Better pricing, stronger yarding

Market Morsel

The National Heavy Steer saw a low of 200c/kg lwt in mid October 2023, but prices have recovered through the end of 2023 and have opened 2024 around 44% higher than the October trough holding at around 287c/kg lwt through mid-January. It is a stronger story of recovery for the National Trade Lamb Indicator, peaking in mid-January at 775 c/kg cwt which equates to an 86% lift from the low seen in early September 2023 of 411 c/kg cwt.

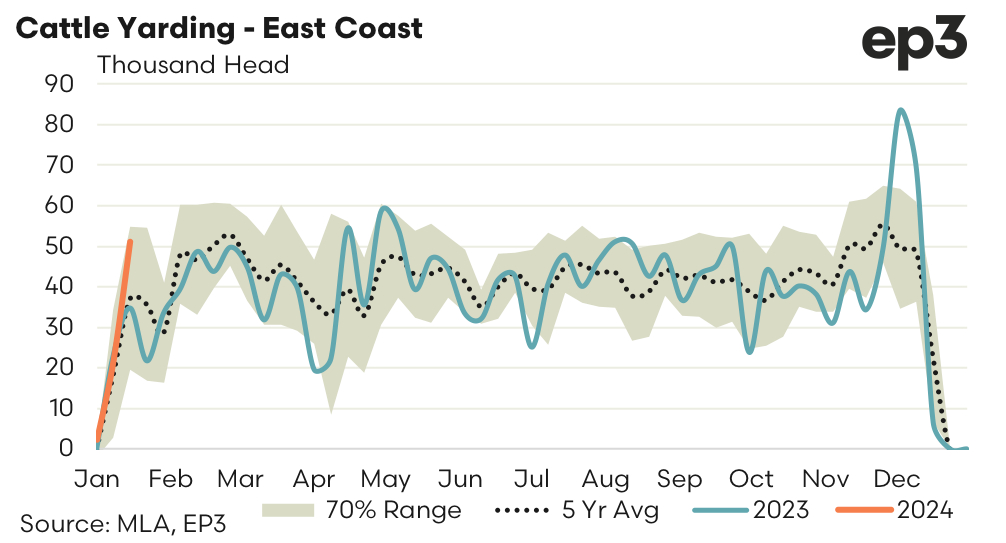

The improved pricing structure has been noted across cattle, sheep and lamb categories at the saleyard and it is encouraging some strong opening weekly yarding figures for the east coast saleyards. East coast cattle throughput for the first few weeks of January 2024 have come in 26% higher than the levels seen during the start of 2023 and 31% higher than the seasons opening average trend based on the last five years of weekly throughput data.

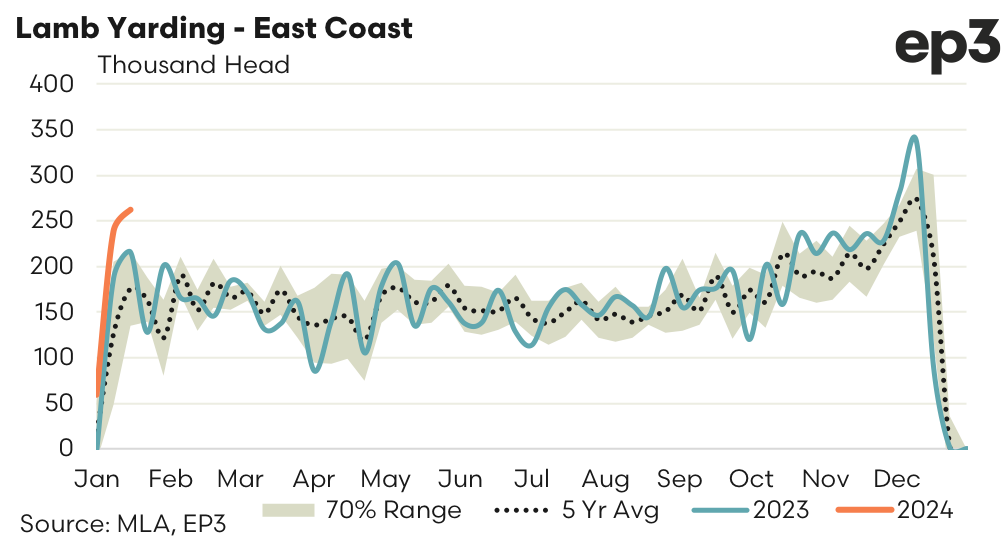

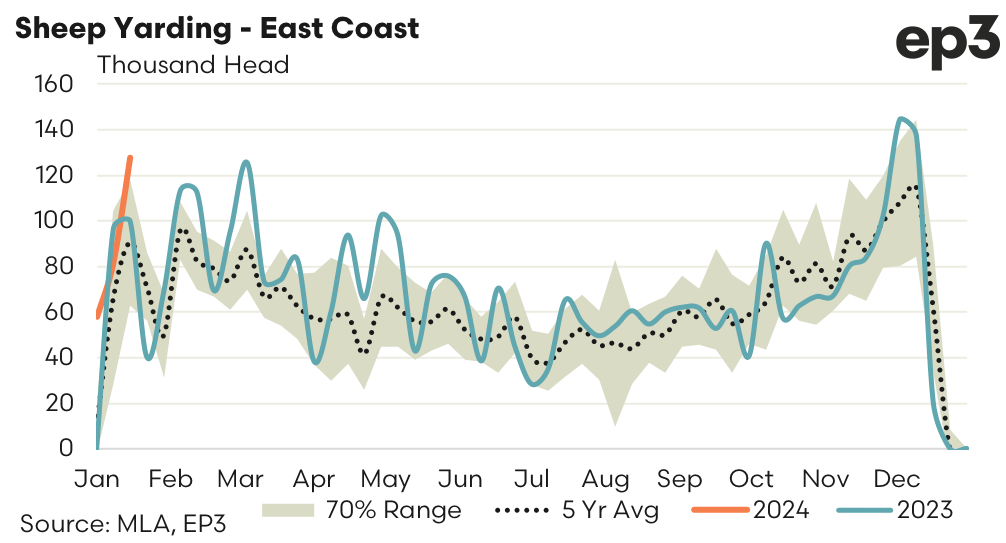

It is a similar strong start for lamb throughput volumes with the first few weeks of January 2024 coming in 24% higher than January 2023 and 65% higher than the five-year average pattern for the first few weeks of January. Meanwhile, east coast sheep yardings have started 2024 around 7% higher than the first few weeks of 2023 and 34% above the five-year average sheep yarding levels for the early January saleyard opening.