Sheepmeat export update February 2026

February 2026 - Sheep Meat Export Update

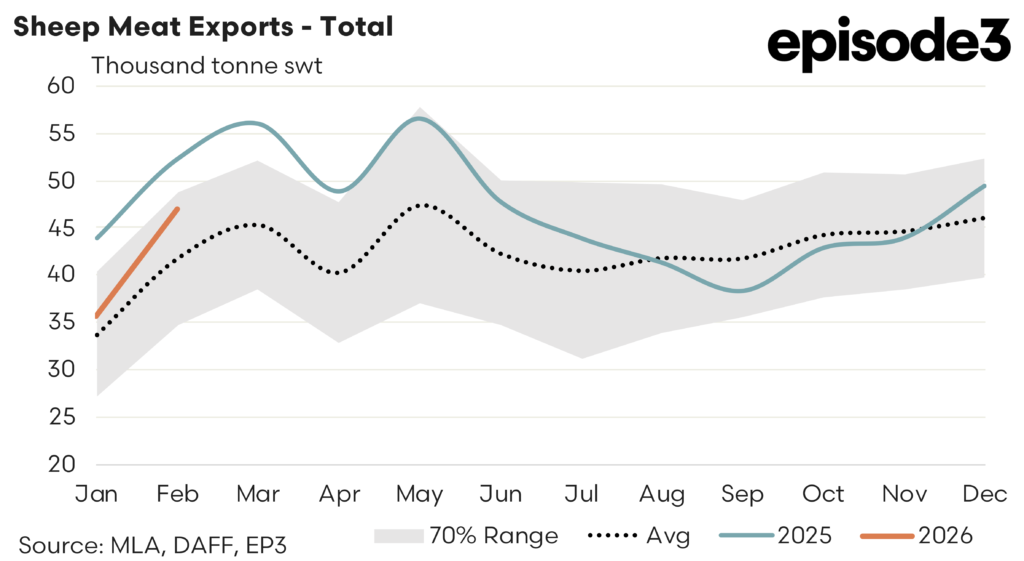

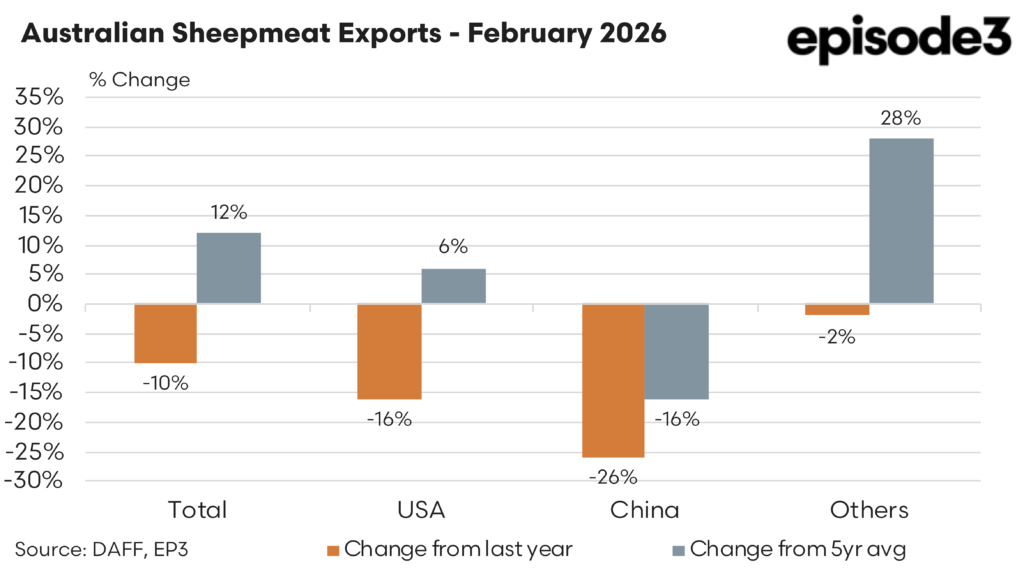

Australian sheepmeat exports softened in February, easing back from the exceptionally strong levels seen in recent years. Total shipments reached 46,890 tonnes for the month which placed exports 10 percent lower than February last year. Despite the year on year decline the result still sat 12 percent above the five year February average, highlighting that export volumes remain historically solid even as the market adjusts from the unusually high throughput seen through 2024 and 2025.

The softer result reflects a combination of factors including slightly tighter livestock supply in some regions and a period of adjustment in global demand after record price levels last year. While exports have eased from the record pace of recent seasons the broader trend still points to strong underlying demand for Australian lamb and mutton across a diverse set of global markets.

China remained the largest individual destination during February with 9,325 tonnes of Australian sheepmeat shipped into the market. Despite retaining its position as the leading market, shipments to China were 26 percent lower than February last year and also 16 percent below the five year February average. That result highlights the continued volatility within Chinese import demand. Over the past decade China has been one of the most important growth markets for Australian sheepmeat, particularly for mutton product. However monthly trade flows can vary significantly depending on domestic inventory levels and the timing of purchases by importers.

The United States was the second largest destination during February with 8,079 tonnes exported. Shipments to the US were 16 percent lower than the same month last year, reflecting a modest pullback from the very strong buying seen through much of 2025. Despite the year on year decline, exports into the US were still 6 percent above the five year February average, suggesting demand remains broadly firm even if the pace of buying has moderated slightly.

Outside of the two largest markets the remainder of Australia’s export program continues to be spread across a wide range of destinations. Combined shipments into other markets reached 29,486 tonnes during February. That segment of the trade was 2 percent lower than the same month last year but sat 28 percent above the five year February average. The strength relative to historical averages highlights the increasing diversification of Australia’s sheepmeat export base, with product flowing into markets across Asia, the Middle East, North America and a range of smaller destinations.

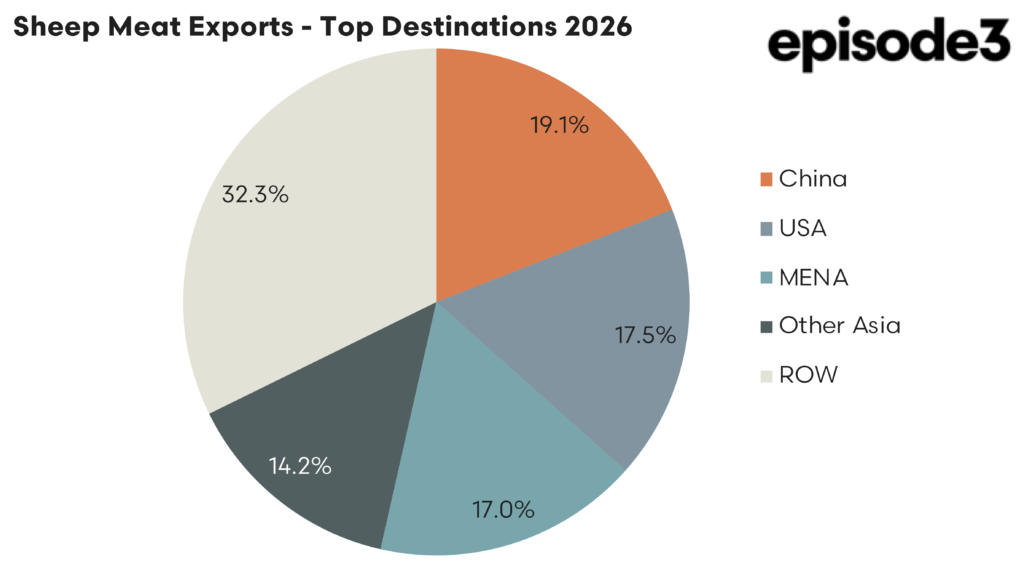

Looking at the broader composition of the export market provides additional context. China accounted for around 19 percent of Australia’s sheepmeat exports, while the United States represented roughly 18 percent of total shipments. The Middle East and North Africa region continues to play a major role as well, absorbing around 17 percent of exports, while other Asian markets collectively account for roughly 14 percent. The remaining third of the trade is spread across a variety of smaller markets.

That diversified export structure has become increasingly important for the industry. While China and the United States remain the two largest individual buyers, a significant share of Australian sheepmeat now moves into a wide range of secondary markets. This breadth of demand provides a degree of resilience when conditions soften in any single destination.

Even with the decline from last year’s levels the February figures still represent a relatively strong result when viewed against longer term seasonal patterns. Export volumes remain above the five year average and global demand for Australian sheepmeat continues to be supported by strong consumption across multiple regions.

Looking ahead the key drivers for the remainder of 2026 will likely include the pace of Chinese demand, conditions in the US foodservice sector in response to the 15% tariff applied recently and developments across the Middle East where ongoing geopolitical tensions due to the Iran war could influence shipping/airfreight access. For now however the February data suggests the market is settling into a more balanced position after the unusually strong export performance of recent years while still maintaining historically solid trade volumes.