Australia’s winter crop: still large, but the hard work starts now

The Snapshot

- National winter crop production is forecast at 54.5 million tonnes, down 21pc on last season but still 4pc above the 10-year average

- High fuel and fertiliser costs are squeezing margins, with the biggest uncertainty around whether growers will continue applying urea for top-dressing in July and August

- The season is sharply divided geographically, with NSW and Queensland facing falls of around 37-38pc while SA and Victoria remain close to or above their 10-year averages

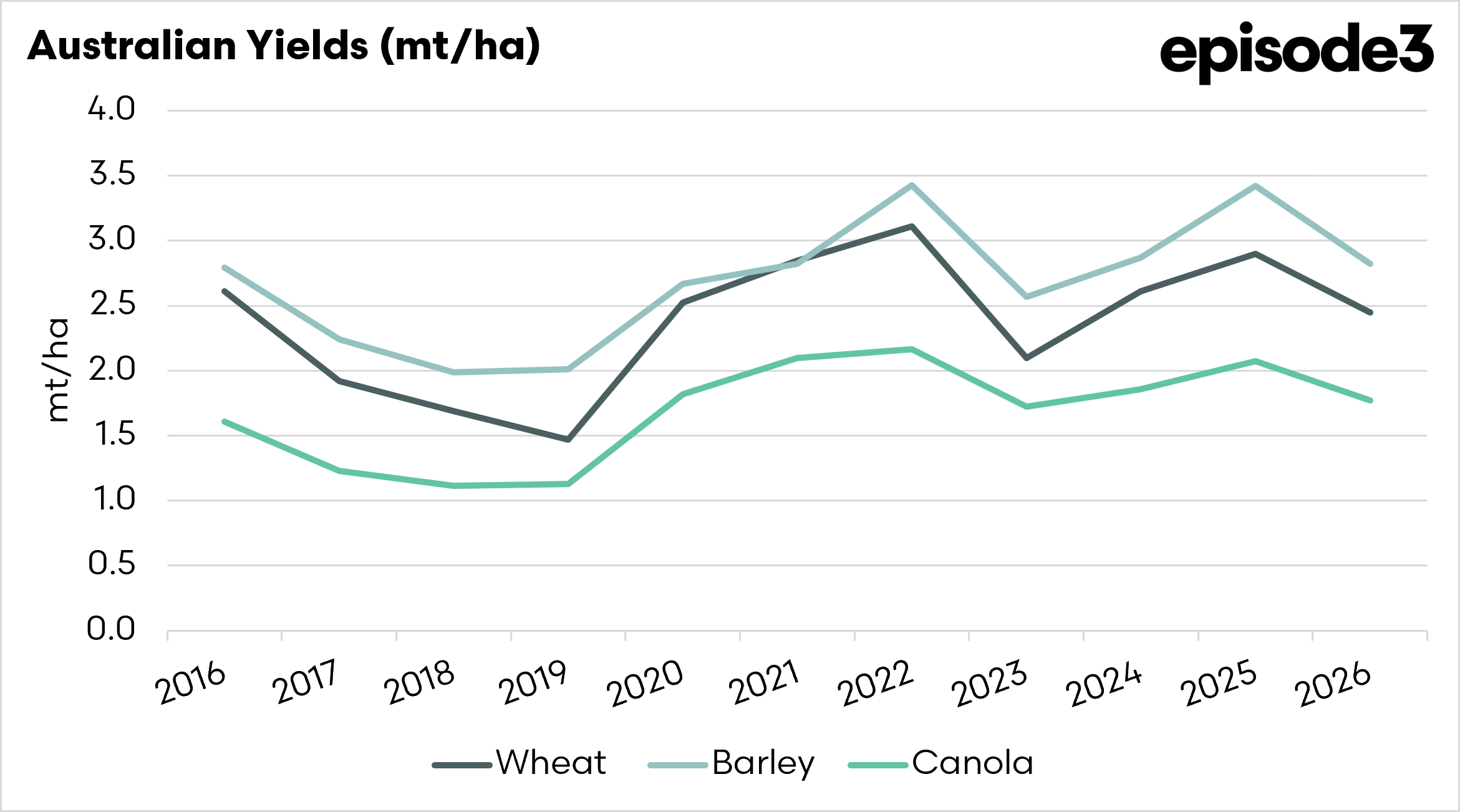

- Growers are shifting their crop mix away from wheat toward barley, which has lower fertiliser requirements and handles drier conditions better

- The Bureau of Meteorology is forecasting a 60-80pc chance of below-average winter rainfall across major cropping regions, leaving the final outcome heavily dependent on what happens over the next few months

The Detail

Australian grain growers are heading into the 2026–27 winter cropping season with a decent crop still on the cards, but with a lot less comfort than last year. This year has been one of the hardest for analysts and traders to get a handle on because of the amount of change driven by a possible El Niño, already dry weather, and events in the Middle East. Despite these challenges, the forecasts are for another large crop.

The June ABARES crop report has a national winter crop production forecast at 54.5 million tonnes, down 21 per cent from last season. In most years, that would sound like a serious fall, and in one sense, it is. But context matters. The downgrade sounds large, but the crop would still sit 4pc above the 10-year average and rank as the seventh-largest winter crop on record, so this is not a disaster forecast, provided the weather cooperates.

The national crop is still large by historical standards, but it is on potentially uneven ground. It is more exposed to winter rainfall, more exposed to fertiliser decisions, and much more uneven across the country than the headline number might suggest.

The issue Australian agriculture has been discussing more than usual has been costs, and ABARES is direct about the pressure from fuel and fertiliser markets, with the conflict in the Middle East disrupting global supply chains for liquid fuels and fertiliser. Australian broadacre farmers are exposed because they rely heavily on imported inputs and have limited short-term ability to substitute.

The problem is currently price rather than outright shortage, which is something that EP3 have been discussing since the start of the conflict, but the supply is riskier the longer the conflict continues.

The more important fertiliser question may not be what was available at sowing, but what growers are willing to buy later. ABARES expects growers to have sufficient fertiliser for planting, but there is greater uncertainty about urea for July and August top-dressing. If growers decide that urea is too expensive, or if they choose to ration applications, that decision will show up in final yields. A crop can be planted and established, but still fall short if growers are not prepared to chase the yield potential through winter, which, at EP3, we believe is a significant risk in 2026.

Australia is a huge continent, and the production forecasts are split around the country. Western Australia, South Australia and Victoria had a much better start to the season, with average to well-above-average rainfall from February to April, lifting soil moisture and giving growers more confidence to plant. The north is a different story. Northern New South Wales and southern Queensland were extremely dry through mid-May, leaving soil moisture levels low and forcing many growers into difficult decisions. Late May rain may have helped, but once the main window starts to close, the response is limited by timing, seed availability, fertiliser availability and appetite for risk.

That split shows up clearly in the state forecasts. New South Wales winter crop production is forecast to fall 37pc to 11.7 million tonnes, while Queensland is forecast to fall 38pc to 2.4 million tonnes. By contrast, South Australia is forecast to hold broadly steady at 9.1 million tonnes, still 13pc above its 10-year average, while Victoria is forecast at 9.7 million tonnes, down only 4pc and still 10pc above its 10-year average. Western Australia is forecast to fall 21pc to 21.5 million tonnes, but that comes after record production last season and still leaves the state 11pc above its 10-year average.

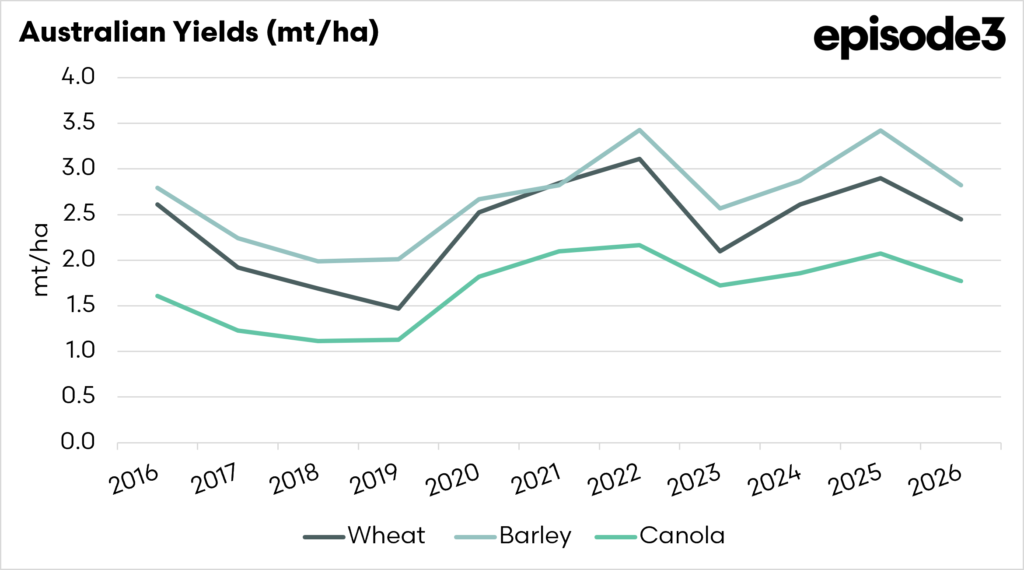

ABARES forecasts national wheat production at 26.7 million tonnes, down 26pc year-on-year. Area planted to wheat is forecast to fall 12pc to 10.9 million hectares, which would be the smallest wheat area since 2019–20. Wheat is still the dominant winter crop, but it is losing ground this season because margins are being squeezed, fertiliser is expensive, northern cropping regions have been dry, and in some areas other crops simply look more practical.

The wheat downgrade is not evenly spread. In New South Wales, wheat production is forecast to fall 38pc to 7.0 million tonnes. In Queensland, it is forecast to fall 43pc to 1.32 million tonnes. Western Australia, coming off a record year, is forecast to fall 29pc to 9.47 million tonnes. South Australia and Victoria are far steadier, with wheat production forecast at 4.66 million tonnes and 4.22 million tonnes, respectively. This is the heart of the wheat story: a large WA crop coming back to earth, and the dry north taking a heavy bite out of area and yield prospects.

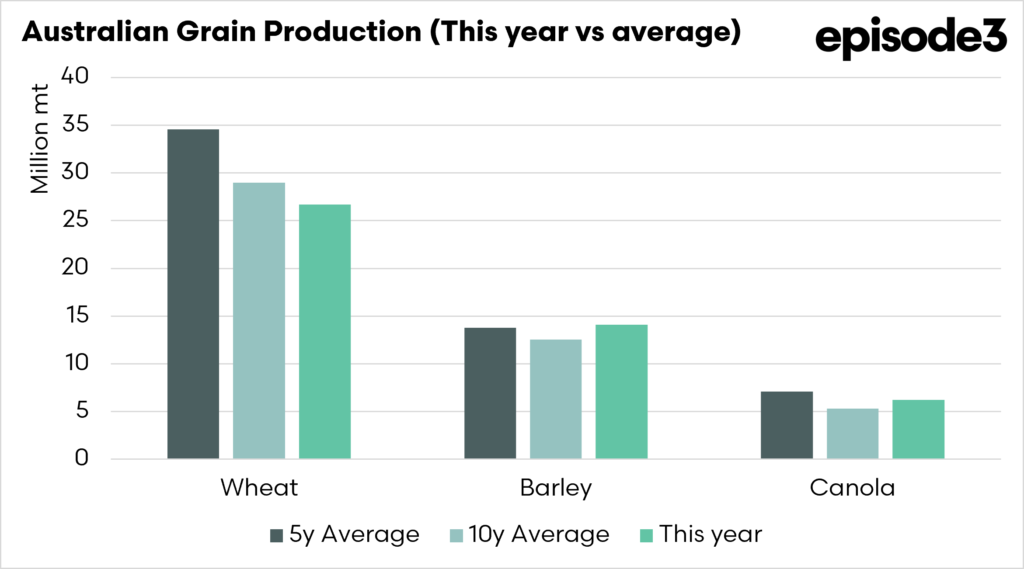

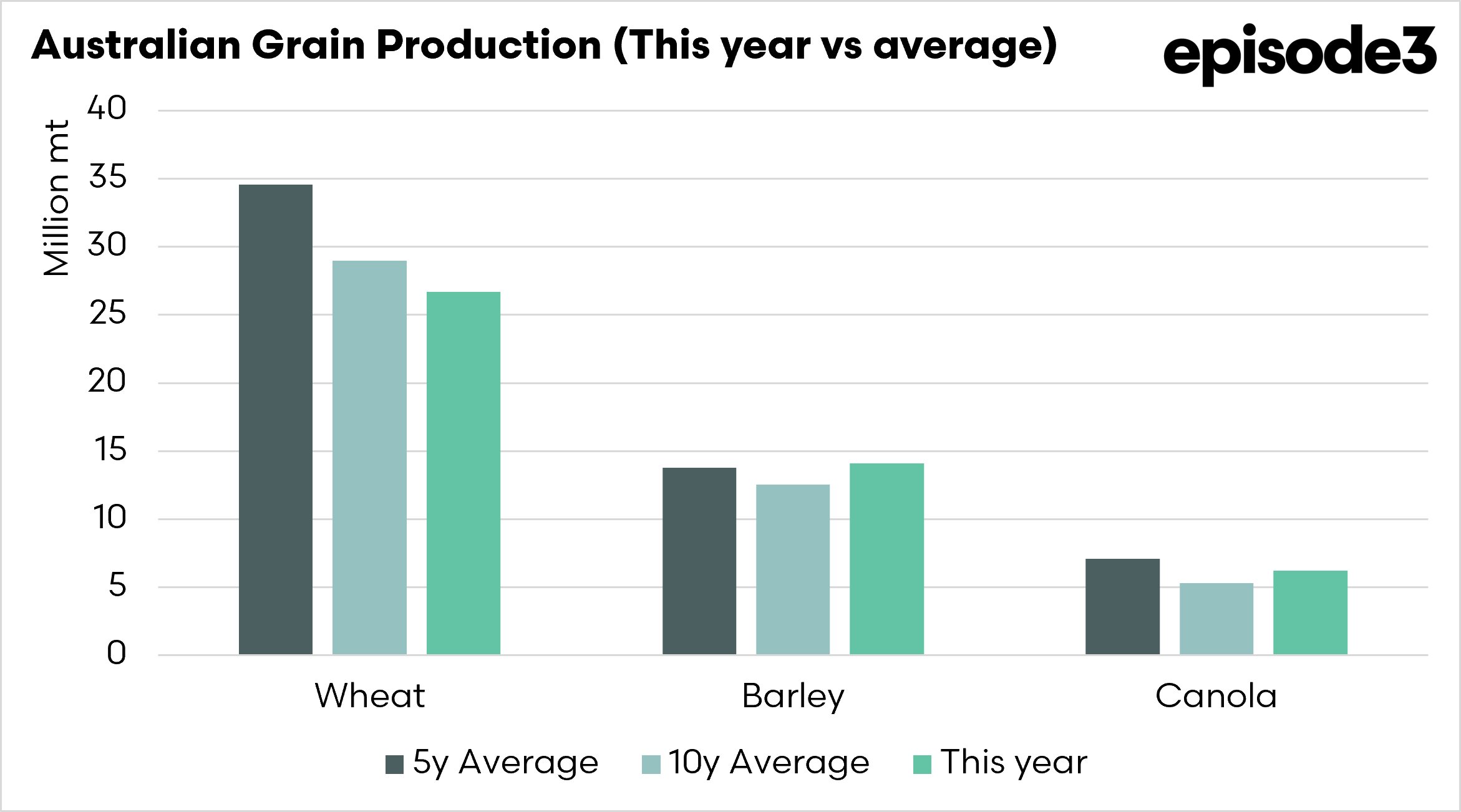

Barley is the more interesting story, because while production is forecast lower, area is forecast higher. National barley production is forecast at 14.1 million tonnes, down 15pc on last season, but still 2pc above the five-year average and 12pc above the 10-year average. More importantly, barley area is forecast to rise 4pc to 5.0 million hectares.

Barley fits this season better than wheat in many areas. It has lower fertiliser requirements, can handle drier conditions more comfortably, and is supported by feed demand and relatively strong prices. In a year when growers are looking at input costs with a sharper pencil, barley becomes a practical choice. This does not mean barley production escapes the seasonal downgrade, with WA, NSW and Queensland all forecast to be lower, but South Australia is forecast to lift slightly to 2.18 million tonnes. The national area increase says a lot about how growers are managing risk.

Canola sits between these two stories. Production is forecast at 6.2 million tonnes, down 20pc on last year, but still 17pc above the 10-year average. Area planted to canola is forecast to fall 6pc to 3.5 million hectares, but most of that fall is a New South Wales story. Dry conditions in northern cropping regions closed the ideal planting window and prompted some growers to forgo canola. NSW canola production is forecast down 34pc to 1.05 million tonnes.

In Western Australia, Victoria and South Australia, the picture is better. ABARES expects modest increases in area in those states, although production is still forecast to be lower as yields are expected to ease. WA is still the key canola state, with production forecast at 3.4 million tonnes. The important point is that canola has not been abandoned, even with high fertiliser prices. Where soil moisture is adequate, growers are still prepared to plant it because the gross margins can still stack up against cereals.

The pulse story adds another layer to the seasonal divide. Lentils continue to build momentum, with production forecast to rise 3pc to a record 2.2 million tonnes, more than double the 10-year average. Chickpeas are going the other way, with production forecast to fall 51pc to 1.1 million tonnes, largely because the key growing regions in northern New South Wales and southern Queensland had such poor planting conditions. Lupins are also expanding, with WA production forecast at 990,000 tonnes, up 8pc, helped by livestock feed demand and lower input requirements.

The Bureau of Meteorology outlook, cited by ABARES, shows a 60pc to 80pc chance of below-average winter rainfall across many cropping regions. The south and west have stored moisture to lean on, and Australian growers have become better at turning marginal starts into reasonable outcomes. But the margin for error is thinner than it was last year.

Australia is still forecast to produce a large crop, but it is not the comfortable crop of last season. Wheat is carrying the most obvious downside risk. Barley is gaining favour because it fits the cost and seasonal environment. Canola is still strong where moisture allows it. Lentils are a standout. Chickpeas are the casualty of the dry north. The headline number still looks good, but the season underneath it looks far more complicated.

The season is likely to be one of the most complex we have experienced in a long time, and we expect the June forecasts to be revised further in the next update. The rain still needs to come.