Why Biofuels Won’t Fix Australia’s Fuel Shortage

The Snapshot

- Biofuels could be a small part of the solution to the fuel crisis. Even using all surplus canola only covers 4pc of diesel demand.

- Output swings with the weather, from 6pc in drought years to 25pc in bumper years. It is not a reliable system.

- Realistic policy settings of 10–20pc diversion deliver just 0.4–0.9pc diesel and 4–8pc petrol displacement.

- There is no large-scale biofuel refinery yet. Meaningful production is unlikely until the end of this decade.

- The real case for biofuels is farm margins and diversification, not short-term energy security.

The Detail

The conflict in the Middle East is a major cause for concern this year and likely next. Fuel supply is high on the list of concerns, and rightly so. Australia imports around 90% of its liquid fuel, predominantly from Asia, which in turn imports a significant volume of crude from the Middle East. Australia consumes roughly 55,000 megalitres of liquid fuel each year, including around 32,000 megalitres of diesel and 18,000 megalitres of petrol.

The solution from many is that a biofuels industry would solve a future fuel supply crisis. The idea that we should turn to our grain belt for a solution has a surface logic.

We grow a lot of grain and oilseeds, we export most of it, and we have been talking about a domestic biofuel industry for two decades. This time, a A$1.1bn government commitment behind the Clean Fuels Program and the first large-scale refineries are finally in the planning pipeline, the conversation is more serious than it has ever been.

In my view, there is a genuinely good case for building an Australian biofuel industry, but it will not solve the fuel security crisis which we face. And before we go any further, it is worth running the numbers honestly, because the numbers have a way of reframing the argument.

What can we produce?

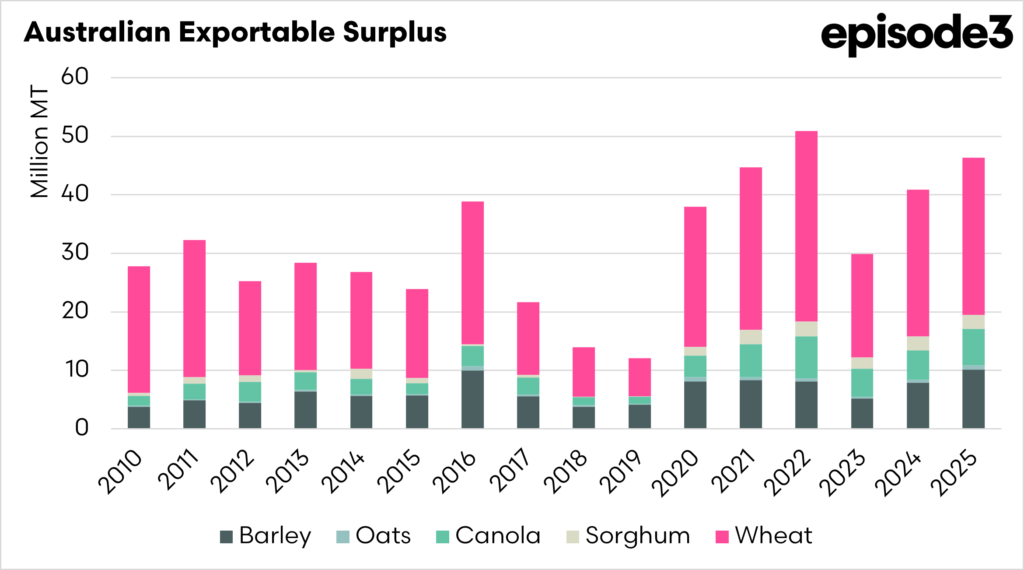

Australia produces a significant surplus of grain and oilseed beyond domestic consumption, and that is the starting point. This is the volume typically available to export, and therefore the pool that could theoretically be redirected into biofuel production.

I have chosen barley, oats, canola, sorghum and wheat for this analysis, and over the period 2010 to 2025, the volume available for export has averaged around 31mmt, ranging from roughly 12mmt to 51mmt depending on the season.

We have used industry conversion rates to provide a theoretical analysis of the total volume of fuel which we could produce from our grains. Wheat, barley, sorghum, and oats produce 300-380 litres of bioethanol per tonne. Canola converts to biodiesel at around 420 litres per tonne. Once you factor in that biofuels don’t pack as much energy as regular fuel, things become clearer. Ethanol gives you about two-thirds of the energy of petrol, while biodiesel gets you a bit closer, at around 90pc of diesel.

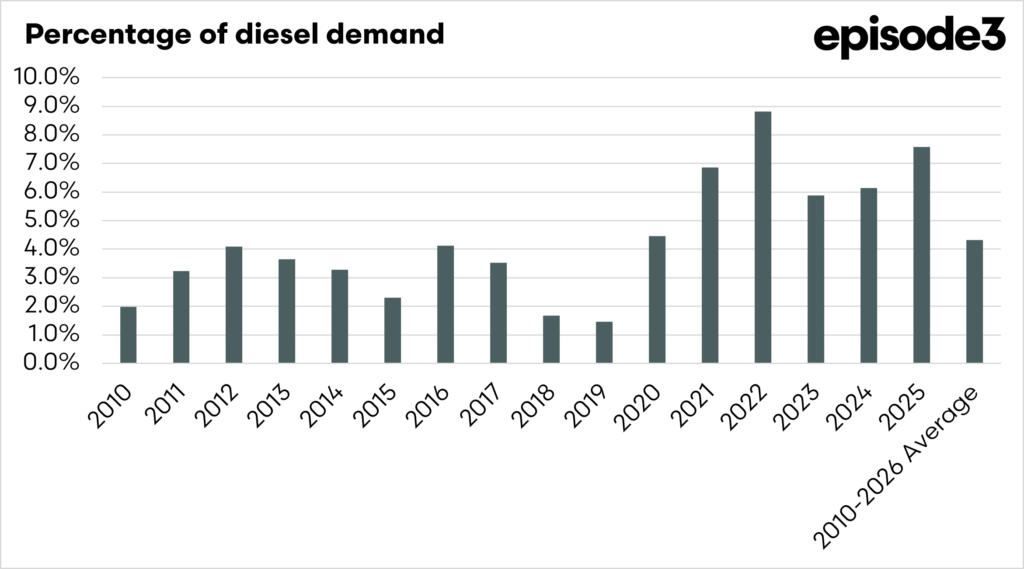

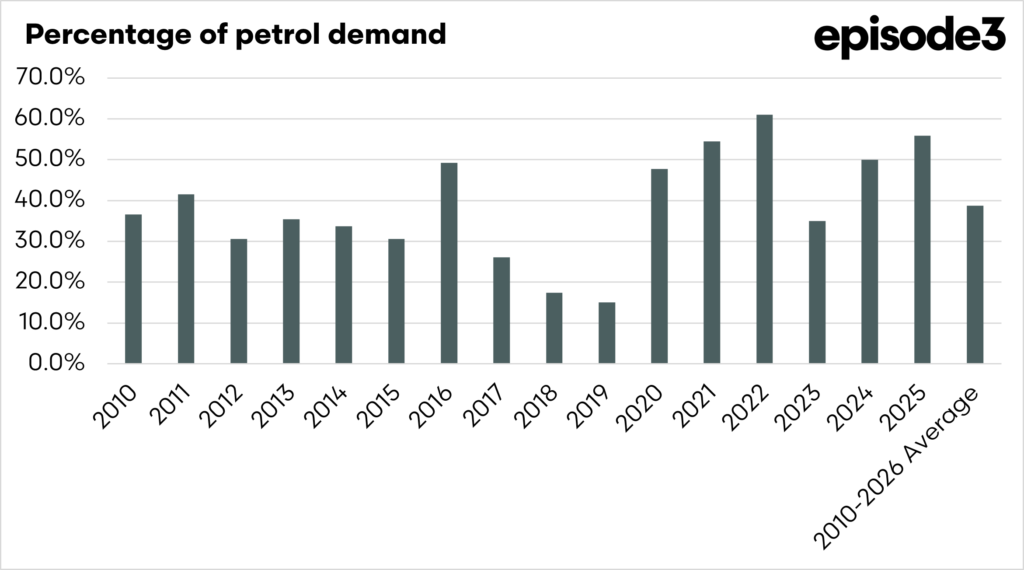

If we converted all the grain and oilseeds which we produce into biofuels, which is not realistic but useful as a theoretical experiment, we would cover just 4.3pc of diesel demand and 38.8pc of petrol demand.

The Scenario Analysis

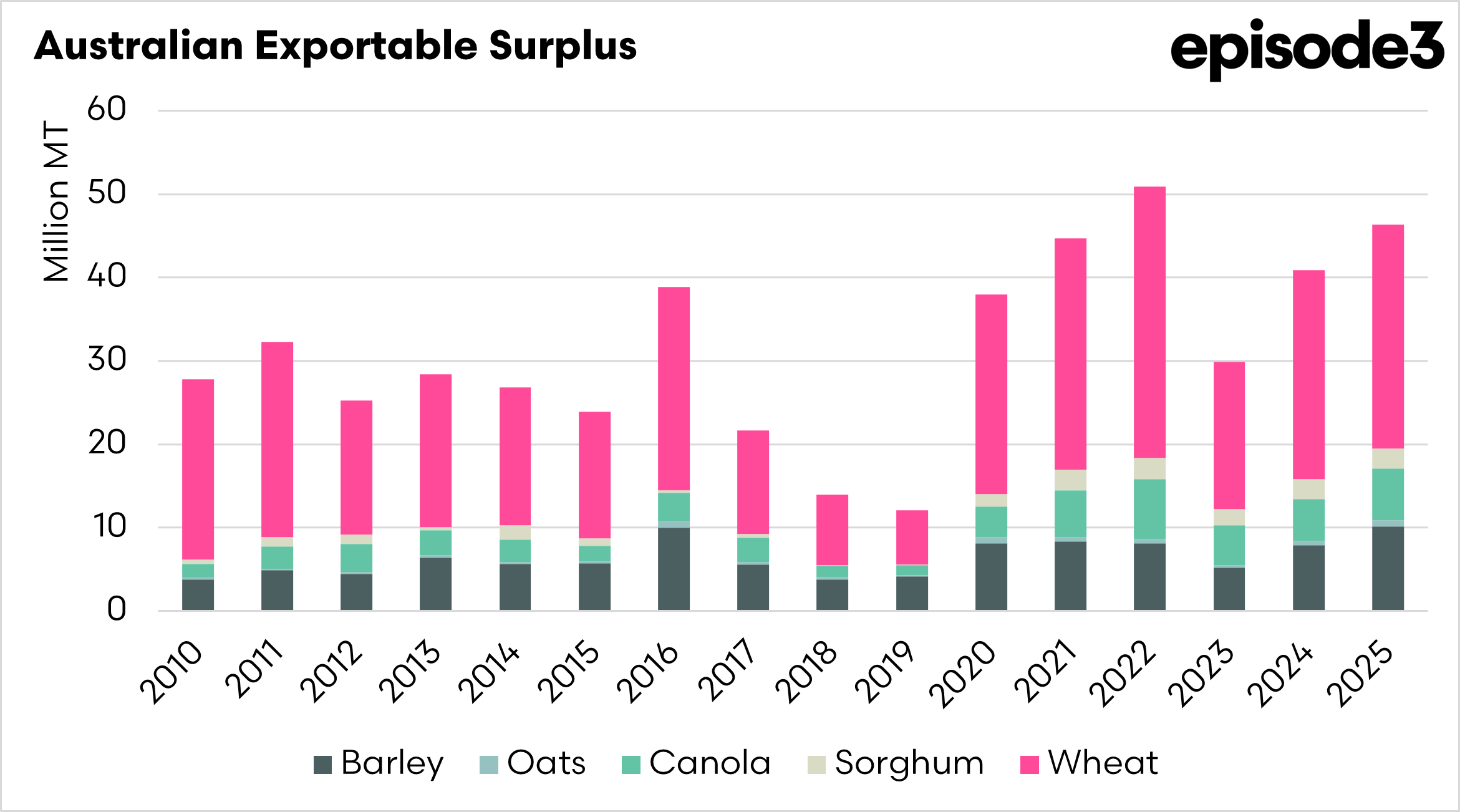

No one is seriously arguing that Australia should divert 100pc of its exportable grain to fuel. We have overseas customers, long-term trade relationships, and a farming sector whose income depends on export markets. It is worth showing the full theoretical maximum to demonstrate the absolute maximum assistance which biofuels could provide to fuel security.

If we look at the average exportable surplus over the period 2010-2025, and we put all of that canola into biodiesel, we would produce 4.3pc of our demand, barely enough to meet the need. Throw every other grain crop at ethanol, and you cover 38.8pc of petrol demand. That is without any exports of grains/oilseeds.

The reality is that we would never convert 100pc to biofuels, but we can look at some realistic policy levels. A 10pc diversion of canola covers 0.4pc of diesel demand. A 20pc diversion covers 0.9pc.

We cannot canola our way out of a diesel crisis at any scale that is remotely realistic, even if we dismantled our export markets.

Trading one risk for another.

Australia’s fuel vulnerability is a supply chain concentration problem, caused by conflict in the Middle East. Redirecting grain and oilseeds to domestic fuel production would replace it with a weather risk.

The annual data make this plain. In 2019, a drought year, total fuel displacement fell to around 1.5pc of national diesel demand. In 2022, a bumper year, it rose to 8.8pc. That is a fourfold swing driven entirely by weather. This adds a further layer of volatility to an already volatile fuel system.

Should we build a biofuels industry?

This article might sound negative towards the biofuels industry in Australia. This is not the case; a biofuels industry would be fantastic for farmers’ margins, but we shouldn’t pretend that it would solve the fuel crisis.

Australian grain growers have two markets for grain: a small domestic market and the export market. When global prices fall, growers bear the brunt. A domestic biofuel refinery creates a second buyer with a different demand driver. That competition, even at a modest scale, sets a floor for farm-gate prices. For individual growers, that is a tangible and recurring benefit that will drive margins.

The economics of biofuels also improve over time. Biofuels currently cannot compete with fossil fuels without subsidy support. As carbon pricing matures, as oil prices trend higher, and as scale reduces unit costs, the gap narrows.

The bottom line

Australia should have a biofuels sector. The government’s A$1.1 billion commitment to clean fuels and related programs is a reasonable start.

Biofuels will not save Australia in case of current or future fuel supply shocks. The fuel we are most exposed to is diesel, the driver of freight, mining and agriculture. Our entire exportable canola crop, converted entirely to biodiesel, covers 4.3pc of that demand. Even the theoretical ceiling of 8.8% total displacement requires exporting zero canola and relies on a bumper harvest.

Biofuels have a role in Australia’s energy future. That role is real, worth investing in, and will matter more over time. We should build this industry with clear eyes about what it can and cannot do and stop overselling it to farmers and the public as the panacea to the energy crisis.