Processors and Prices

Processing Throughput

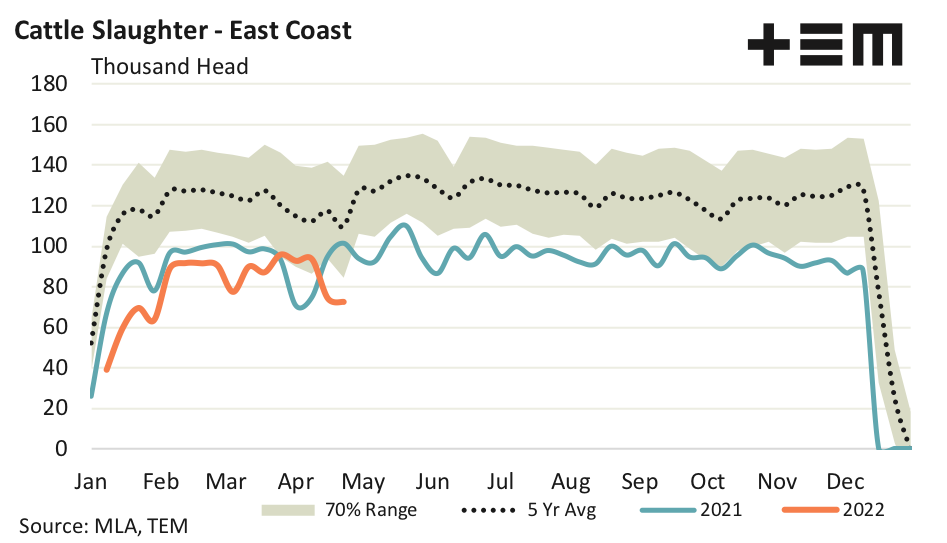

East coast weekly cattle processing levels remain relatively flat as the Easter and Anzac day holiday period keeps volumes light. There were 72,441 head of cattle processed to the week ending 22nd April which is nearly 3% higher than the low point of cattle processing throughput during Easter 2021.

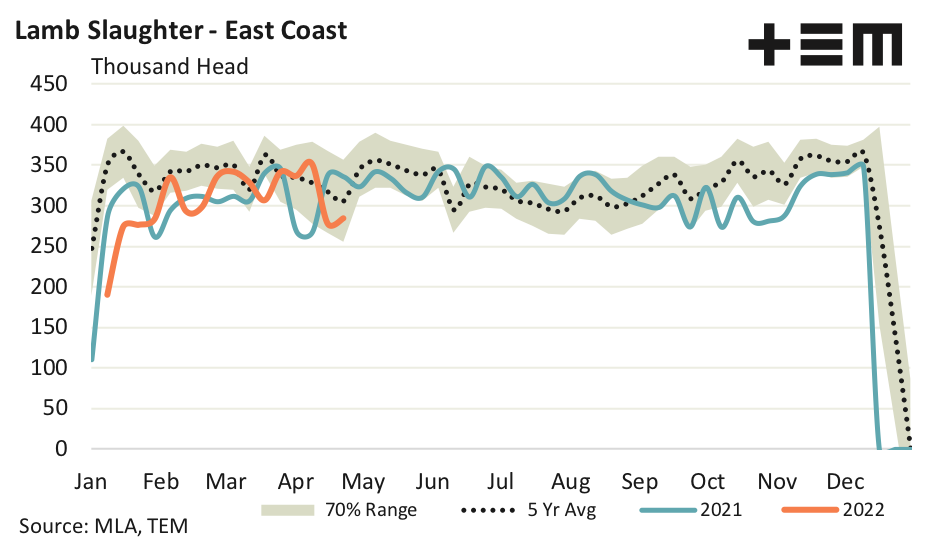

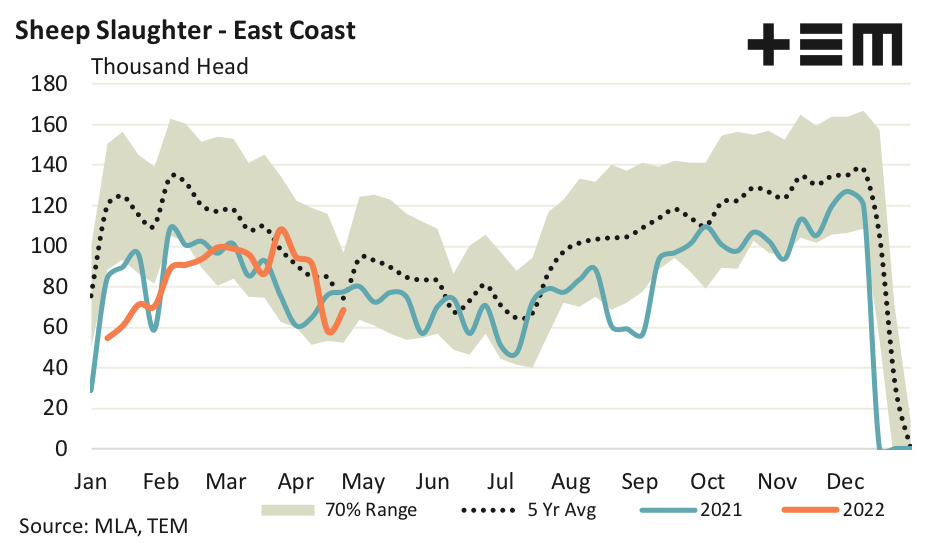

Weekly east coast lamb slaughter managed a 2% gain on the previous week to register 284,044 lambs processed. The Easter lull in 2021 saw lamb processing drop to a weekly low of 267,307 head putting this season’s throughput volumes ahead of last year by 6%. A strong gain was recorded by mutton slaughter volumes, up 18% on the week prior to manage 68,421 head processed.

Saleyard Prices

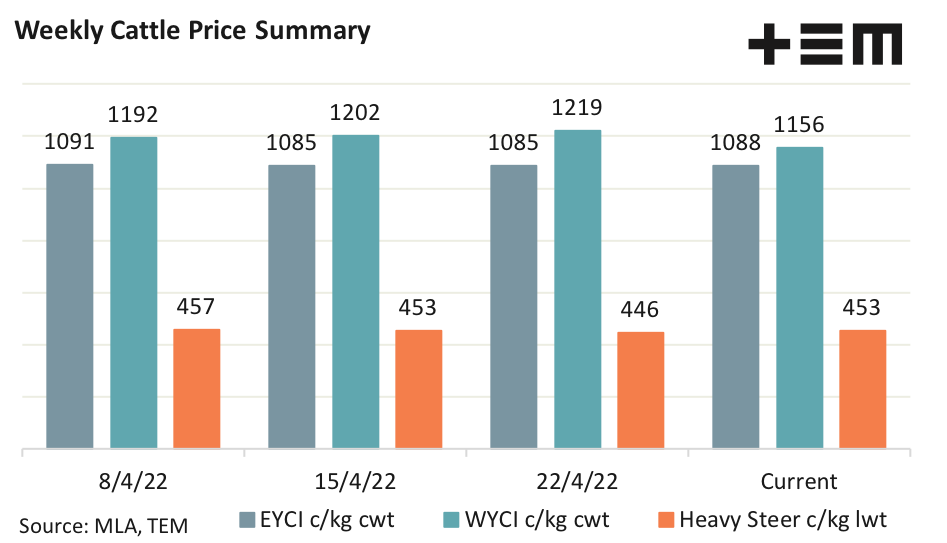

Young cattle markets across the eastern seaboard are relatively unchanged at 1088 c/kg cwt. Indeed comparing the weekly price for the Eastern Young Cattle Indicator (EYCI) across the last month shows very little change with a 3 cent fluctuation noted either side of the current price. Young cattle prices in the West have been a little more active with a 5.2% drop noted for the week (as at 28th April) to trade at 1156 c/kg cwt.

The National Heavy Steer has regained some ground, lifting 1.6% to close at 453 c/kg lwt, back to where we were a fortnight ago.

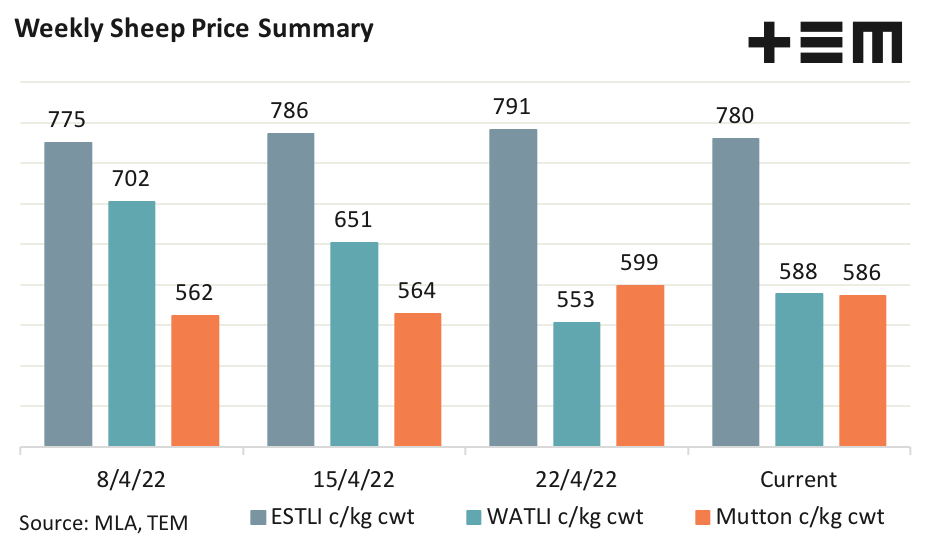

The Eastern States Trade Lamb Indicator (ESTLI) continues to soften, down 1.4% on the week to 780c/kg cwt. Although, as our recent analysis highlights it is not uncommon to see the ESTLI begin to gain ground during May so a change of trend maybe just around the corner. The WA Trade Lamb Indicator managed to bounce back from the Easter pricing lull with a 6.3% lift to 588c/kg cwt, as at 28th April. Although the National Mutton Indicator wasn’t as fortunate, sliding 2.2% to close at 586c/kg cwt.