicates that processors were able to finish the year with a more positive margin position than the revised November figure alone would suggest.

However, the annual perspective tells a more sobering story. The average SPTC for the 2025 season is now estimated at 19 percent, a significant decline from the 40 percent average recorded in 2024. That shift reflects a year characterised by tighter spreads, elevated livestock costs for much of the period, and only intermittent support from export markets. While the latter part of the year delivered some improvement, it was not enough to offset the weaker margins experienced through earlier months.

The contrast between 2024 and 2025 highlights how quickly processor profitability can shift in response to market conditions. In 2024, relatively favourable export prices and more manageable livestock procurement costs supported stronger margins. By comparison, 2025 saw a more challenging environment, with processors needing to manage tighter spreads and greater variability in export returns. The revised November figure and the December recovery encapsulate this dynamic, showing how quickly margins can be reshaped by updated data and by short-term price movements.

Looking ahead, the key question is whether the improvement seen in December can be sustained. Export demand remains the primary driver of processor profitability, and any further gains in key markets such as the United States or Southeast Asia would provide welcome support. At the same time, livestock procurement costs will remain a critical factor. If sheep and lamb prices strengthen as flock rebuilding gathers pace, processors may once again find margins squeezed unless export values rise in tandem.

For now, the late-year data point to a sector that is stabilising but not yet fully recovered. The revision of November’s margin to two percent underscores how fragile improvements can be, while December’s eight percent reading offers some encouragement. The annual average of 19 percent, well below the previous year’s level, serves as a reminder that 2025 was a year of tighter conditions and incremental progress rather than a full-scale rebound.