Aye, Grain: The Weekly Grain Wrap

The Snapshot

- Global grain markets rallied after weeks of drifting lower, with US weather concerns and renewed Chinese soybean buying giving traders something fresh to focus on.

- Corn led the charge, supported by hot, dry conditions during the critical US pollination period and deteriorating maize prospects across Europe following recent heatwaves.

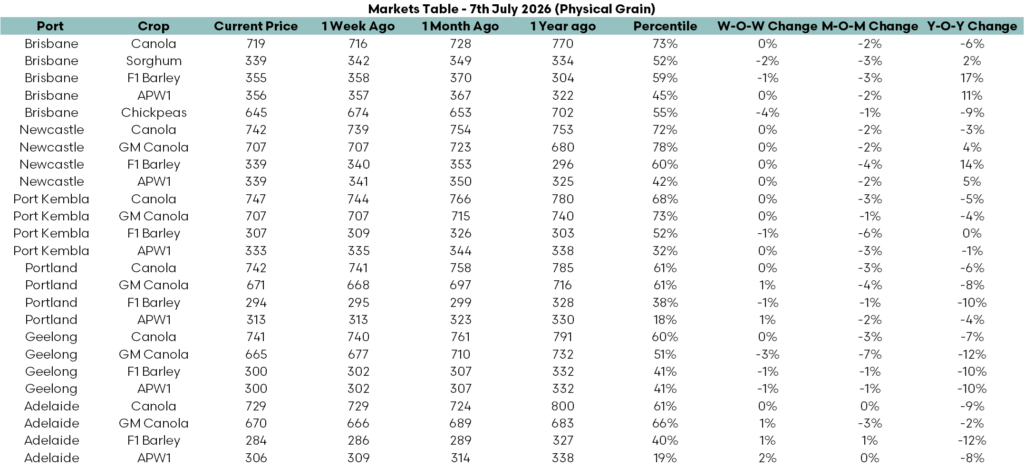

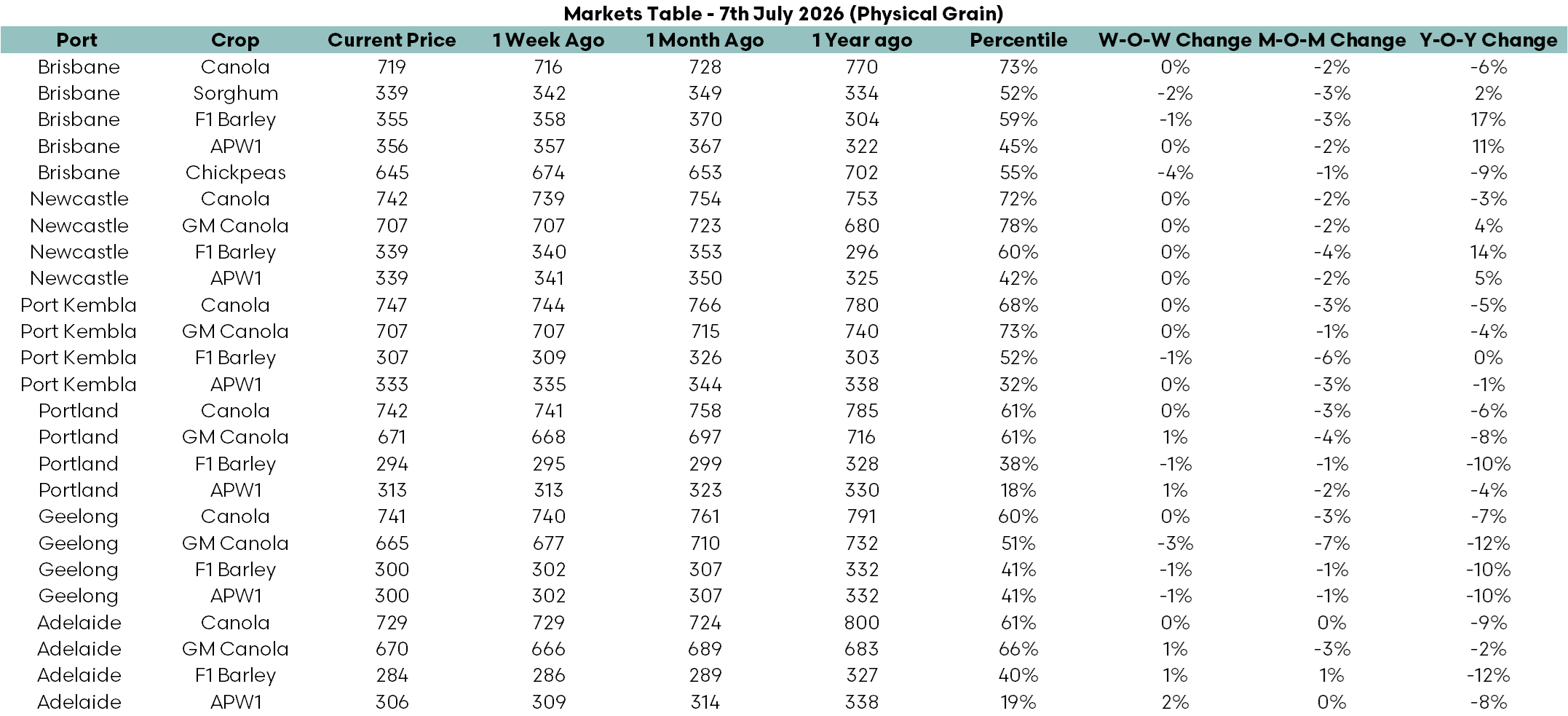

- Australian grain prices remained subdued, as widespread winter rainfall and improving crop prospects across much of the country continue to cap local values despite stronger international futures.

- The Black Sea remains the key wheat battleground, with another large Russian harvest weighing on prices, while escalating attacks on Ukrainian ports threaten to disrupt exports and lift freight costs.

- Growers received more positive news on the cost side, with urea prices falling again as Middle Eastern fertiliser exports recover, although diesel and petrol prices edged higher during the week.

The Detail

Global grain markets finally found a pulse this week. After drifting lower for weeks, traders had something to work with: US crop weather, European heat and signs that China may be stepping back into the US soybean market.

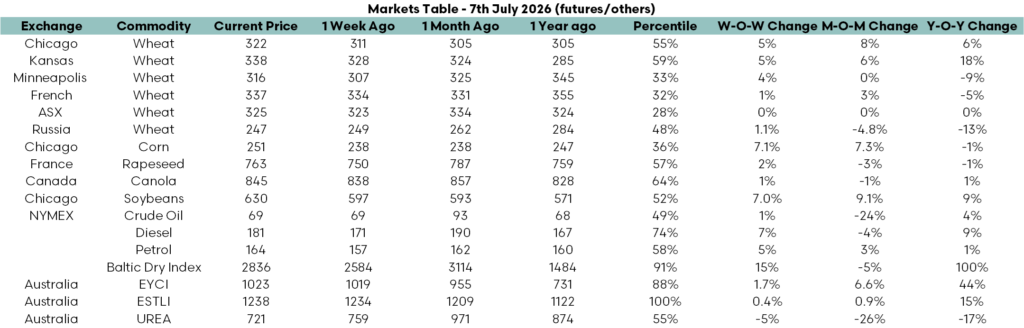

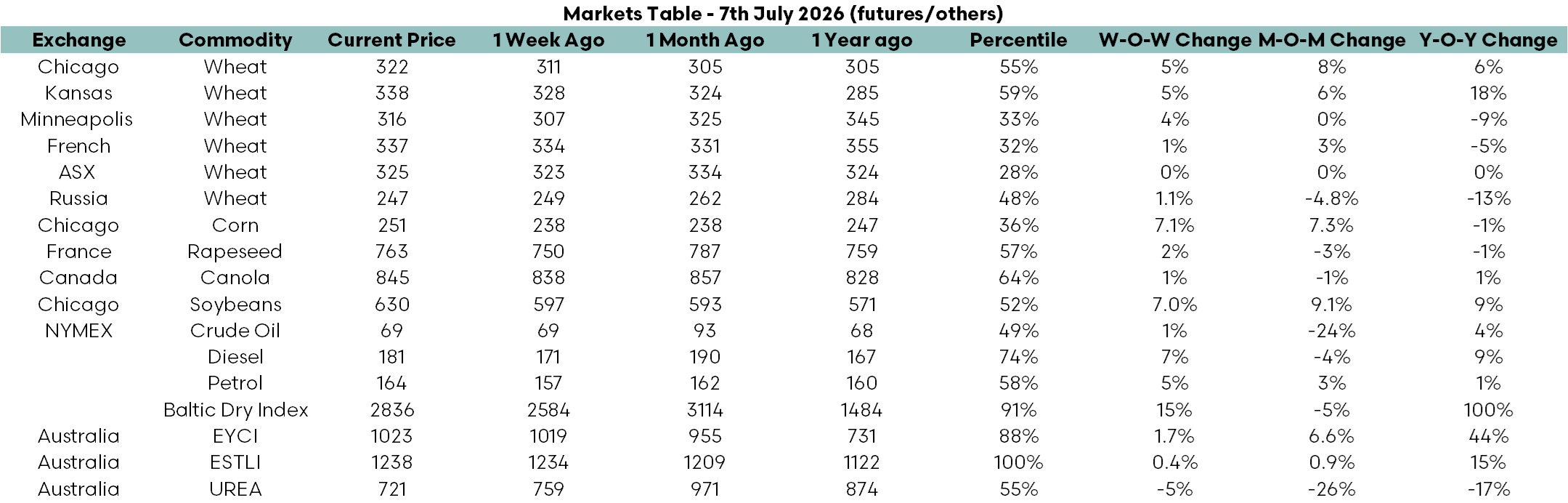

Corn and wheat follow each other, and corn did the heavy lifting. Chicago corn futures jumped almost 9 per cent over the week as forecasts turned warmer and drier across parts of the US Midwest, just as the crop moves into pollination. That is not a period when the market likes to see heat. Europe added to the concern, with recent hot weather hitting maize prospects and French crop conditions falling to their lowest level in more than a decade.

Soybeans followed, helped by reports that Chinese buyers had booked at least 300,000 tonnes of US soybeans. That was enough to lift prices more than 5 per cent for the week. After weeks of thin demand stories and heavy fund selling, even a modest Chinese bid was always going to get attention.

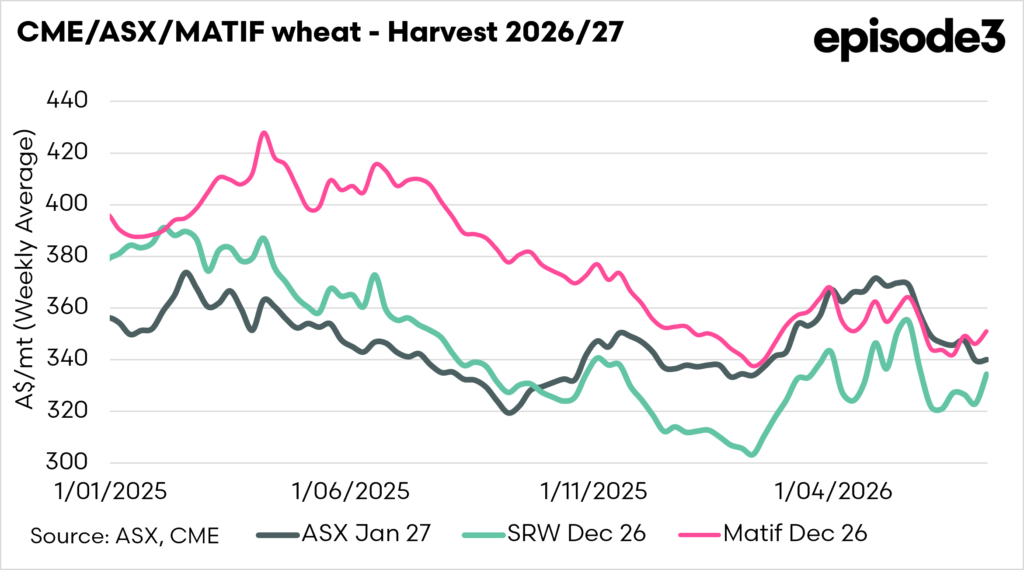

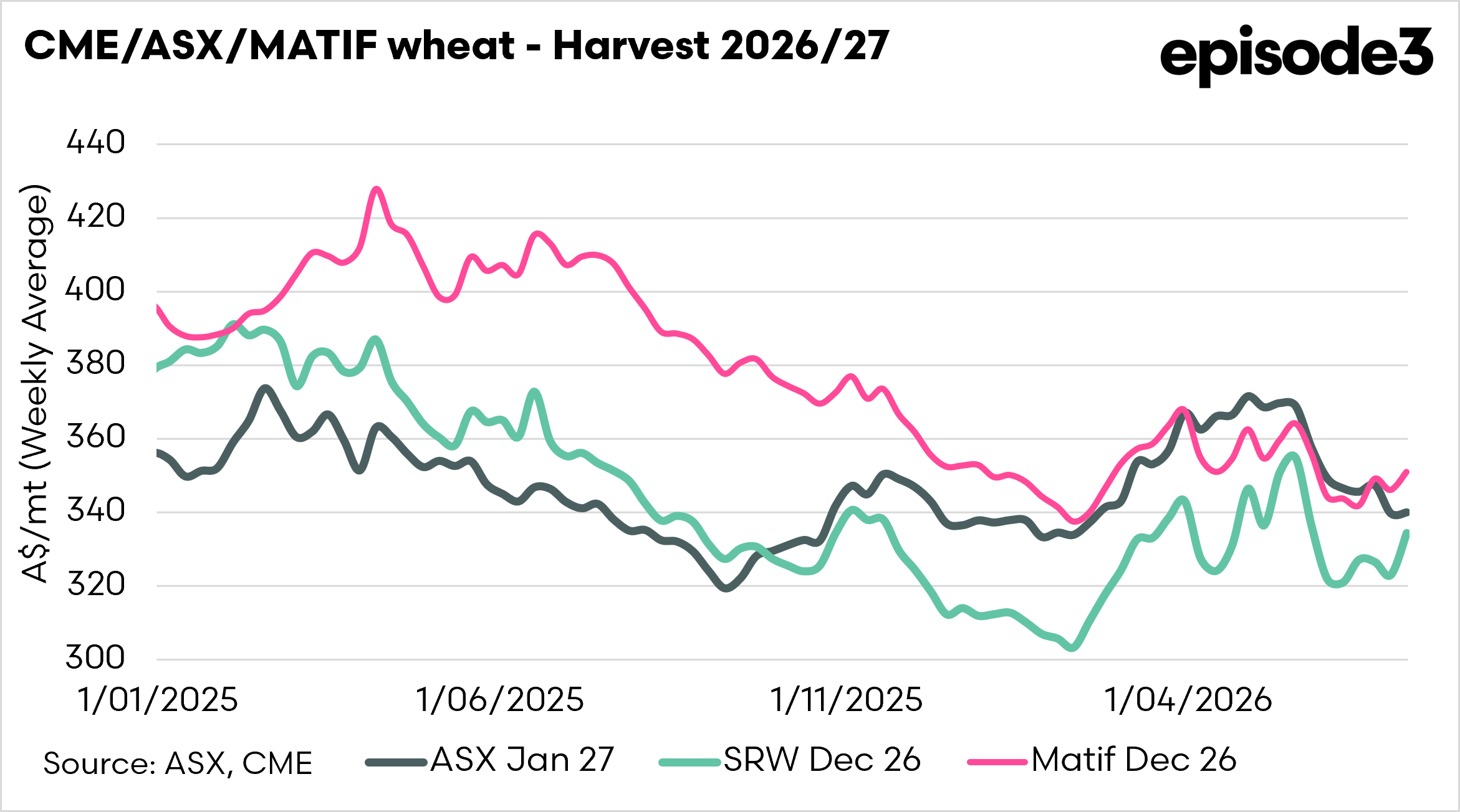

Wheat joined the rally, but it was not really leading it. Strength in corn and soybeans helped, as did Saudi Arabia’s latest wheat tender. The problem for wheat is still Russia. Another large Black Sea crop is coming, Russian export values eased again during the week, and the world’s cheapest major supplier is still setting the tone.

That said, the Black Sea is not a clean bearish story. Ukraine has warned that increased Russian attacks on ports, vessels and export infrastructure could cut monthly grain shipments through the Odesa corridor by as much as one-third. Ukraine accounts for around 6 per cent of global wheat exports and 11 per cent of global corn exports. If that flow gets disrupted for any length of time, the market will have to care. Freight would lift, risk premiums would widen, and buyers would start asking harder questions about execution.

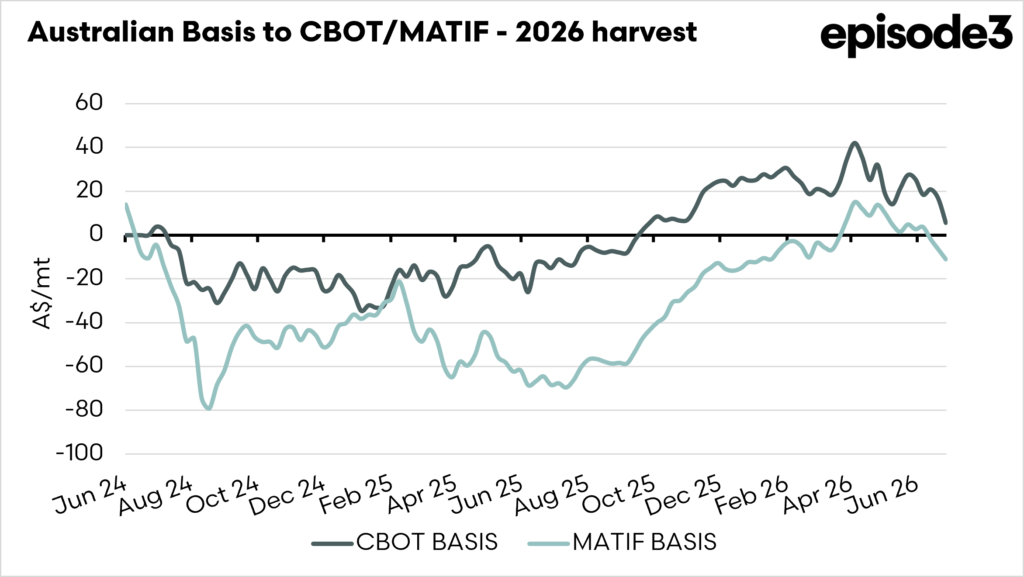

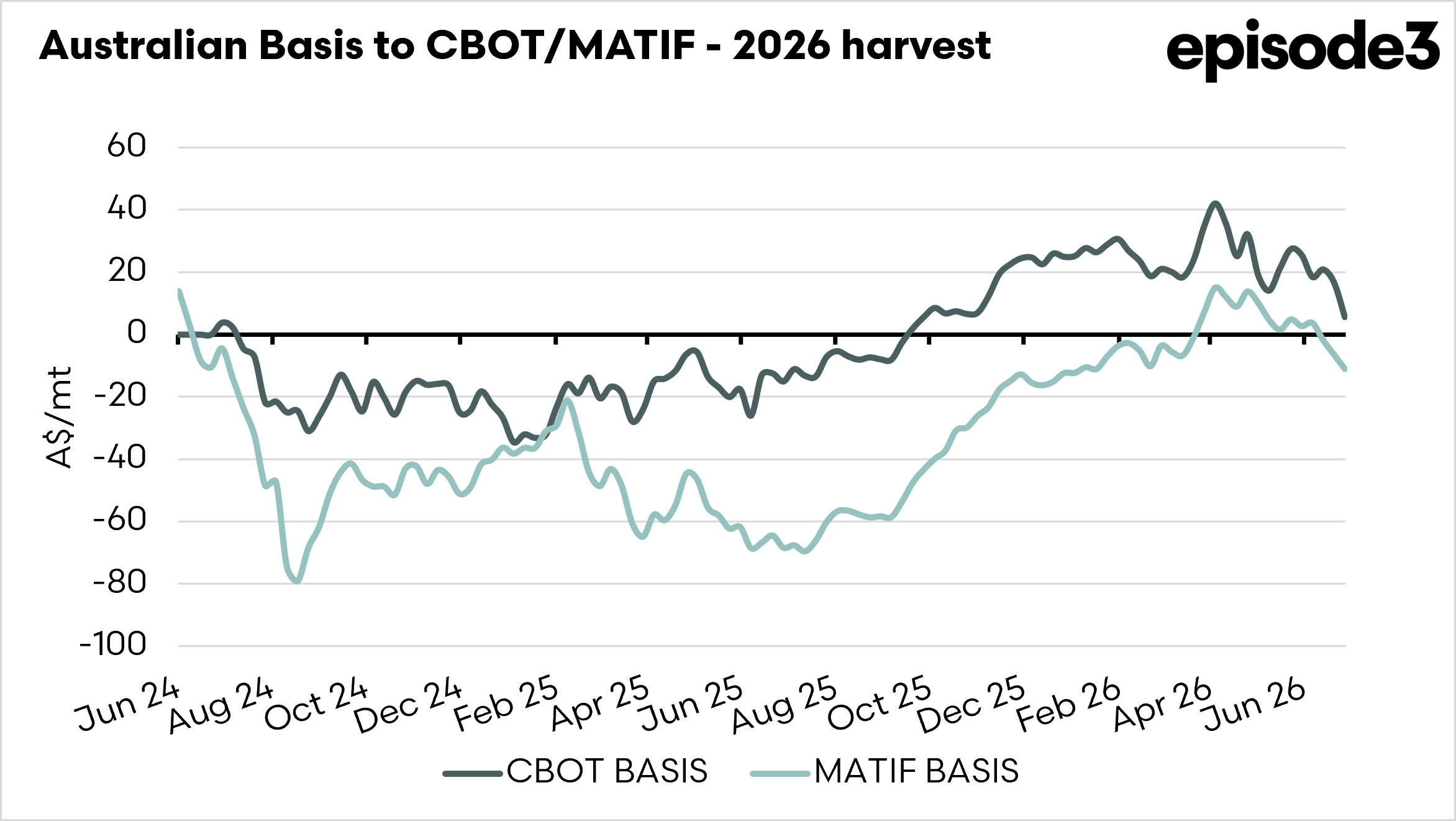

Locally, the attention has been on the Australian weather maps. Recent rain across New South Wales, Victoria and parts of South Australia has improved production prospects again, while much of Western Australia is still in decent shape after useful winter rainfall. That is good news in the paddock, but it has taken some urgency out of the local cash market.

The pricing table clearly shows the split. Chicago wheat finished the week 5 per cent higher, corn lifted almost 9 per cent, and soybeans gained more than 5 per cent. Australian physical wheat values barely moved, with most east coast APW prices unchanged to slightly lower. Barley was generally softer. Canola also failed to fully follow offshore oilseed strength.

The cost side is where growers are getting the better news. Australian urea prices fell another 5 per cent during the week and are now 26 per cent below a month ago and 17 per cent lower than a year earlier. Shipping through the Strait of Hormuz has improved, Middle Eastern exports are recovering, and Australian import programs have done enough to calm the supply panic.

Fuel is less friendly than fertiliser this week. Diesel and petrol bounced, although crude oil is still well below the highs reached during the Iran conflict.

For growers, the market message is pretty blunt. Offshore futures have found weather risk again, but local prices are not chasing while the Australian crop keeps improving. The rallies that matter will be the ones that survive a decent local production outlook, not just a hot week in Chicago.