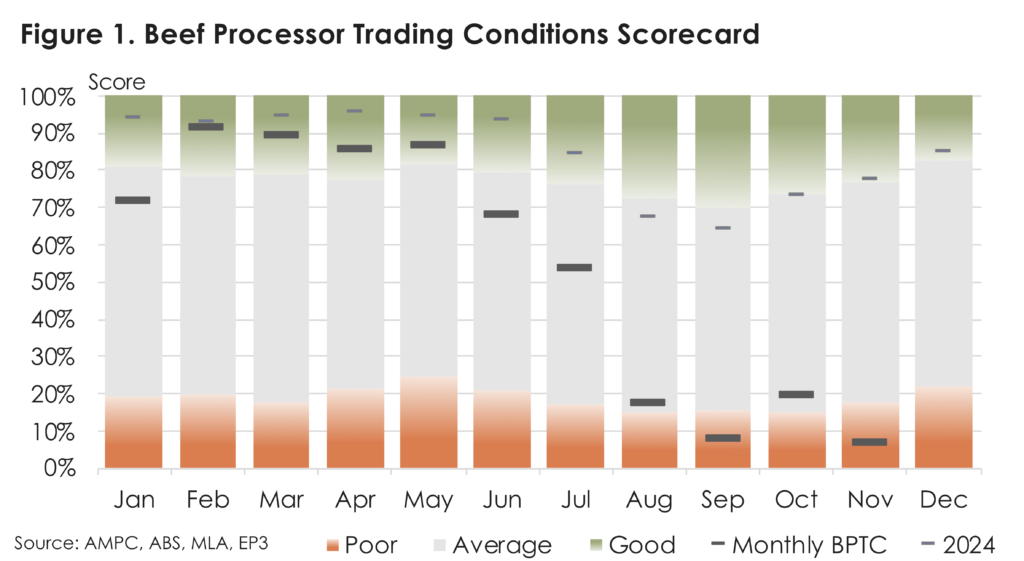

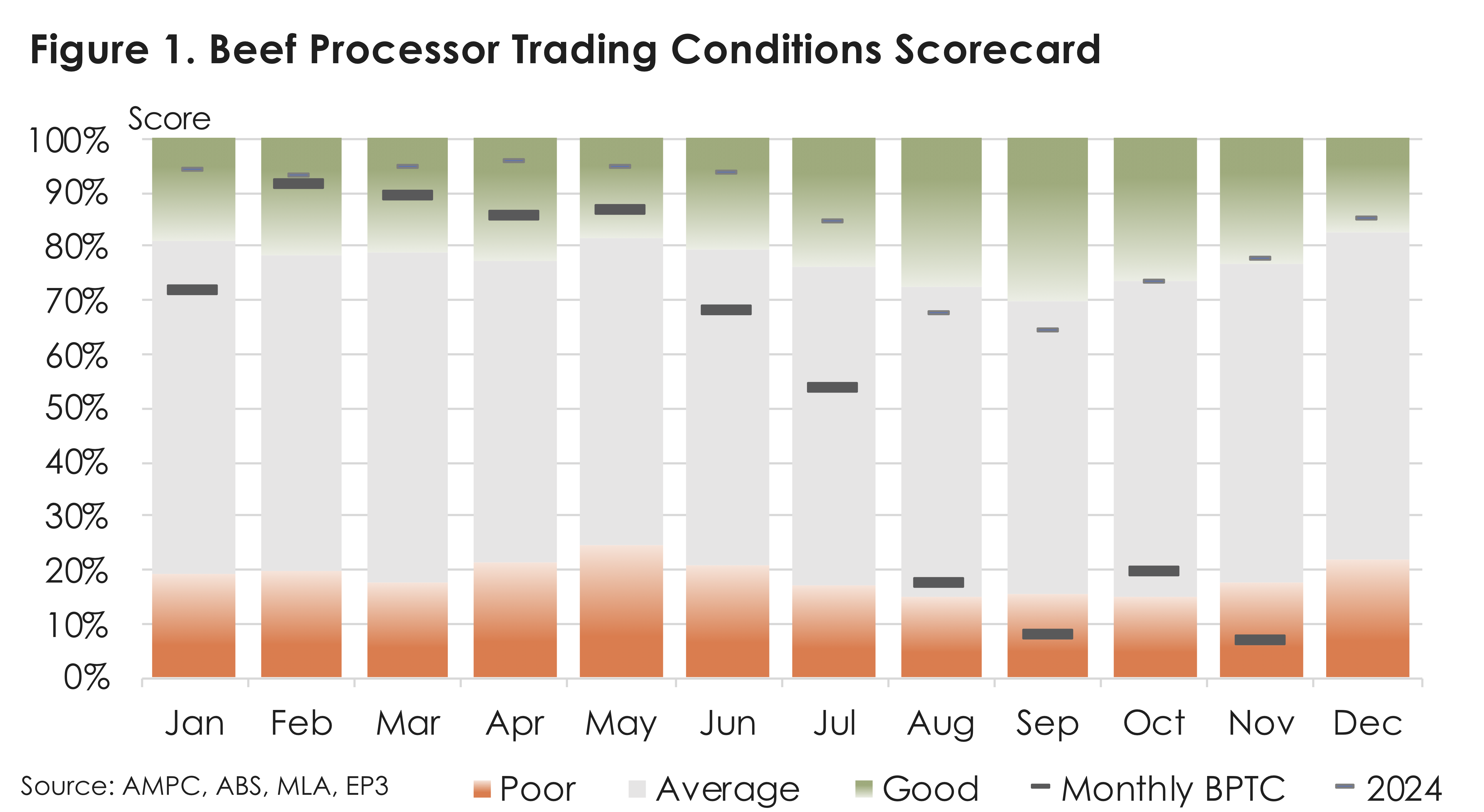

Choppy finish for beef processors

Beef Processor Trading Conditions Update

Processor margins came under renewed pressure in November as a sharp rise in livestock procurement costs outweighed only modest improvements in selling prices across export and domestic markets. The latest movements in key variables that feed into the BPTC index highlight how quickly trading conditions can tighten when cattle prices move higher without a corresponding lift in downstream returns.

The most significant shift through November occurred on the input side of the ledger. Heavy steer prices rose by 5.7 percent over the month, while young cattle values lifted by 6.0 percent and processor cow prices increased by 6.5 percent. These increases represented a broad based rise across all major procurement categories and followed the brief easing that had been recorded in October. For processors, this meant that the cost of securing livestock moved materially higher in a short period of time, compressing margins at the plant level and eroding the modest improvement that had emerged earlier in the spring.

Export market performance provided only partial support, based upon average beef export value trends. Returns into the United States improved by 2.2 percent, while Japan recorded a stronger lift of 7.0 percent. These gains, however, were offset by declines into two key North Asian destinations. Export values to South Korea fell by 1.0 percent over the month and returns into China dropped by 4.1 percent. When combined across the four major offshore beef markets, the overall improvement in export value was limited to just 0.8 percent. This modest lift was insufficient to keep pace with the rise in cattle prices and therefore offered little protection to processor margins.

Domestic factors moved in a more favourable direction but again at a scale too small to materially offset higher livestock costs. Retail beef prices rose by 1.3 percent through November, continuing the gradual upward trend seen in recent months.

Producer input costs for the food manufacturing sector eased slightly during the last quarter of 2025, with the relevant index declining by 0.4 percent over the period. This measure captures a range of operating inputs including wages, maintenance and general plant running costs, and the small fall suggests some moderation in underlying processing expenses. However, this easing was offset by an increase in utilities costs, with the utilities price index lifting by 0.5 percent over the same time frame.

Given the energy intensive nature of beef processing operations, even a modest rise in electricity, gas and related services can quickly erode any savings from softer labour or operating inputs. The combination of a marginal fall in broader producer input costs and a rise in utilities meant that overall operating cost pressures were broadly steady to slightly higher. In the context of a 5 to 6 percent jump in livestock procurement costs, these movements in operating and utilities expenses provided little meaningful relief for processor margins through November.

The inclusion of the weak November result has pulled the 2025 year to date average BPTC down from 59 percent to 54 percent. Strong margins through the first half of 2025, supported by lower cattle prices and relatively solid export returns, had kept the annual average elevated despite mounting pressure from late winter onwards. As procurement costs lifted through August, September and again in November, monthly readings fell into low territory and eroded that earlier buffer. Even with the downward revision, a 54 percent annual average still points to a year that was reasonable in aggregate for processors, though the trend into the final months highlights a far more challenging operating environment and a much thinner margin cushion heading into 2026.

The November movements illustrate the core dynamic driving the latest decline in processor trading conditions. Livestock input costs rose sharply across all categories at a time when export and domestic selling prices were only edging higher on balance. The result was a renewed squeeze on margins and a further softening in the BPTC index for the month. The data reinforces the sensitivity of processor profitability to rapid changes in cattle markets and highlights how even modest shifts in export and retail returns can be overwhelmed when procurement costs move higher in a concentrated period.

With co product values still to be updated, the full revenue picture for November is not yet complete. Even so, the scale of the increase in livestock prices suggests that any additional support from hides, offals or tallow would be unlikely to fully offset the impact on margins. For now, the November data points to a sector that remains highly exposed to movements in cattle prices and reliant on stronger downstream demand to restore more balanced trading conditions.