Fast forward to harvest.

The Snapshot

- It’s time to start looking forward to harvest pricing for wheat.

- Typically at harvest, Australian wheat trades at a premium to overseas futures.

- At present forward physical prices are trading at a negative throughout large tracts of the country.

- You can sell physical and lock away your fx, futures and basis.

- Alternatively, you can lock you futures (and fx), and only be exposed to basis.

The Detail

The focus is now firmly on the coming harvest. The seeding rigs around the country are either in operation or getting set up. Whilst the job at hand is getting the seed drilled into the ground, the marketing task starts (if not already).

In an earlier morsel today, I had a look at basis around the country for old crop. Whilst this is important for those remaining onto old crop, its not much value for looking down the horizon to harvest.

Basis or futures?

The majority of farmers in Australia don’t use futures (or swaps), they use flat price contracts. Flat price is the physical price which you are offered, which combines futures, fx and basis. However at times it is an effective solution to separate your pricing.

There are many strategies, but at its most basic, if basis is low, sell futures and if basis is high sell physical.

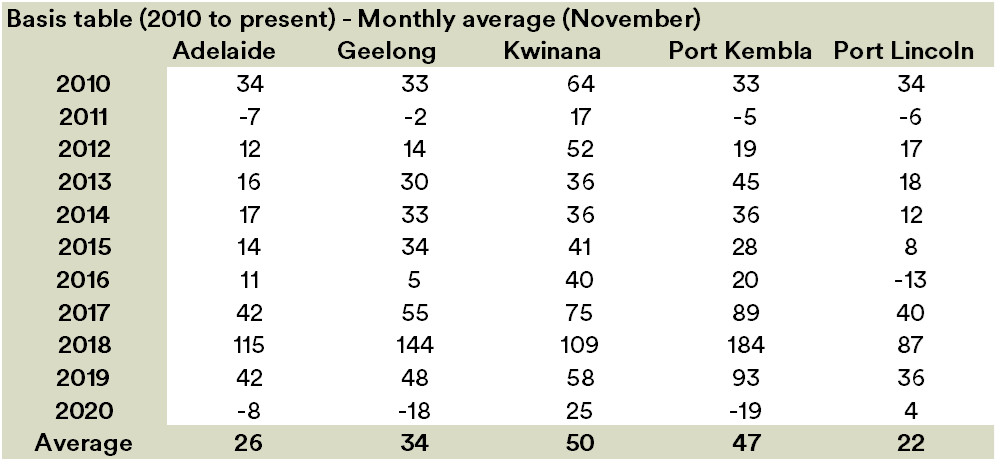

The table below shows the historical basis between Chicago wheat futures and local physical pricing for APW during November.

Whilst basis does move between positive and negative, generally, harvest basis has been at a premium for most of the period 2010 to present.

Forward to the future

So at this time of the year its worthwhile looking forward to harvest, and considering your sales strategy.

If making sales, you can look at either the flat price, or the separate components. This will give you a clue to whether you sell physical or futures.

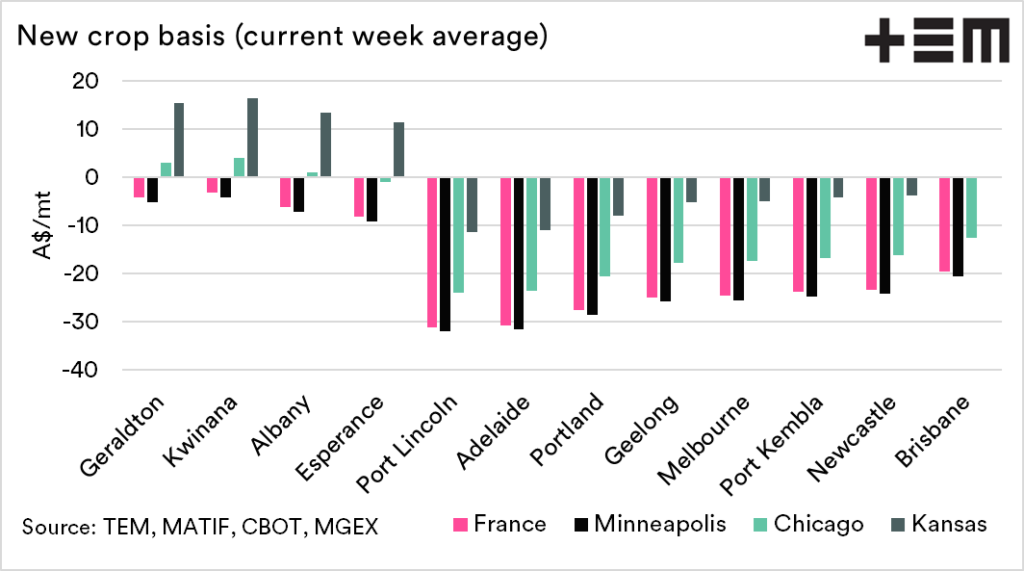

The chart below shows the current basis level between the futures prices which correspond with our harvest, and local APW pricing.

I have included four futures exchanges, in the case of this article all offshore. These are Minneapolis (MGEX), Paris (Matif), Chicago (CME) and Kansas (CME).

We can see that the basis between physical and the various exchanges is considerably lower than the basis which would typically be received during the harvest period.

So what are the strategies?

There are many different strategies that can be used for marketing grain, for both pre and post harvest.

- Lock in physical contract with trader. This will lock in all the components of pricing, fx, basis and futures. This will remove all risks to do with pricing, and you have absolute certainty of the price which you will receive.

- Sell futures at the prevailing rate either directly through a broker or a swap through the bank. This will protect you from the futures (fx*) price falling, but will leave you exposed to basis.

If basis falls further, then you will lose. Still, suppose basis rises to return to typical levels. In that case, you will receive that benefit when you come to close your futures and sell physical at harvest.

Strategy 1 will leave you without any price risk, and no further thinking. Strategy 2 retains some risk, but the potential for leaving less on the table. It will come down to risk appetite which strategy is used.

*FX can be left open or locked in, but that is a discussion for another day.