Flush fades as lamb prices firm

Market Morsel

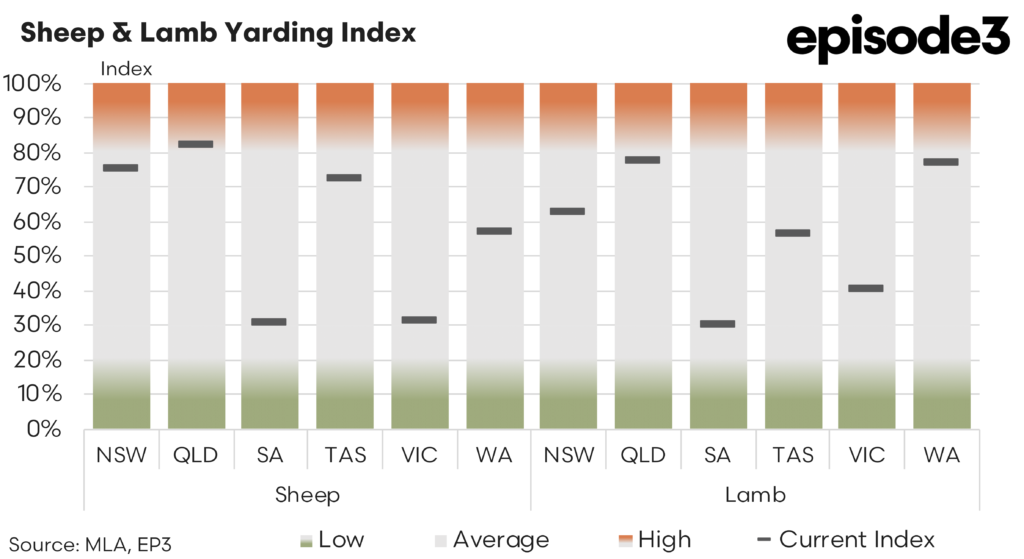

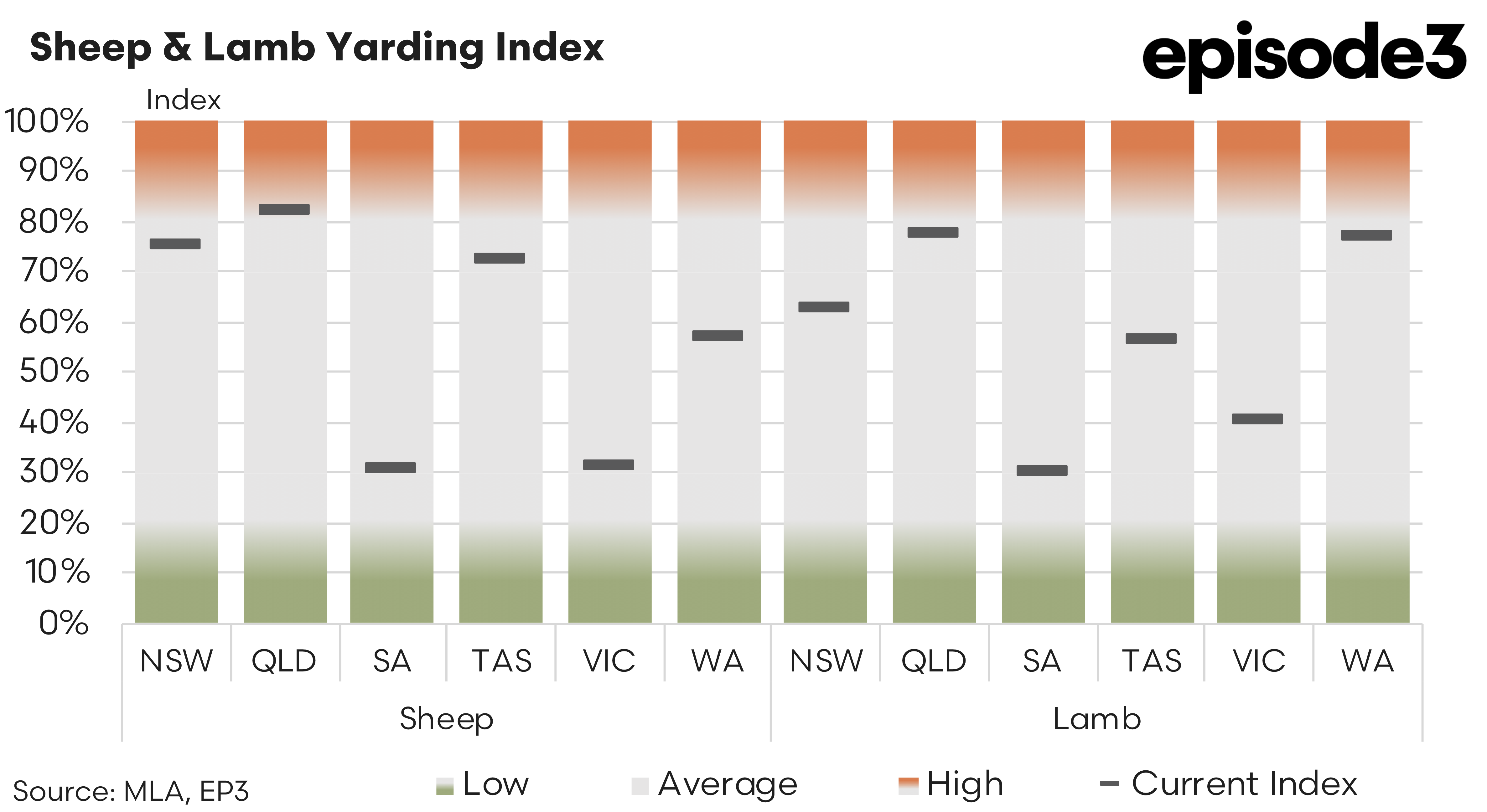

Lamb and sheep supply has continued to evolve through late summer, but the latest yarding index movements show that the flush which dominated markets earlier in the season is now easing in several regions. The changes recorded between mid-January and mid-March reveal a market that is gradually tightening in parts of the eastern states, even as some areas continue to move through the tail end of their seasonal supply.

For sheep, the yarding index movements show a mixed pattern across the country. New South Wales eased slightly from 79 percent to 76 percent, indicating that throughput remains relatively strong but has softened marginally compared with the levels seen earlier in the year. Queensland moved in the opposite direction, lifting from 72 percent to 82 percent, suggesting that sheep turnoff has picked up noticeably in the northern state over the past month.

South Australia continues to sit well below typical levels, although it has lifted modestly from 19 percent to 30 percent. While this increase is proportionally significant, it still represents historically low supply conditions for the state and highlights how tight sheep availability remains across parts of the southern producing regions. Tasmania recorded one of the more pronounced movements, rising from 47 percent to 72 percent, indicating that sheep supply has strengthened considerably there over the past several weeks.

Victoria showed a tightening change, sitting at 31 percent compared with 46 percent earlier in the period. This still places Victorian sheep yardings well below typical seasonal levels and reinforces the view that sheep supply across the major eastern states remains constrained relative to historical norms. Western Australia moved only slightly, from 55 percent to 57 percent, suggesting relatively stable supply conditions through the western market.

While sheep supply has been mixed, the lamb yarding indices tell a clearer story of tightening availability across the eastern states. New South Wales declined from 63 percent to 58 percent, reflecting a gradual easing in lamb throughput as the earlier wave of spring-born lambs begins to pass through the system. Queensland recorded a sharper decline, falling from 78 percent to 67 percent, which indicates that the earlier supply surge in the northern market has now begun to taper off.

South Australia moved in the opposite direction, although from a very low starting point. Lamb yardings lifted from 30 percent to 34 percent, suggesting some additional throughput entering the market. Even so, this remains well below the levels typically associated with a full seasonal flush and highlights the relatively tight supply conditions that have persisted in the state.

Tasmania remained unchanged at 57 percent, indicating that lamb supply there has stabilised after earlier increases. Victoria recorded a modest lift from 41 percent to 46 percent. Although this represents an increase in throughput, Victorian lamb yardings remain well below the levels typically seen during the peak of the spring run, confirming that the main seasonal flush has already passed and the market is now operating with more limited supply.

Western Australia stands out as the strongest lamb supply region at present, with the yarding index sitting at 77 percent compared with 67 percent earlier in the period. This suggests that lamb availability remains relatively strong in the west compared with conditions across the eastern states.

The shift in supply conditions over the past month aligns closely with the price movements recorded in the national indicators. Lamb prices have strengthened across most categories during the past four weeks, reflecting the tightening in yardings evident in several of the key producing states.

The trade lamb indicator has risen to around 1,168 cents per kilogram carcase weight, gaining roughly 67 cents over the past month. Restocker lambs have shown the strongest price improvement, lifting by more than 46 cents over the same period to sit above 1,174 cents per kilogram. The scale of this movement suggests that producer demand for replacement lambs has been particularly active.

Heavy lamb prices have also strengthened, rising by close to 36 cents over the past four weeks to sit just above 1,111 cents per kilogram. These values reflect a market where the tightening yardings in several states have clearly increased competition for stock among processors.

Mutton prices have also firmed over the past four weeks. The national indicator is now sitting at roughly 804 cents per kilogram carcase weight, an increase of around 37 cents compared with a month ago. This rise is consistent with the relatively constrained sheep supply evident in several of the eastern states, particularly Victoria and South Australia.