Food inflation Update April 2026

Food Inflation Update - April 2026

Australia’s food inflation picture softened slightly through April, with the latest Consumer Price Index data showing some easing across protein categories even as fresh produce remained volatile. The broader annual trend, however, continues to show red meat and beverages driving food inflation higher compared with the same period last year. The result is a food basket still moving unevenly across categories, with short-term relief emerging in some areas while longer-term price pressures remain firmly embedded in others.

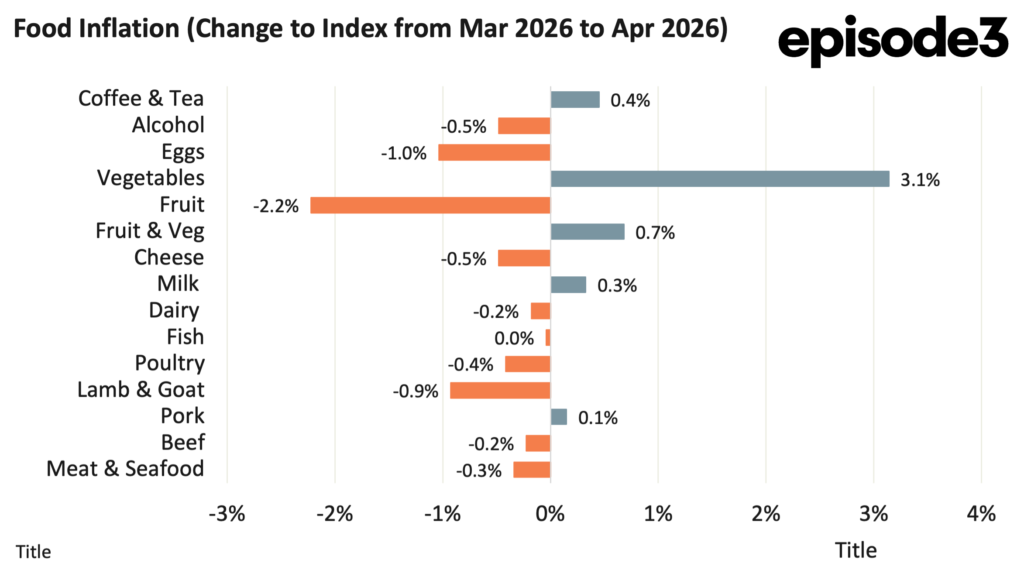

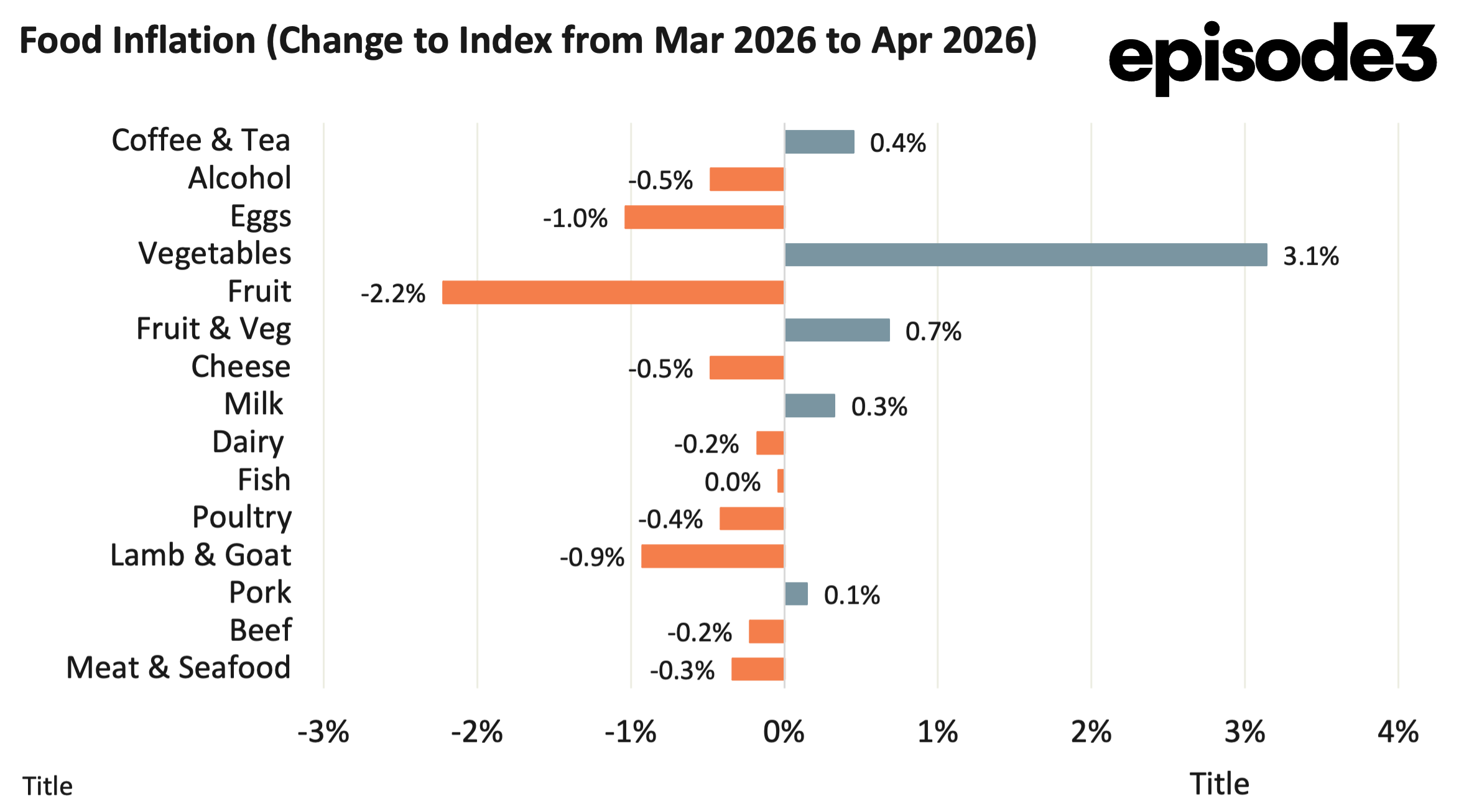

The monthly movement from March to April points to softer momentum across much of the protein complex. Lamb and goat prices fell 0.9 percent during the month, beef declined 0.2pc and poultry eased 0.4pc. The broader meat and seafood category slipped 0.3pc overall, suggesting some short-term cooling after several months of firm pricing.

Fresh produce movements remained volatile. Vegetable prices surged 3.1pc over the month, while fruit prices moved sharply lower, declining 2.2pc. Combined fruit and vegetable prices still increased 0.7pc during April.

Egg prices fell another 1.0pc over the month, continuing their weak trend. Dairy movements were mixed. Milk prices edged 0.3pc higher, while dairy overall declined 0.2pc and cheese fell 0.5pc. Coffee and tea prices rose modestly by 0.4pc during the month, while alcohol prices declined 0.5pc.

The annual picture into April 2026 remains heavily influenced by protein markets. Beef prices continue to lead the way, rising 8.4pc over the year as tight cattle supply and strong export demand continue to support domestic retail pricing. Lamb and goat prices have also strengthened further, now up 8.2pc annually. Reduced flock numbers and improved export conditions continue to underpin pricing across the sheep meat complex, helping lift the broader meat and seafood category 3.4pc higher over the year.

Other proteins remain comparatively subdued. Pork prices are up 0.9pc annually, poultry has increased 0.5pc and fish prices are 1.0pc higher.

Beverages remain another key source of inflationary pressure. Coffee and tea prices are up 4.9pc over the year, while alcohol has increased 3.0pc, reflecting both global supply dynamics and broader retail cost pressures.

Dairy inflation remains relatively moderate. Milk prices are 2.4pc higher annually and dairy overall has increased 1.7pc, while cheese prices remain slightly negative at -0.3pc.

Fresh food continues to present a softer annual inflation profile. Fruit prices are up just 0.8pc over the year, vegetables have increased 0.3pc and combined fruit and vegetable prices are only 0.5pc higher. Eggs remain one of the weakest categories, down 1.6pc annually.

The April data suggests Australia’s food inflation cycle is continuing to moderate compared with the broad-based pressure seen earlier in the decade. Fresh produce remains volatile monthly, but the annual trend has stabilised considerably, while protein inflation, although still elevated, showed signs of easing during April.

There remains a forward risk building outside the CPI data itself. Any prolonged disruption through the Strait of Hormuz would likely push fuel and fertiliser costs higher, adding further upward pressure to food prices in the months ahead.