Improved finish to 2025 for beef processors

Beef Processor Trading Conditions - Dec 2025 update

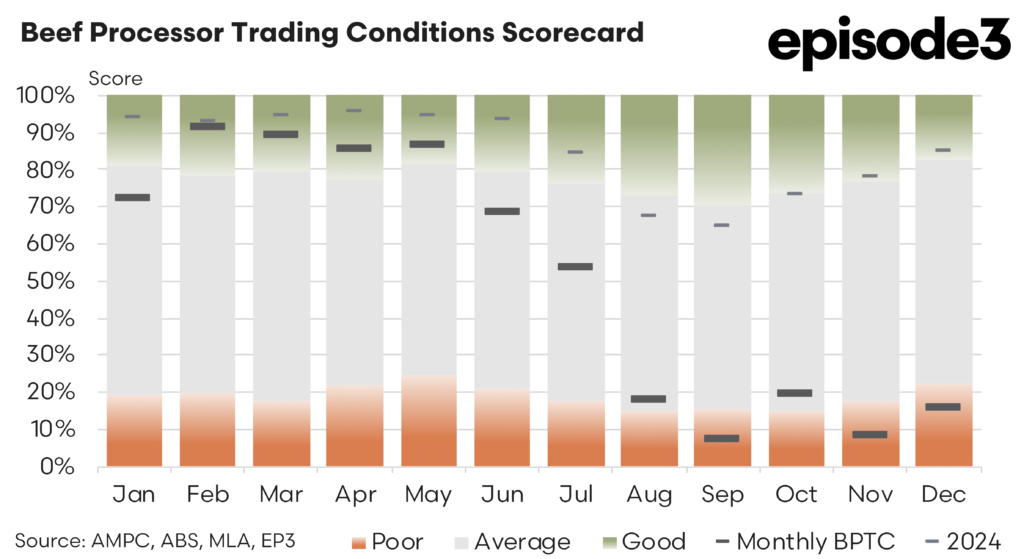

The final month of 2025 delivered a modest improvement in trading conditions for Australian beef processors, although the broader picture still reflects a far more challenging operating environment than the sector enjoyed a year earlier.

After a difficult November, when margins came under pressure from sharply rising cattle procurement costs, the December data show some easing in livestock prices and a more supportive export market backdrop. Together these movements helped lift the Beef Processor Trading Conditions (BPTC) index from 8 percent in November to 16 percent in December.

The improvement was driven primarily by the input side of the processing ledger. Livestock prices softened across the major procurement categories during December, providing processors with some relief after several months of rising cattle values. Heavy steer prices declined by 0.8 percent over the month, while young cattle prices fell by 1.2 percent. Processor cow prices recorded the largest adjustment, easing by 2.4 percent. These movements reversed part of the sharp increases seen through November and helped bring procurement costs back slightly from the elevated levels that had been compressing margins.

While the reductions were relatively modest in percentage terms, they occurred at a critical point for processors who had been facing a sustained lift in cattle prices since late winter. The easing in December therefore provided a welcome, if limited, reset in the cost structure faced by abattoirs heading into the final weeks of the year. For plants operating on tight margins, even small shifts in procurement costs can materially influence profitability when multiplied across large processing volumes.

On the revenue side of the ledger, export markets moved in a more favourable direction through December. Average export values increased across all four of Australia’s key offshore beef markets. Returns into the United States lifted by 2.9 percent, while Japan recorded a 2.1 percent increase. South Korea posted a 2.2 percent rise, and export values to China increased by 2.6 percent. When combined, the weighted average across the four largest export destinations showed a gain of around 2.5 percent for the month.

The broad based nature of these improvements is noteworthy. In previous months gains in one or two markets were often offset by weakness elsewhere, limiting the overall support to processor returns. In December, however, all four key markets moved higher simultaneously. This more uniform lift in export pricing helped strengthen the revenue side of the processing equation at the same time that livestock procurement costs were easing.

Domestic retail pricing provided little additional support during the month. Retail beef prices declined slightly by 0.2 percent, indicating that the modest improvements in export values were not mirrored in the domestic consumer market. Retail pricing trends tend to move more slowly than export values, reflecting the lagged nature of supermarket pricing cycles and the broader dynamics of household consumption. As a result, retail price movements typically play a secondary role in short term changes in processor trading conditions.

Co product values, which can provide an important supplementary revenue stream through hides, offal and tallow, have not yet been updated since September 2025. These returns often provide an additional buffer for processors when primary beef prices are under pressure. However, the December improvement in the BPTC index has already occurred before these figures are incorporated, suggesting that the easing in livestock procurement costs and stronger export pricing were the primary drivers of the monthly improvement.

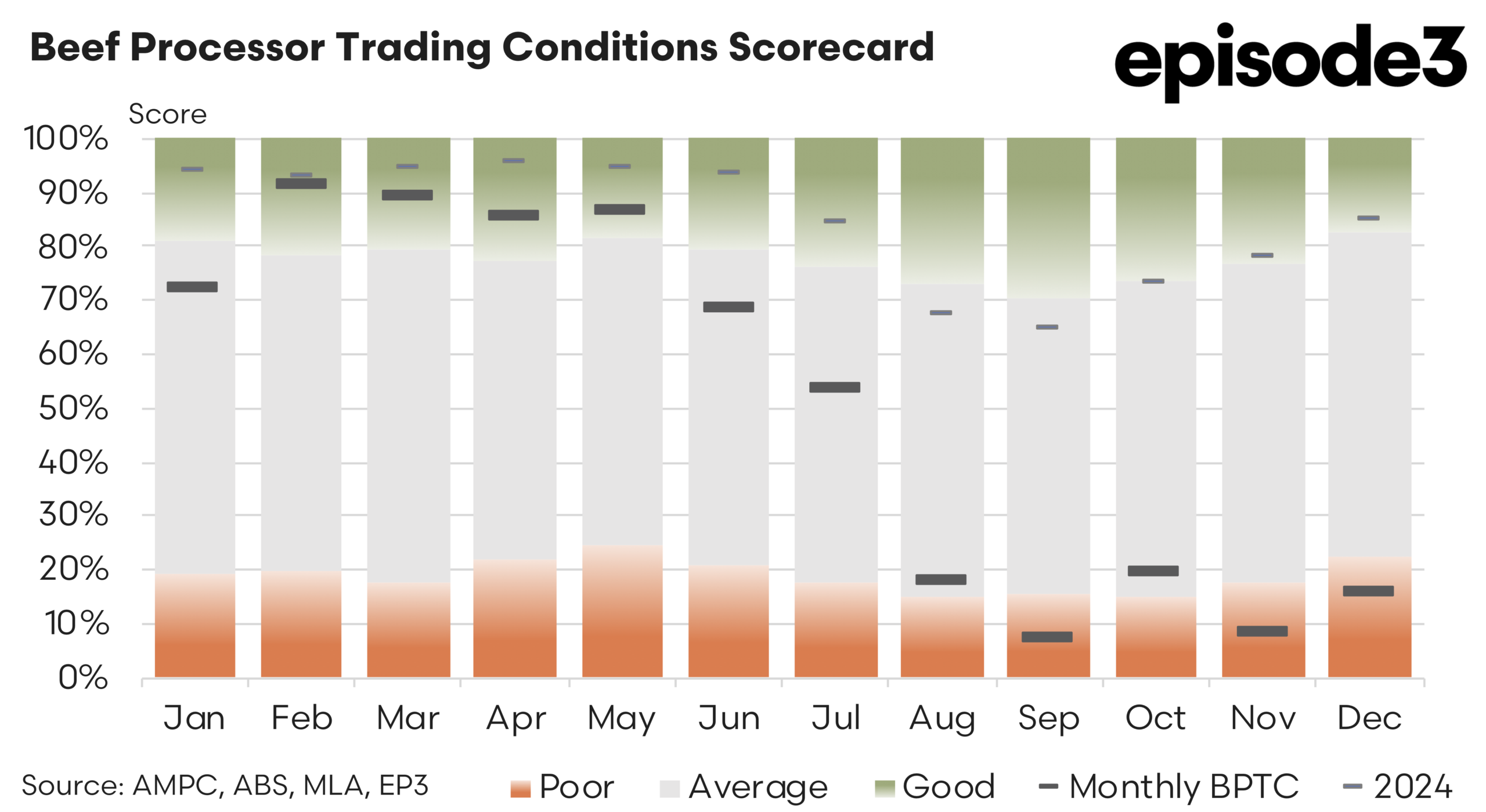

Despite the lift in December, the broader trend across the second half of 2025 remains one of tightening margins. The late year pressures were sufficient to pull the full year average BPTC reading down to 51 percent. This places 2025 firmly within what could be described as a typical or average operating year for beef processors. By comparison, the annual average BPTC result for 2024 stood at a very strong 85 percent, highlighting just how favourable trading conditions were for processors during that earlier period.

The contrast between the two years largely reflects the shift in cattle market dynamics. During much of 2024 processors benefited from relatively abundant cattle supplies and lower livestock procurement costs, while export markets remained reasonably supportive. That combination created an unusually favourable margin environment. Through 2025 the balance gradually shifted as cattle prices strengthened, tightening the cost structure faced by processors and steadily eroding the margin advantage that had existed previously.

As the industry moves into 2026, the key variables to watch remain largely unchanged. Movements in cattle prices will continue to exert the strongest influence on processor margins, while export market performance will determine how effectively those input costs can be recovered through the value chain.