Farm Around and Find Out

The Snapshot

- US farm bankruptcies follow profitability, not politics, but policy shapes those margins

- Trade tensions and tariffs in the late 2010s coincided with rising financial stress

- Government support and strong prices masked pressure through 2021–2023

- The lift in bankruptcies into 2024 and 2025 suggests margins are tightening again

- US policy settings continue to influence global markets, including Australia

The Detail

Farm bankruptcies tell a consistent story over time. They rise when margins come under pressure and fall when profitability improves. What is often missed, however, is how strongly policy settings can influence those margins, particularly through trade.

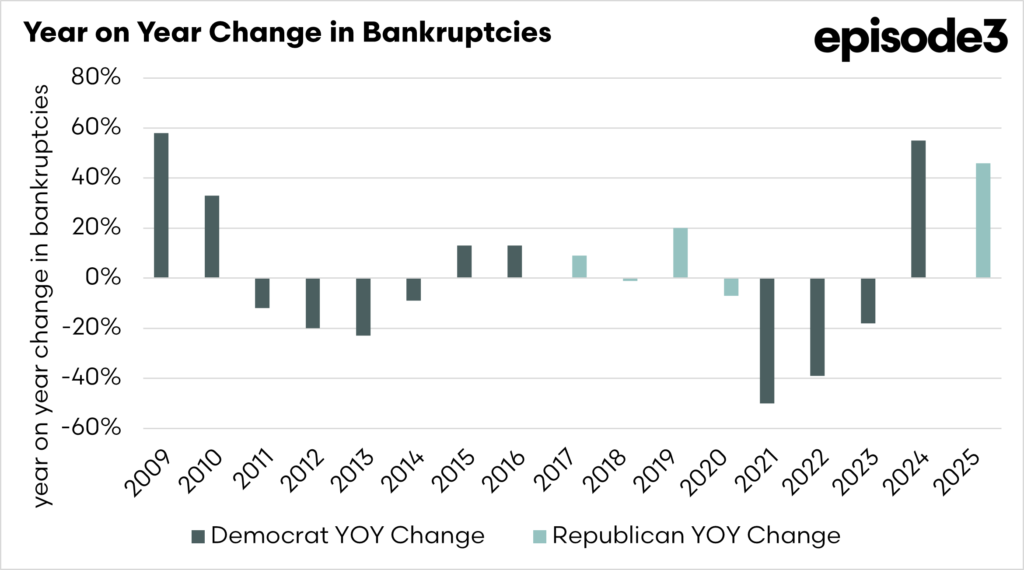

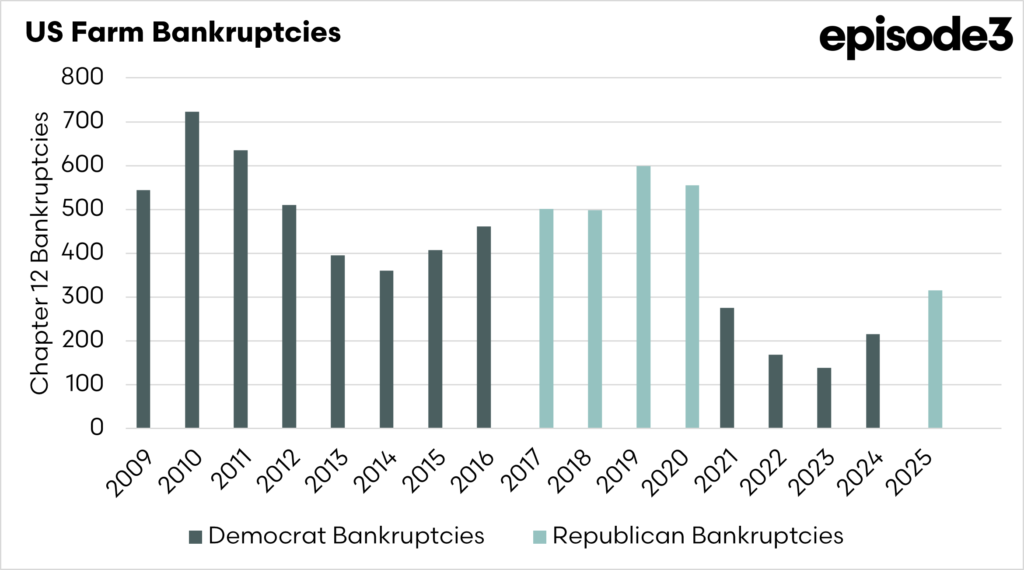

Following the global financial crisis, bankruptcies rose, peaking at more than 700 cases in 2010, in the early years of the Obama administration. That reflected weak prices, tighter credit and broader economic stress. As conditions improved through the early to mid-2010s, bankruptcies fell steadily, reaching around 360 by 2014. This was a period of stronger commodity prices and relatively stable global trade flows.

The cycle shifted again in the late 2010s. Bankruptcies lifted back towards 600 by 2019 and remained elevated into 2020 during the Trump administration. This period coincided with the introduction of tariffs and escalating trade tensions between the United States and China. For US agriculture, the impact was direct. Key export markets were disrupted, particularly for commodities such as soybeans, and price volatility increased. While support payments helped offset some of the losses, they did not fully remove the pressure on farm margins.

Farmers do not respond to party lines; they respond to prices, costs and access to markets. But policy decisions, including trade policy, shape all three. The late 2010s give a clear example of how changes in market access can translate into financial stress at the farm level.

After 2020, the picture changed sharply. Bankruptcies fell to just 139 by 2023 under the Biden administration, the lowest level in the dataset. Strong global commodity prices, significant government support and improved balance sheets combined to reduce financial stress.

That stability now appears to be fading. Bankruptcies rose to 216 in 2024 and have lifted again to 315 in 2025, as the policy environment again shifts. The drivers are familiar. Higher interest rates are increasing the cost of servicing debt, while input costs, particularly fertiliser and fuel, remain elevated. At the same time, global trade remains uncertain, with ongoing geopolitical tension and evolving policy settings continuing to influence market conditions.

This is where the link back to policy becomes relevant again. Trade disruption, whether through tariffs, sanctions or broader geopolitical tension, reduces certainty and can limit access to key markets. For export-oriented sectors like agriculture, that flows directly into price risk and margin pressure. Different administrations may approach trade and international relations in different ways, but the transmission mechanism into farm profitability remains the same.

For Australian farmers and agribusiness, the implications are clear. We operate in the same global system, and US policy decisions can shift trade flows, influence pricing, and alter competitiveness. When US exports are disrupted, those volumes often need to find a home elsewhere, reshaping global markets. At the same time, volatility in input costs and energy markets feeds through to Australian production systems.

The recent rise in US farm bankruptcies does not yet signal a crisis, as levels stay well below those seen in earlier periods of stress. However, the change in direction matters. It suggests margins are tightening again, and that the combination of higher costs and uncertain trade conditions is beginning to bite.

It is important to note that this dataset of bankruptcies is prior to the US/Israel war against Iran, which has caused tremendous impacts on global markets, especially in the inputs that farmers need.

The lesson is that who you vote for matters. Policy decisions shape margins, and margins drive outcomes. When policy disrupts markets, the farmer ends up paying the cost.