Fertiliser Falls, Wheat Softens, Risks Remain

The Snapshot

- Australia is still forecast to produce an above-average winter crop despite a difficult start in the north.

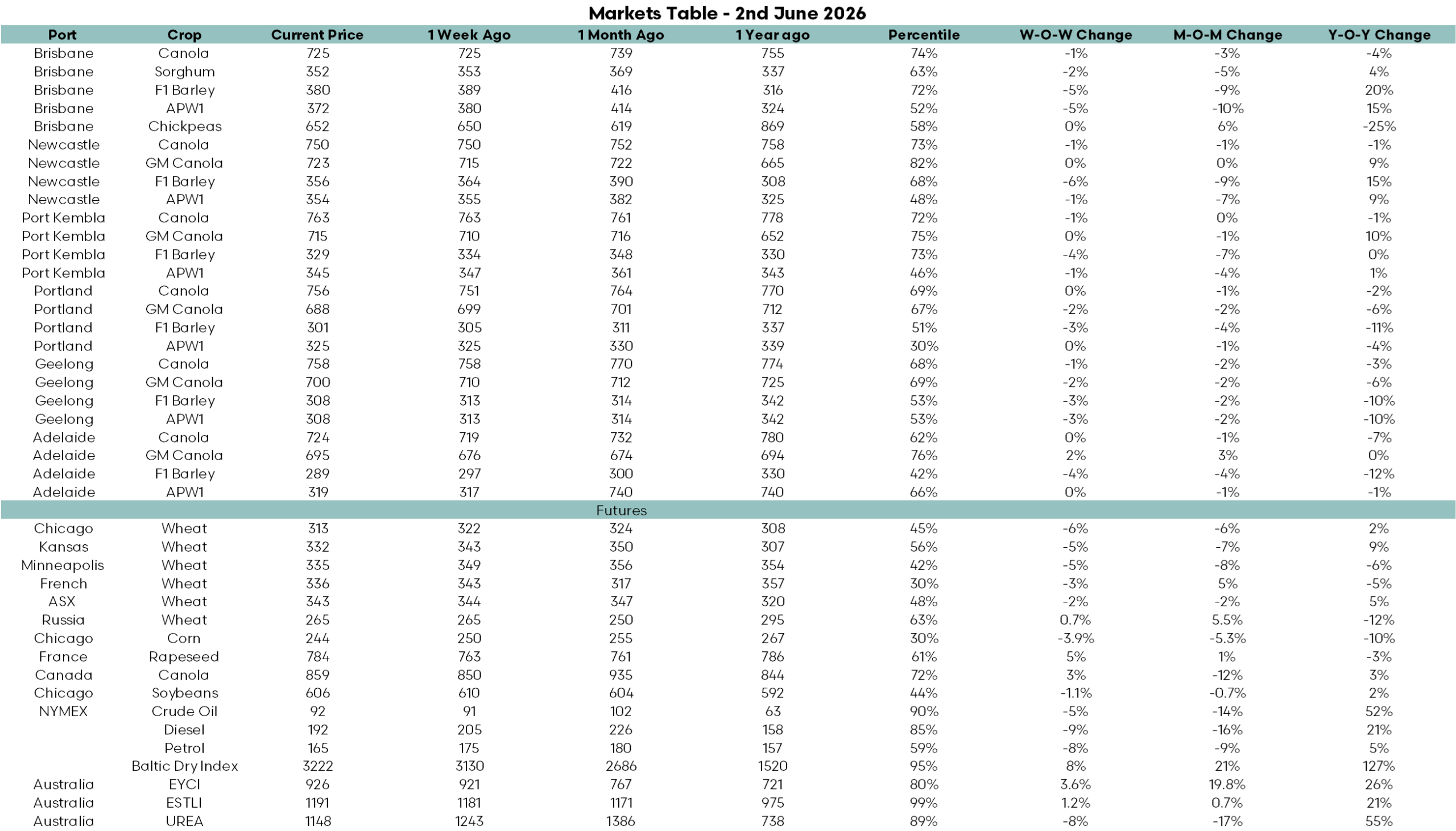

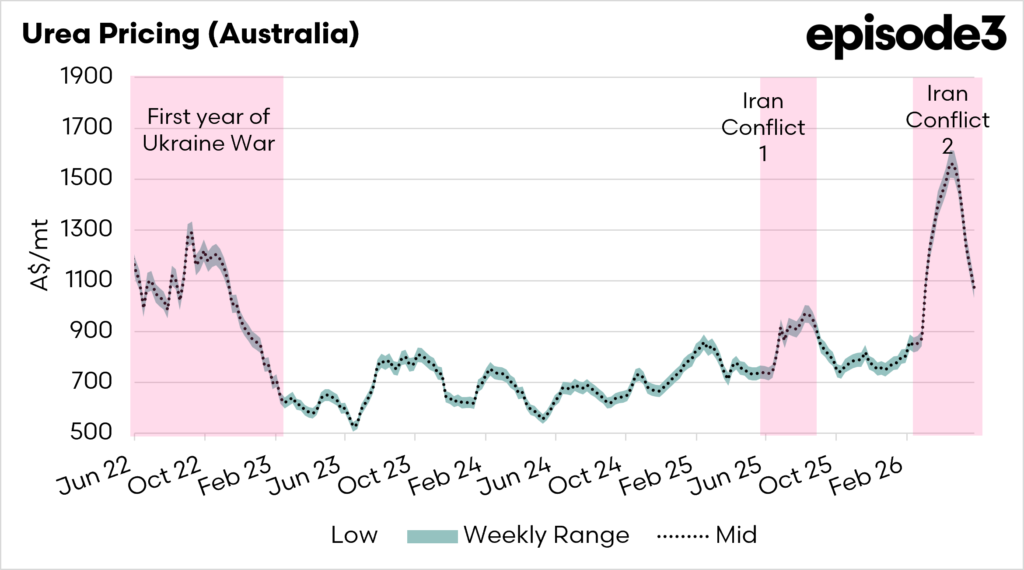

- Falling urea prices are providing some relief, but fertiliser remains historically expensive.

- Strong US and Ukrainian production prospects are weighing on global grain markets.

- Russian wheat remains unusually firm due to a strong ruble and limited farmer selling.

- Fuel, fertiliser and freight costs continue to be the biggest margin risks for growers

The Detail

Australian grain growers head into winter with a reasonably large crop still on the cards, but the season is becoming increasingly complex. The latest ABARES forecast places national winter crop production at 54.5 million tonnes. That is down 21pc on last season’s exceptional result, but still above the long-term average. The headline number looks comfortable enough, but the reality beneath the surface is far more uneven.

The season has become increasingly divided between regions. Western Australia, South Australia and much of Victoria entered winter with reasonable soil moisture profiles following a stronger start to the year. The northern production regions have faced a much tougher run. New South Wales and Queensland endured an exceptionally dry autumn, leaving growers to make difficult planting decisions and increasing their reliance on winter rainfall. The national crop forecast remains respectable, but much of the outcome will depend on rainfall over the next few months and on fertiliser applications.

At the same time, growers are receiving some welcome relief on the input cost front. Urea prices have continued to ease as global supply improves. China’s return to the export market has helped soften international sentiment, while Australian supply has improved significantly with large import volumes scheduled to arrive through May and June. Domestic warehouse values have retreated noticeably from the highs seen earlier in the year.

That relief should not be confused with cheap fertiliser. Urea remains historically expensive, and many growers are already looking ahead to top-dressing decisions in July and August. The question is no longer whether fertiliser will be available, but whether growers will be willing to apply as much nitrogen as they normally would. In a season where margins remain under pressure, fertiliser decisions may have as much influence on final yields as the weather itself.

Global grain markets are also becoming less supportive than they were several weeks ago. Favourable crop conditions across much of the US Midwest continue to weigh on corn and soybean markets, while Ukraine is forecasting a larger grain and oilseed harvest in 2026. Improved global supply expectations have pushed grain futures lower, with Chicago wheat, corn and soybeans all weakening during the week.

Wheat is still the exception. Russian export wheat values continue to hold firm despite softer futures markets elsewhere. A strong ruble and continued reluctance by Russian farmers to sell grain have kept export prices elevated. Russian wheat values remain near season highs even as global futures have softened. While global supply remains comfortable overall, the world’s largest wheat exporter continues to support the market.

The final theme is energy and logistics. Oil prices continue to react to developments in the Middle East, with markets moving sharply as hopes of progress in negotiations between the United States and Iran rise and fall. For Australian agriculture, the impact is less about crude oil itself and more about what it means for fuel, fertiliser and freight costs. The longer uncertainty remains around the Strait of Hormuz and regional shipping routes, the greater the risk to input costs.

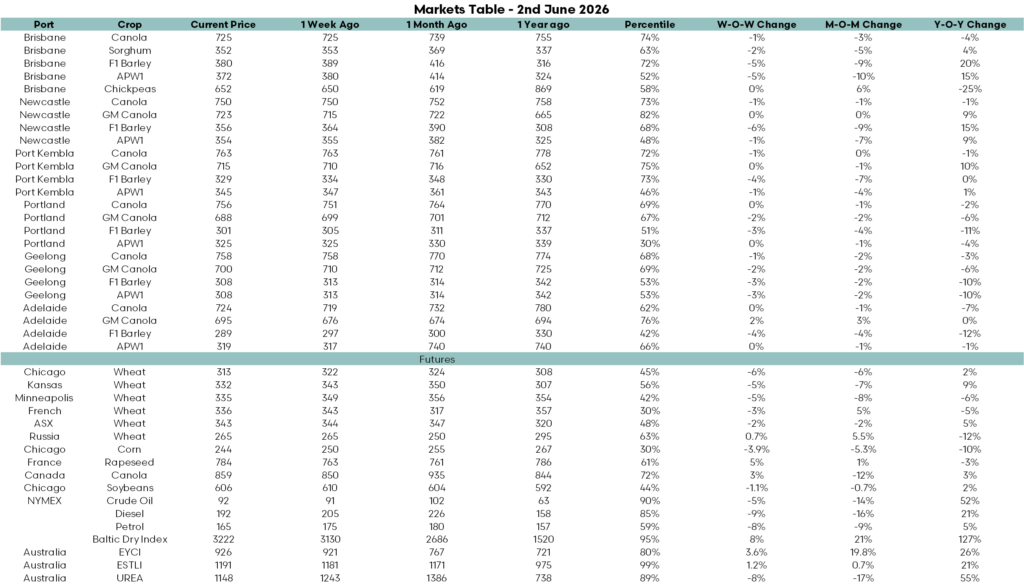

The accompanying market table reflects many of these themes. Grain markets were generally weaker over the week, with Chicago wheat down 6pc, Kansas wheat down 5pc, and corn down almost 4pc as traders focused on favourable crop conditions and improving global supply prospects. Australian grain markets also softened, particularly in the north, where improved seasonal conditions reduced some of the urgency that had supported prices earlier in the year. Brisbane APW1 fell 5pc over the week, while Brisbane and Newcastle barley values eased between 5pc and 6pc.

Input costs continue to move in the opposite direction. Urea fell another 8pc during the week and is now more than 20pc below levels seen a month ago. Diesel declined by 9pc, while petrol eased by 8pc. However, costs remain elevated by historical standards. Urea is still 55pc above year-ago levels, and freight remains expensive, with the Baltic Dry Index sitting 127pc above last year. The good news for growers is that Australia is being supported by a generally favourable seasonal outlook, while some of the pressure from fertiliser and fuel has started to ease. The challenge is that margins remain highly sensitive to both winter rainfall and global energy markets.