Somewhere over the rainbow

The Snapshot

- The forward curve represents the horizon for a futures markets. It shows each trading expiry date.

- The market can be in either contango or backwardation.

- A market in contango is where the forward months are trading at a premium to present; backwardation is the opposite.

- The wheat market has tended towards contango in recent times.

- The market tends to pay ‘carry’ or a premium for forward months.

- There are some historically attractive futures levels on the current horizon.

The Detail

We are into July, and it might be time to start thinking of your marketing program if you have not already started.

The marketing of grain is for many, not in front of mind. However, marketing is an activity which should be conducted in advance, during and after harvesting.

Managing your grain sales allows you time for other activities that arise and to mitigate the risk of adverse movements.

A tool worth using is the forward curve. The forward curve is a chart which we will often refer to in EP3 articles, as it provides a quick view of the market. The forward curve details the price for each of the contract expiry dates for the futures contract of a commodity.

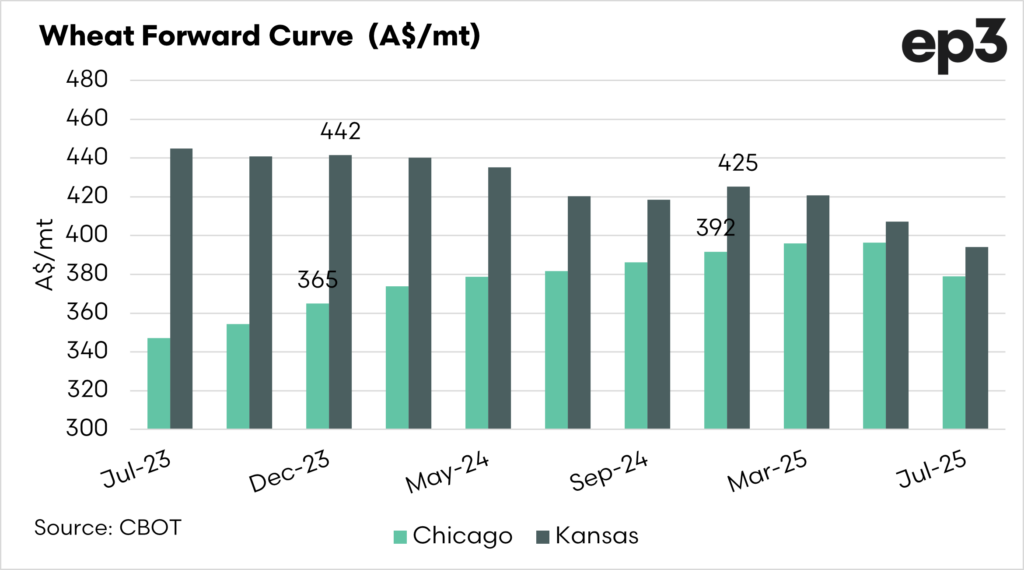

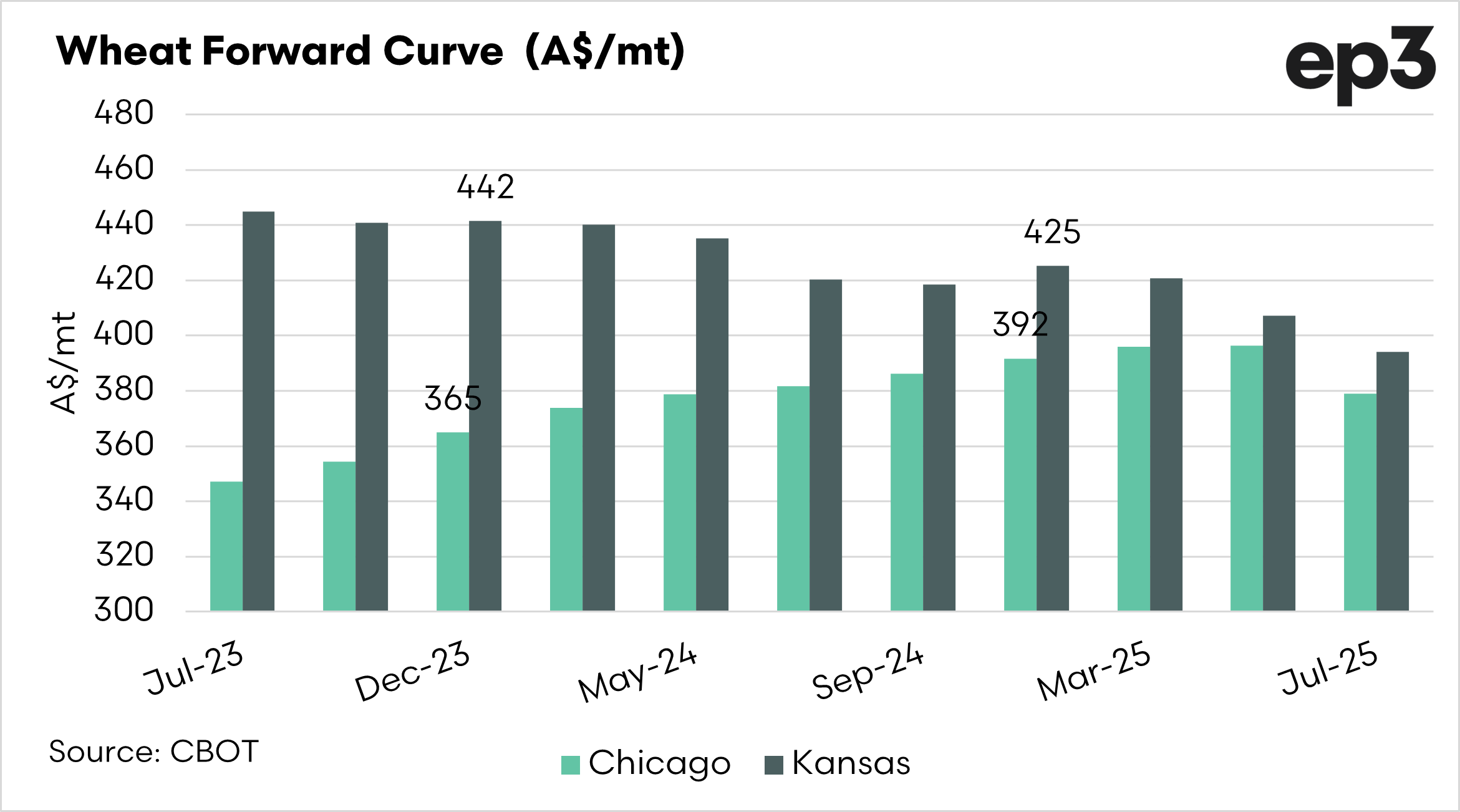

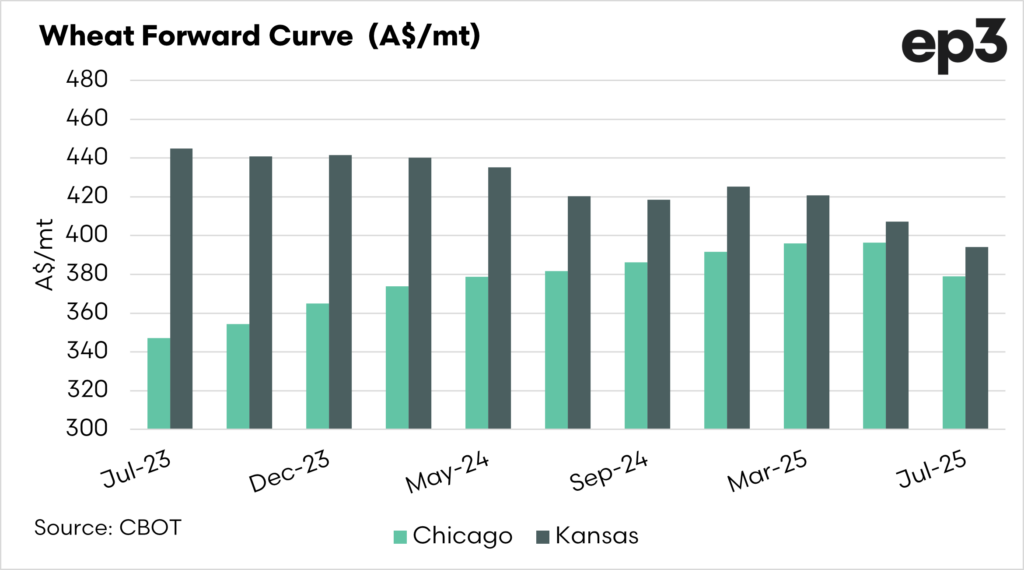

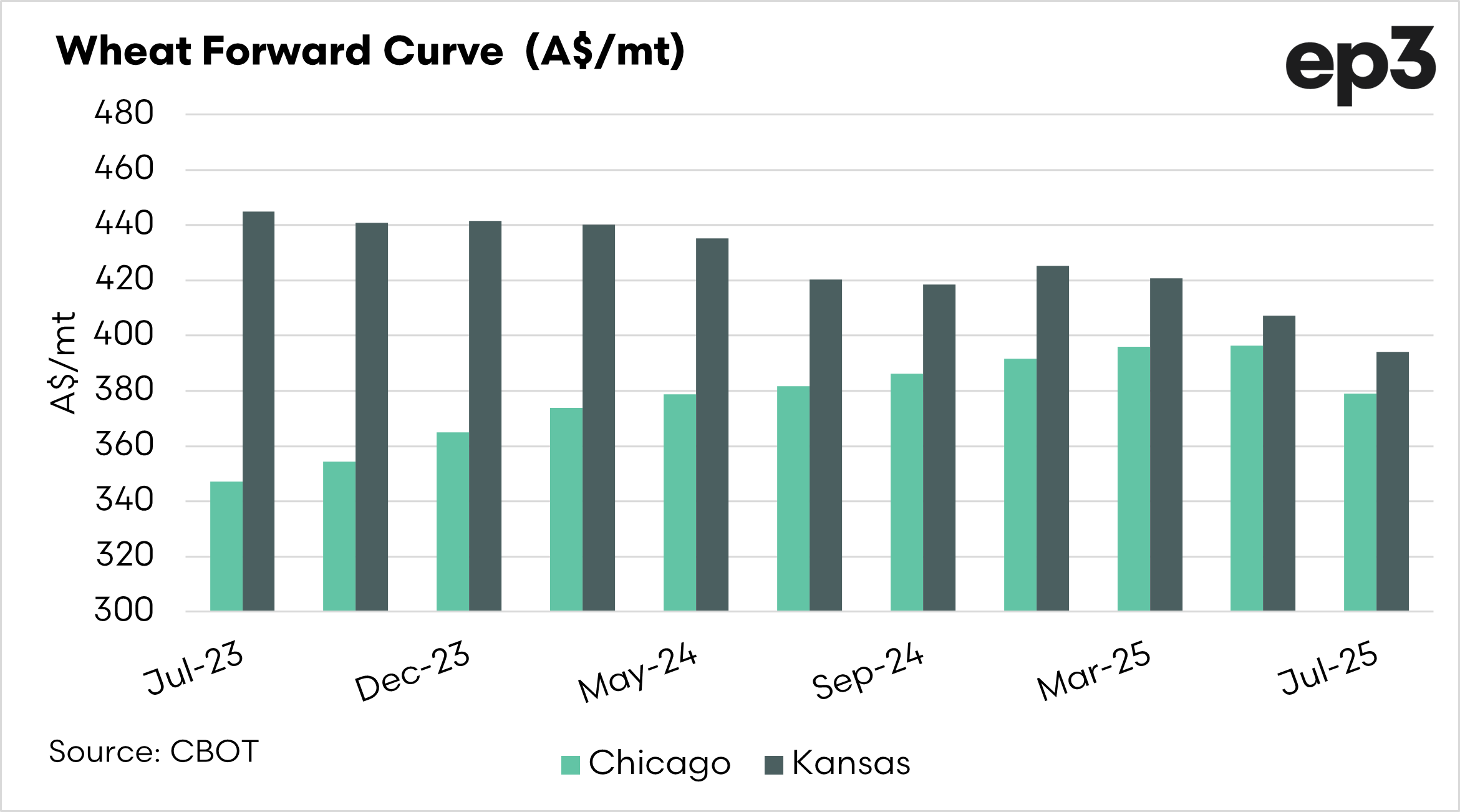

The curve gives an instant snapshot of where you could theoretically buy or sell the commodity. The below chart displays the forward curve for Kansas & Chicago wheat converted to A$/mt.

The forward curve can be in either contango or backwardation. In typical financial/economic gobbledygook fashion, the terms sound more complicated than reality. Although there are a range of economic theories behind contango and backwardation, I’ll try to explain them succinctly below.

Contango:

A forward curve is in contango when the forward futures months are at a premium to the spot level. In the above chart, the market is in contango, as each of the months ahead is higher than the September contract.

The futures market in contango is effectively paying a premium for the seller to carry the crop.

Backwardation:

As you might expect, backwardation is the opposite of contango. The forward curve is in backwardation when the forward market is trading at a discount to the spot market.

When in backwardation, the market is effectively wanting access to grain as soon as possible and does not want to pay you to carry the grain.

How to use it as a farmer?

The wheat futures tend to be in contango and effectively provided a premium versus spot. This offers the opportunity to lock in futures on the forward curve i.e beyond the current harvest at a premium to spot.

It is important to note that the price can (and will) change between taking out a contract and when it expires. However, if you are locking in a price that you are happy with, then that becomes less of an issue.

In the chart below, I have highlighted the December contract for this year and next, because this is the time period that we are generally looking at, as it coincides with the Australian harvest.

We can see that we can lock in A$365/442 for this year and A$392/425 for next year. I have included both Kansas and Chicago, as these are two (of many) options which farmers have for hedging their wheat.

It is important to note that basis has to be taken into account. Typically our basis is a premium, but it can and has recently been a negative. The potential for a negative basis has to be taken into account when looking in futures contracts.

That being said, these are some pretty high futures levels for a long time horizon.