Wheat’s Bad News Isn’t Bad Enough

Summary & key takeouts

- Global grain markets remain under pressure as larger crops emerge across Russia, Ukraine and Europe.

- US wheat conditions are the worst in decades, but markets are looking beyond America to stronger crops elsewhere.

- South Australia’s crop is forecast to exceed 9 million tonnes, with lentils set for another record season.

- Speculative funds continue to sell wheat and corn as confidence in global grain supplies improves.

- Australian grain prices softened again this week, while livestock markets continued to strengthen.

The Detail

The grain market is becoming increasingly comfortable with supply, making it difficult for prices to find support. Over the past week, wheat, corn and soybean markets all came under renewed pressure as traders focused on expanding Northern Hemisphere production and the steady progression of harvest activity. While geopolitical tensions briefly returned to the headlines following renewed military strikes between Iran and Israel, the reaction across agricultural markets was muted compared to earlier in the year.

The reason is simple. Supply is currently winning the argument. Chicago wheat futures slipped to their lowest levels in around two months, extending a run of losses that has now lasted several weeks. Corn futures also pushed to fresh contract lows, while soybeans remained under pressure from favourable growing conditions across the US Midwest and the continued absence of significant Chinese buying activity.

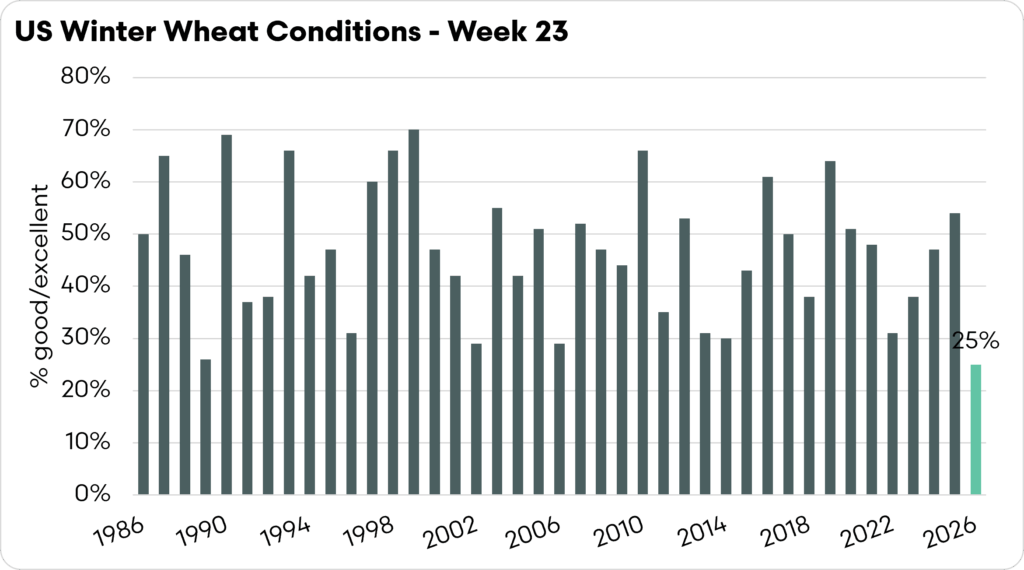

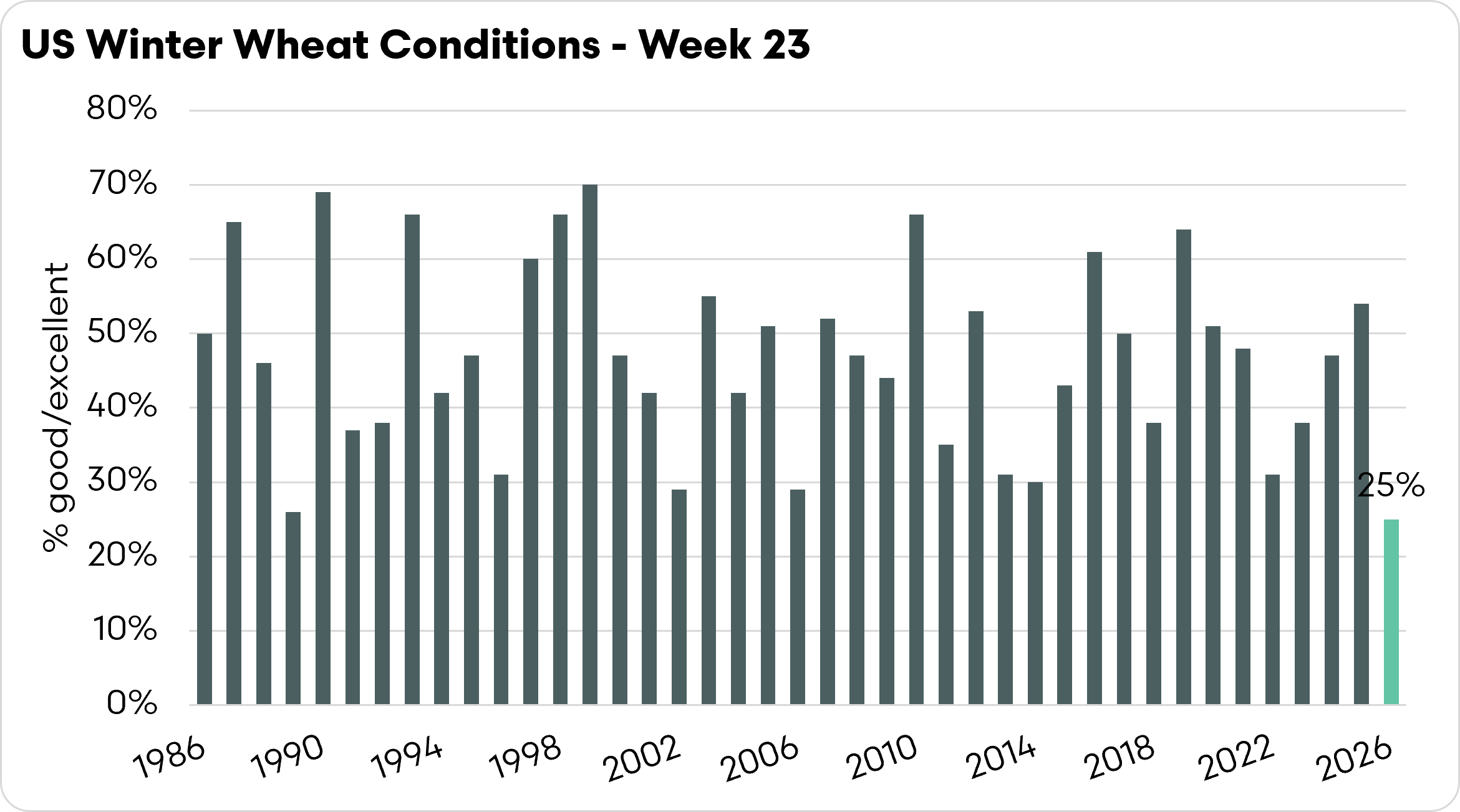

What makes the wheat story particularly interesting is that the US crop has historically been poor. Winter wheat conditions currently sit at just 25pc good-to-excellent, the lowest rating in the data series stretching back to the mid-1980s. In most years, a crop rating that weak would be enough to inject a significant risk premium into global wheat prices.

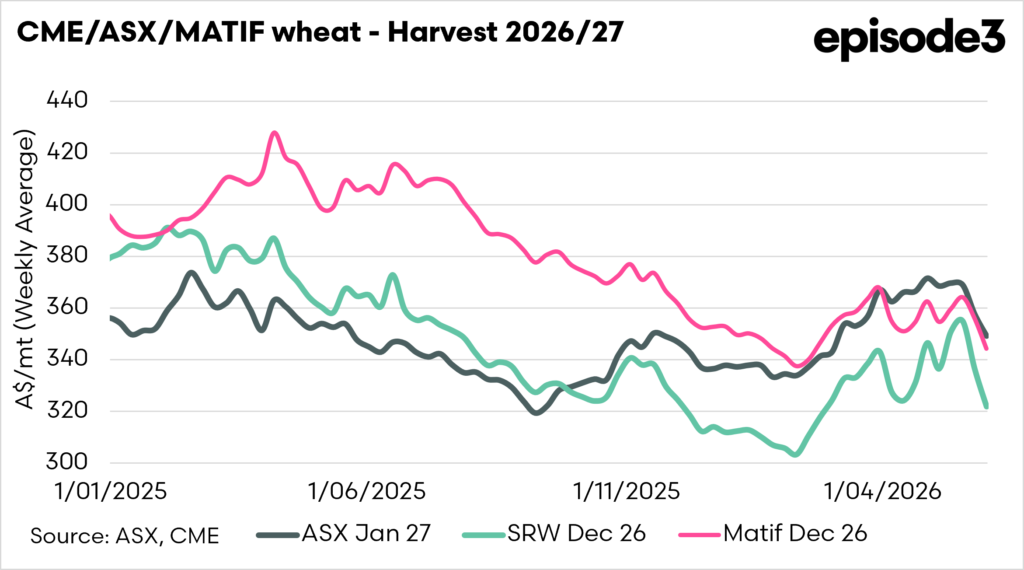

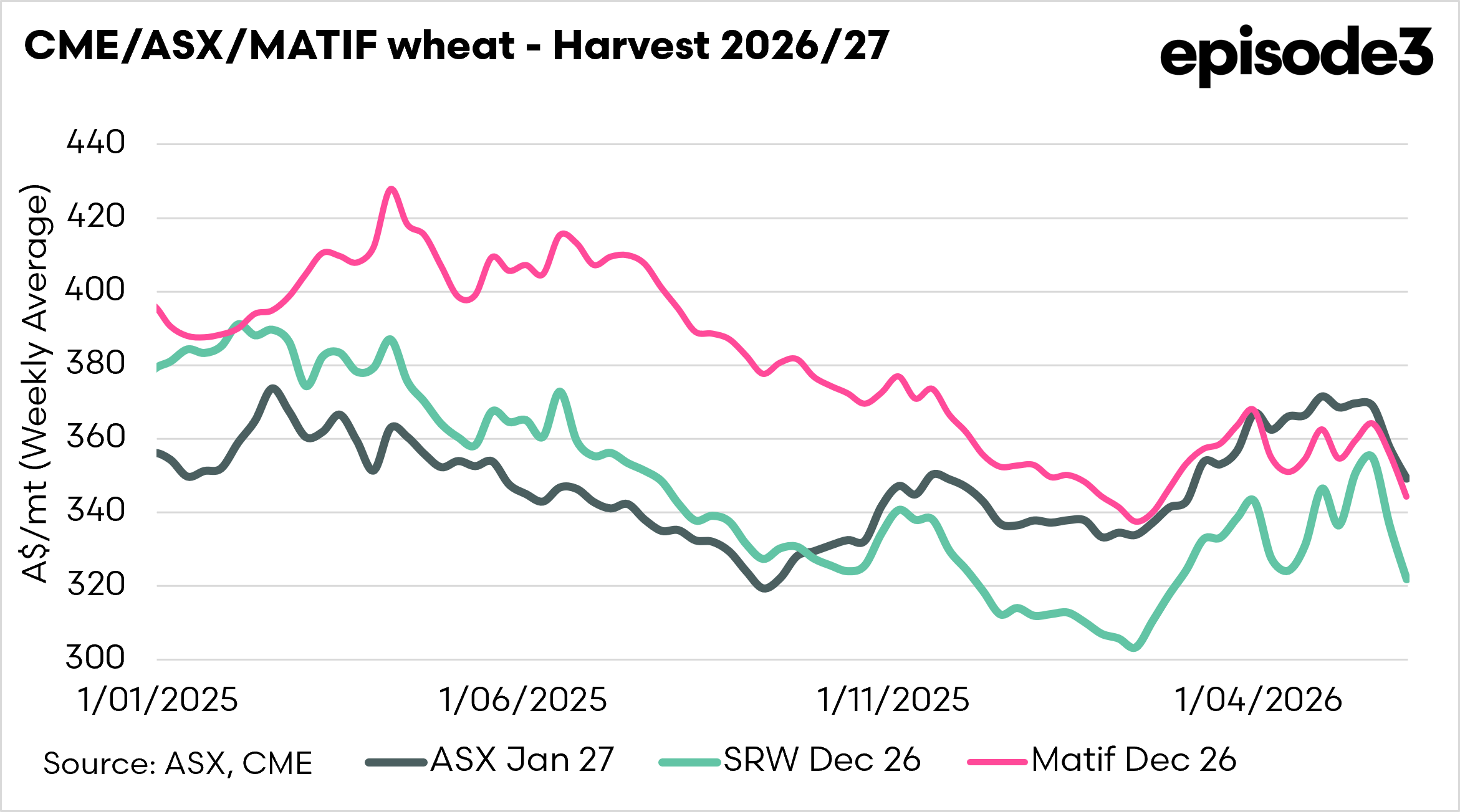

This year, however, the market is looking elsewhere. French wheat conditions are still relatively strong at 76pc good-to-excellent, despite some seasonal deterioration. More importantly, both Russia and Ukraine have recently increased production forecasts for the coming season. Ukraine’s wheat crop estimate has been raised to 21.7 million tonnes, while Russian forecasters have raised their estimate above 91 million tonnes. Those revisions are helping reinforce the view that global wheat supplies will remain comfortable despite production challenges in parts of the United States.

Russian export values, which had resisted the broader market weakness earlier in the season, have now started to soften as well. That shift is important because Russia remains the dominant force in global wheat trade. When Russian values begin moving lower alongside global futures, it becomes harder for other exporters to maintain price support.

Closer to home, the Australian production outlook continues to improve. South Australia’s first crop forecast for 2026-27 has pegged production at just over 9 million tonnes, making it the state’s largest crop since the record harvest of 2022-23. Good early rainfall has improved subsoil moisture, supported strong establishment and allowed seeding to progress rapidly across much of the state.

The standout crop continues to be lentils, with production forecast to reach another record and area expected to increase by around 12pc. The expansion reflects the continued search for profitable rotations and highlights how pulses are becoming an increasingly important part of southern Australian farming systems. The seasonal outlook has also improved for livestock producers, with better pasture growth easing pressure on supplementary feeding programs in many regions, although follow-up rainfall will still be required to maintain feed availability through winter and spring.

Perhaps the most notable feature of recent market activity is the growing disconnect between geopolitical developments and grain prices. Crude oil rallied sharply at various points during the week as tensions in the Middle East resurfaced, while vegetable oil markets and rapeseed futures also found support. Yet wheat, corn and soybeans continued to drift lower. Speculative funds appear to be reinforcing that trend, with managed-money traders cutting long positions in corn and soybeans while increasing bearish exposure in wheat.

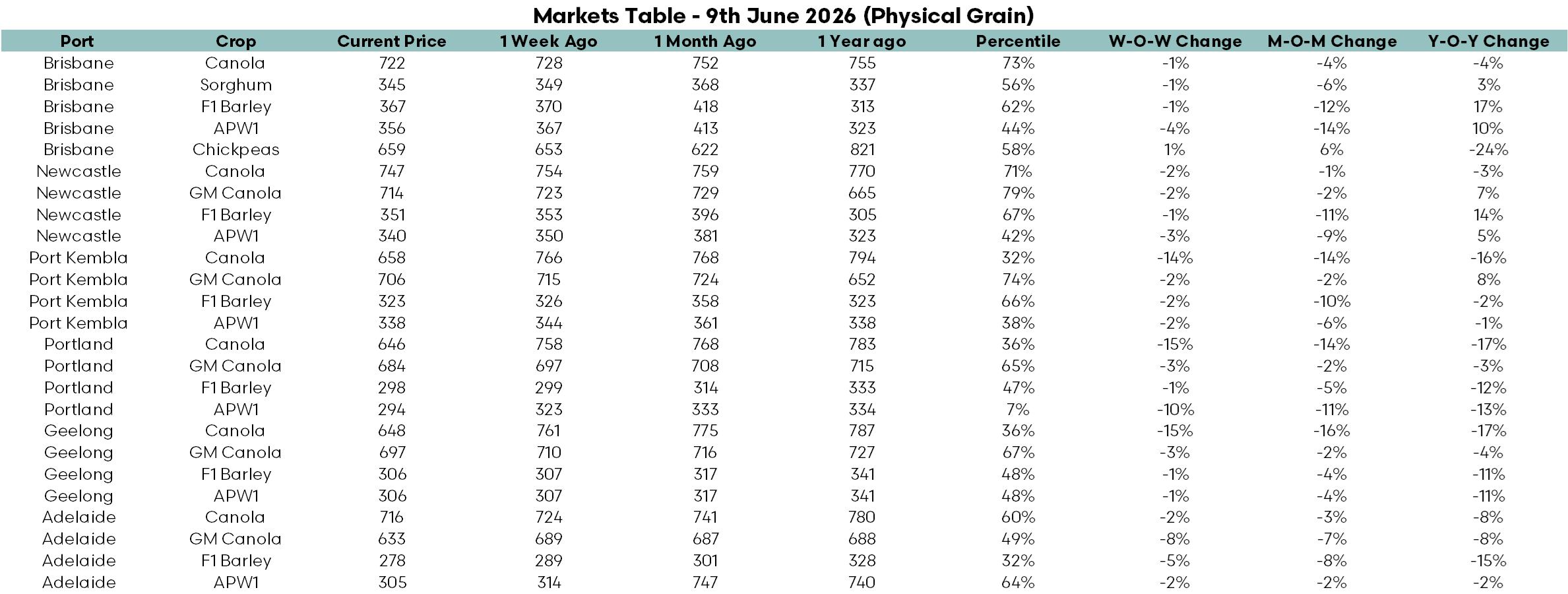

The accompanying market table reflects many of these themes. Australian grain prices weakened across most regions, particularly in eastern markets where wheat and barley values continued to ease. Brisbane APW1 fell 4pc over the week and is now down 14pc over the month, while Newcastle APW1 has slipped 9pc over the same period. Wheat futures also remained under pressure, with Chicago wheat down 2pc for the week and corn losing a further 3pc.

At the same time, canola markets held up better than cereals as energy markets provided some support. Livestock indicators continued to strengthen, with the EYCI lifting 19pc over the month and the Eastern States Trade Lamb Indicator reaching fresh highs. Freight costs remain elevated despite recent easing, while crude oil is still 40pc above year-ago levels. For now, the message from grain markets is clear. Production prospects across much of the world remain favourable, and until that changes, supply is likely to remain the dominant market influence.