Sheep meat processors start 2026 with a small win

Sheep Processor Trading Conditions Model

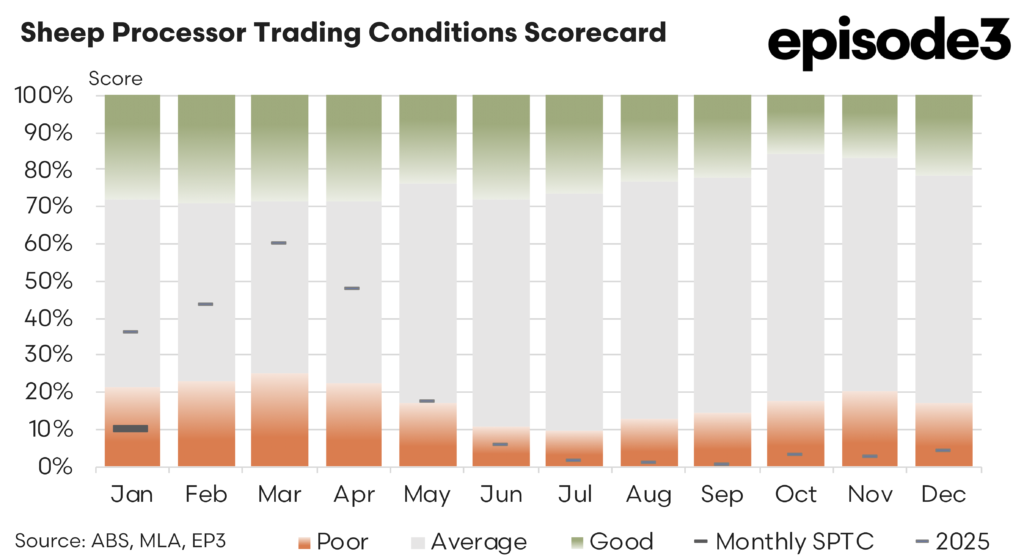

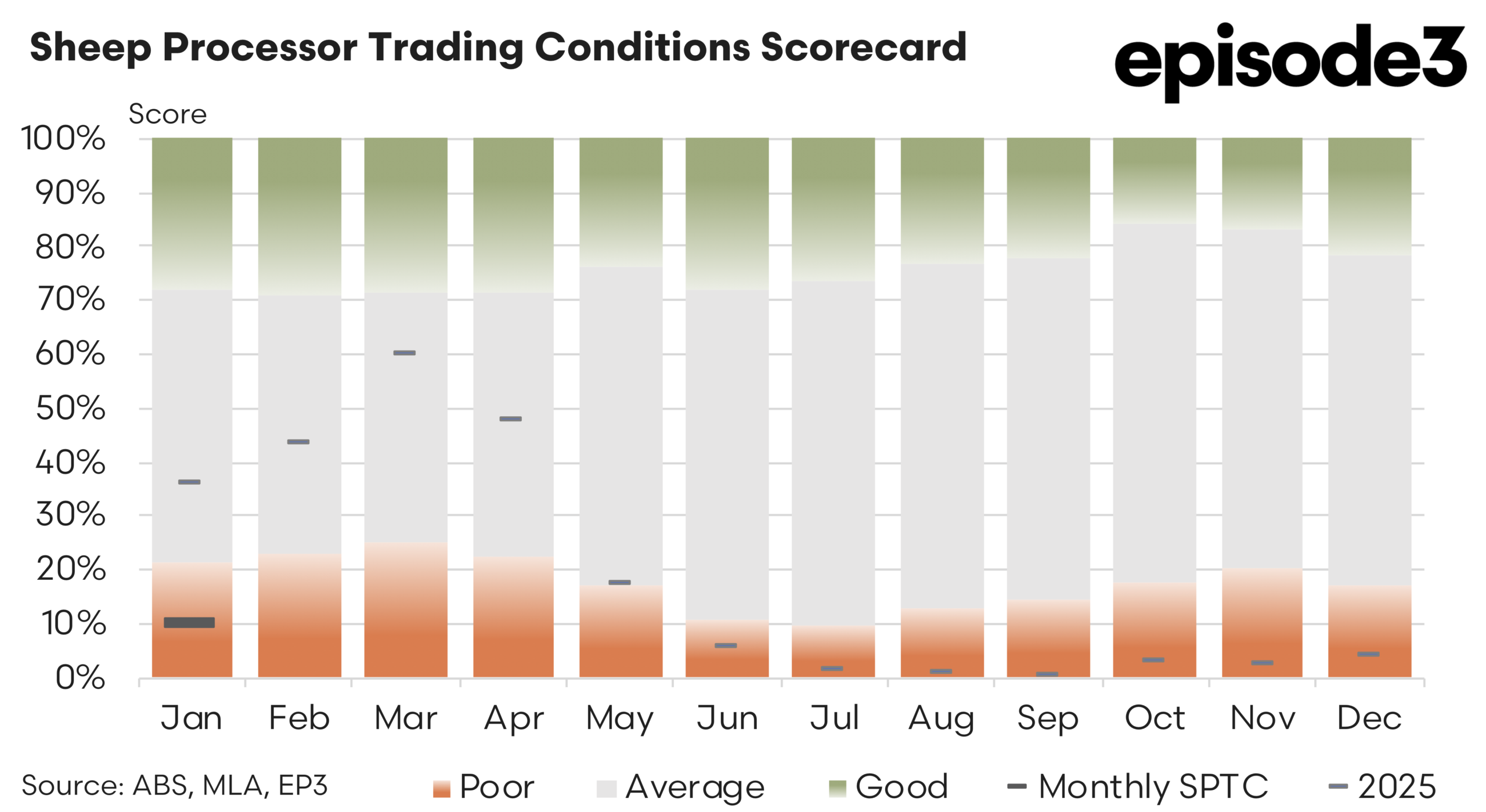

The sheepmeat processor trading conditions (SPTC) model showed a modest improvement in January, but the broader trend remains one of significantly tighter margins compared to the same period last year.

The January SPTC came in at 10 percent, lifting from a revised December figure of 4.5pc, although still well below the January 2025 level of 36pc. The downward revision to December from 8pc to 4.5pc highlights the sensitivity of the model to export value adjustments and reinforces that processor margins at the end of 2025 were weaker than initially estimated. While the lift into January suggests some improvement in operating conditions, the comparison to last year makes it clear that processors are operating in a far more constrained margin environment.

On the livestock procurement side, price movements during January were relatively mixed, offering only limited relief to processors. Heavy lamb prices eased by 2.2pc over the month, while light lambs declined by 0.5pc, providing some marginal reduction in input costs at the heavier and lighter ends of the spectrum. However, these gains were partially offset by increases in other categories, with trade lamb prices rising by 0.9pc and mutton lifting by 0.4pc. This combination of movements suggests that while there was some easing in procurement costs, it was neither broad based nor sufficient to materially shift overall margin pressure. The fact that trade lamb prices increased is particularly relevant, as this category often represents a significant portion of processor throughput and therefore has a disproportionate impact on overall input cost structures.

On the domestic side, retail lamb prices softened during January, easing by 1.7pc over the month. This decline in retail pricing limits the ability of processors to pass through costs and maintain margins, particularly in a market where consumer sensitivity to price remains elevated. The easing in retail values suggests that domestic demand may not be strong enough to support higher wholesale pricing, further constraining processor returns.

Export markets presented a similarly mixed picture, with gains in some destinations offset by weakness in others. Export values to the United States increased by 2.1pc during January, continuing to provide a degree of support given the importance of that market for Australian lamb exports. Malaysia also recorded a modest improvement of 0.5pc, contributing positively to overall export performance.

However, these gains were counterbalanced by declines in other key markets, with China falling by 3.8pc and the United Arab Emirates dropping by 4.5pc. The weakness in China is particularly significant given its role as a major destination for mutton, and the decline suggests that demand conditions there remain subdued or that competitive pressures are weighing on pricing. The fall in UAE values further reinforces the notion that export markets are not uniformly supportive, adding to the volatility in processor returns. The export values data indicates that while there are pockets of strength, the overall environment remains uneven, limiting the extent to which processors can rely on offshore markets to drive margin recovery.

An additional layer of uncertainty in the current SPTC calculations is the absence of updated co product, offal and rendered product pricing from Meat and Livestock Australia. These values have not been released since September 2025, meaning they cannot yet be incorporated into the model for recent months. Given the importance of co products and offals in contributing to total carcass value, their exclusion introduces a degree of incompleteness to the current SPTC monthly estimates. Once these data series are updated, it is likely that there will be revisions to the SPTC figures. Depending on the direction of those revisions, processor margins could be either stronger or weaker than currently indicated.

Despite the improvement from December to January, the broader narrative remains one of constrained trading conditions for sheepmeat processors. The lift to 10pc in January suggests that margins are stabilising rather than deteriorating further, but they remain well below the levels seen a year earlier. The combination of only modest easing in livestock input costs, softer domestic retail pricing and mixed export performance continues to cap margin expansion.

At the same time, the tightening in sheep supply seen in slaughter data is likely to place upward pressure on mutton prices in the months ahead, which could further challenge processor profitability. Lamb markets, while showing some signs of price easing in certain categories during January, are also beginning to firm in broader indicators, suggesting that input costs may not provide sustained relief. Overall, the January SPTC result points to a market that is stabilising but not yet recovering in any meaningful sense.