Grains remain on the uncertainty roundabout

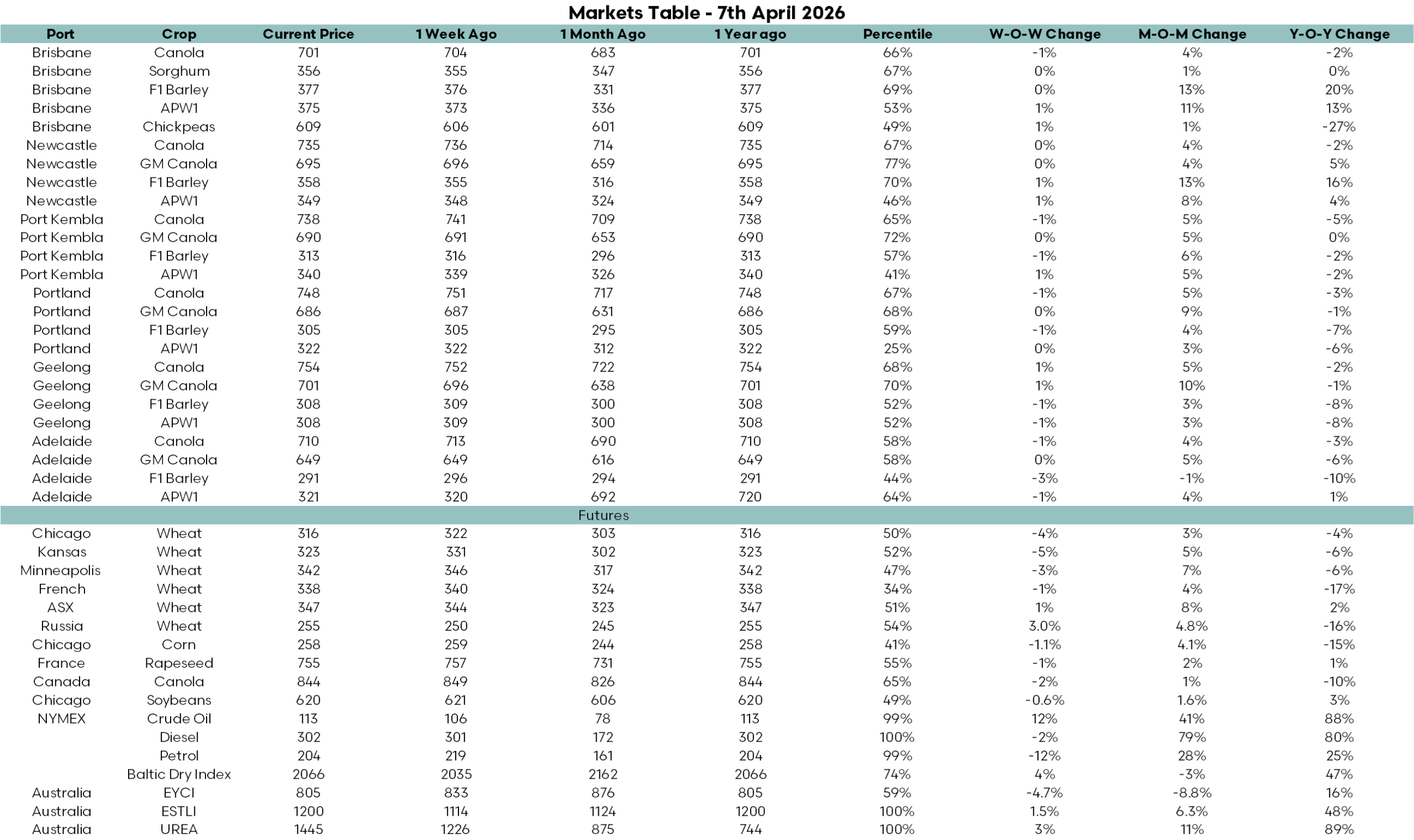

Global grain markets have softened over recent sessions, as a shift in both weather outlook and macro sentiment has removed a layer of support that had been building through March.

Last week, there were concerns with much of the US wheat crop, but Chicago futures eased back as forecasts point to timely rainfall across key parts of the US Plains.

After an extended period of dryness, rainfall is now expected across roughly half of the hard red winter wheat belt over the next 10 to 15 days, particularly across the eastern two thirds of the region. Turning it from a bullish market to a neutral market.

This has quickly altered market sentiment, prompting funds to unwind long positions built on weather risk and geopolitical uncertainty.

The sell-off has been notable, with wheat futures falling back toward recent lows as both premiums were stripped out simultaneously.

Despite this, the underlying condition of the US crop remains concerning.

The first USDA crop progress report for the 2026 season rated winter wheat at just 35pc good to excellent, well below expectations of 42pc and down from 48pc last year.

Around 65pc of the crop remains in drought-affected areas, highlighting that while rainfall is forecast, the production outlook is still far from secure.

The market is now balancing improving forward conditions against historically weak starting ratings, leaving it highly sensitive to any change in the weather outlook.

At the same time, macro drivers remain a factor.

There has been back-and-forth: it looked like a ceasefire would be announced, then it looked distant again.

This potential easing of tensions could remove a key pillar of support for agricultural markets, particularly for crops tied to biofuel demand such as corn, soybeans and canola. The reality is that we will be on the roundabout of uncertainty for some time.

Global supply remains another limiting factor.

Russian wheat exports continue to run aggressively, with March shipments estimated at around 4.6 million tonnes, reinforcing the weight of supply in global markets.

Demand remains relatively steady, suggesting the recent move lower is being driven more by weather and macro positioning than by any deterioration in consumption.

For Australia, these global shifts are beginning to feed into local pricing, although the domestic market remains relatively resilient.

Wheat is expected to track offshore weakness, while canola has also come under pressure as vegetable oil markets ease alongside crude oil.

There are reports of some early new crop sales, we believe that volumes are unlikely to be strong as producers weigh up costs versus the price they receive for their crop.

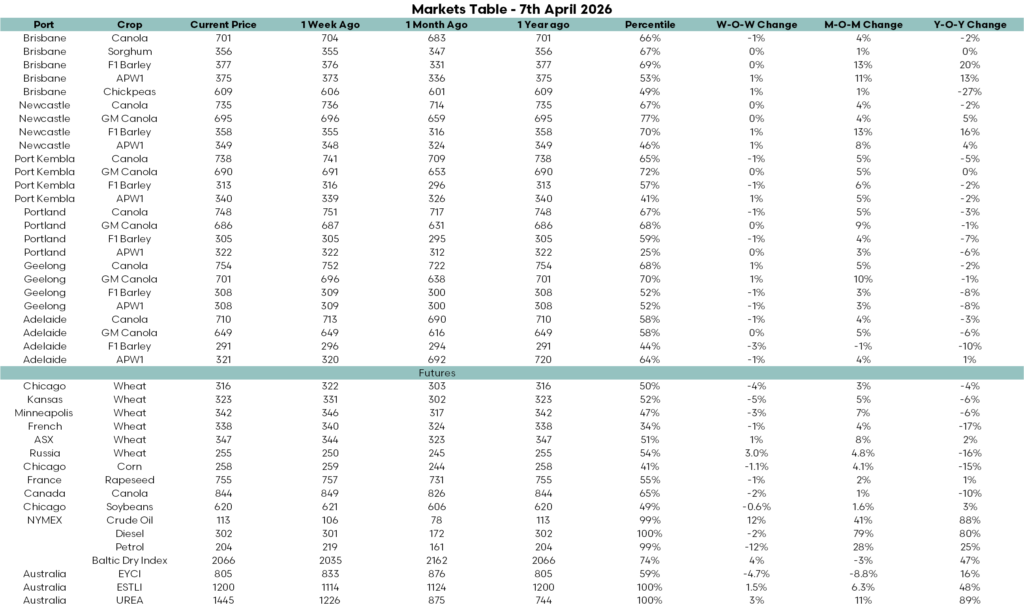

The updated pricing data across Australian ports reflects this balance between softer global sentiment and firm domestic fundamentals.

Week-on-week moves are generally flat to slightly lower, but month-on-month strength remains evident across most commodities.

Brisbane APW1 is up 11pc month on month and 13pc year on year, while Newcastle and Port Kembla show similar gains, particularly across wheat and barley. These are the areas closest to the major demand areas.

Feed grain markets remain supported, with F1 barley up strongly on a monthly basis across most ports, including gains of around 13pc in Brisbane and Newcastle.

Canola prices have eased slightly week-on-week but remain elevated in historical terms, generally sitting in the 60th to 70th percentile range.

Across the southern ports, Geelong and Portland reflect a similar pattern, with modest short-term softness but underlying strength still intact.

Costs remain the main talking point among producers in an environment where energy and input costs are elevated, with crude oil, diesel, and urea all near the top of historical ranges, reinforcing cost pressures across the supply chain.