What’s in store for 2024?

Market Morsel

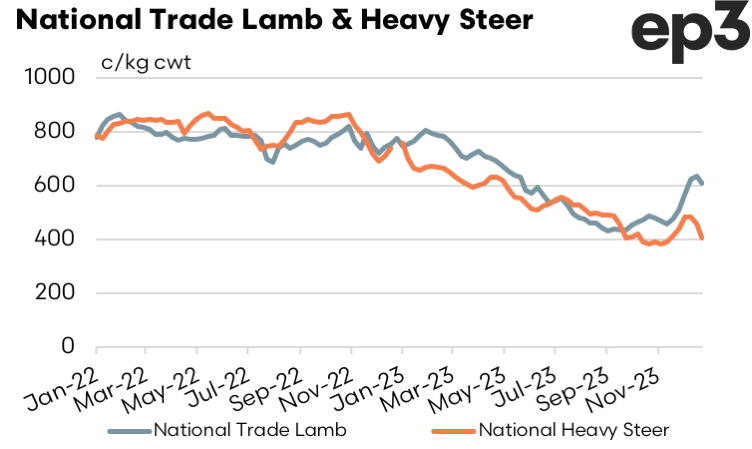

As we begin 2024, the Australian sheep and cattle producers are treading a path markedly different from the stellar heights of the previous years. After witnessing livestock prices halving from the record levels reached in 2022 and the earlier months of 2023, this year brings with it a set of variables that promise to shape the trajectory of livestock markets.

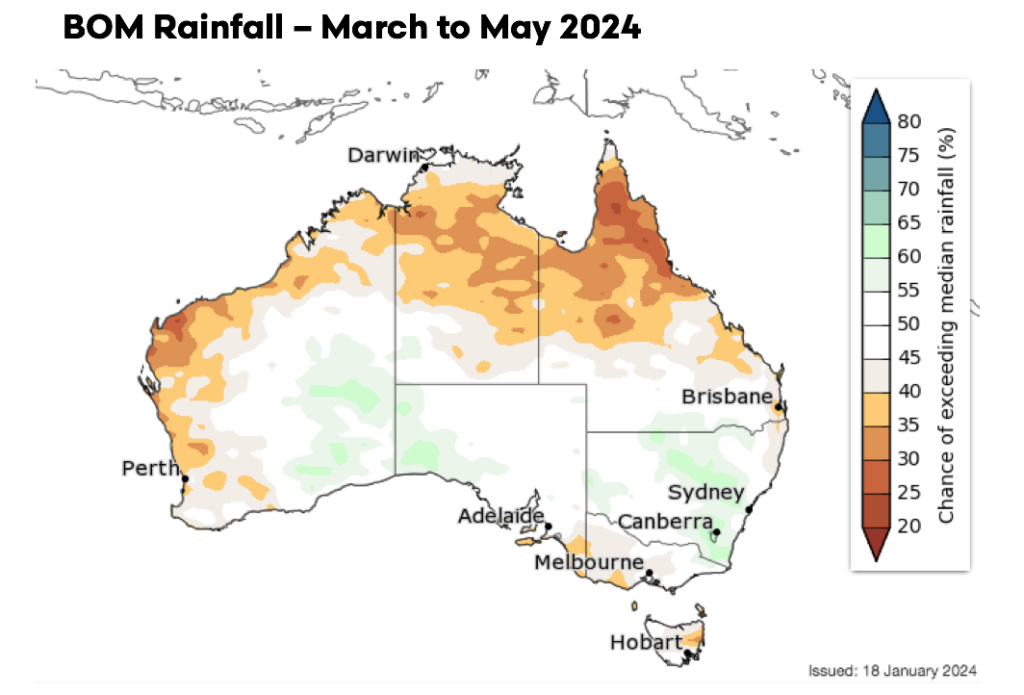

The start of the year has been greeted by a meteorological shift with the breakdown of El Nino, leading to a wetter commencement to 2024 than anticipated by the Bureau of Meteorology (BOM). While a weakening El Nino during the summer months isn’t a rarity, the critical aspect for this year hinges on whether El Nino will make a resurgence or dissipate. A revival of El Nino could spell the onset of arid conditions, propelling the Australian herd and flock towards an intensified liquidation phase. Conversely, a reversion to regular rainfall patterns could provide further support to producer confidence and underpin livestock prices as we edge toward the mid-year.

A key indicator that demands attention is the BOM’s three-month rainfall outlook as autumn approaches. The re-emergence of El Nino and a resulting dry spell could reintroduce price pressures within livestock markets. On the flip side, a sustained pattern of normal rainfall would likely nurture the emerging recovery in livestock prices, a trend that commenced towards the end of the previous year for both sheep and cattle markets.

The narrative of meat processor capacity adds another layer to this complex environment. The previous year’s price pressures were, in part, a by-product of bottlenecks faced by red meat processors, stemming from labour capacity and workforce accommodation constraints. Although there has been a recent improvement in abattoir capacity, the industry has not yet encountered drought-level turnoff volumes that would serve as a litmus test for the processing sector. A looming concern is the potential return of drier conditions and escalated herd and flock liquidation, which could exert undue pressure on the processing sector, leading to disruptions akin to those wrought by workforce limitations seen during 2023 and resulting in unfavourable price pressures for livestock producers.

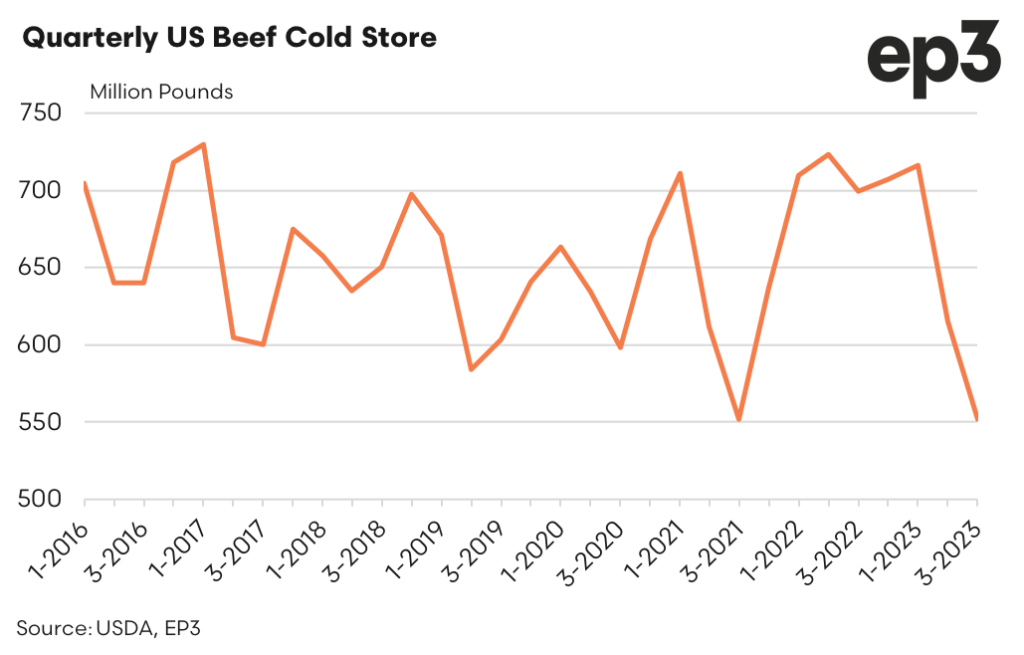

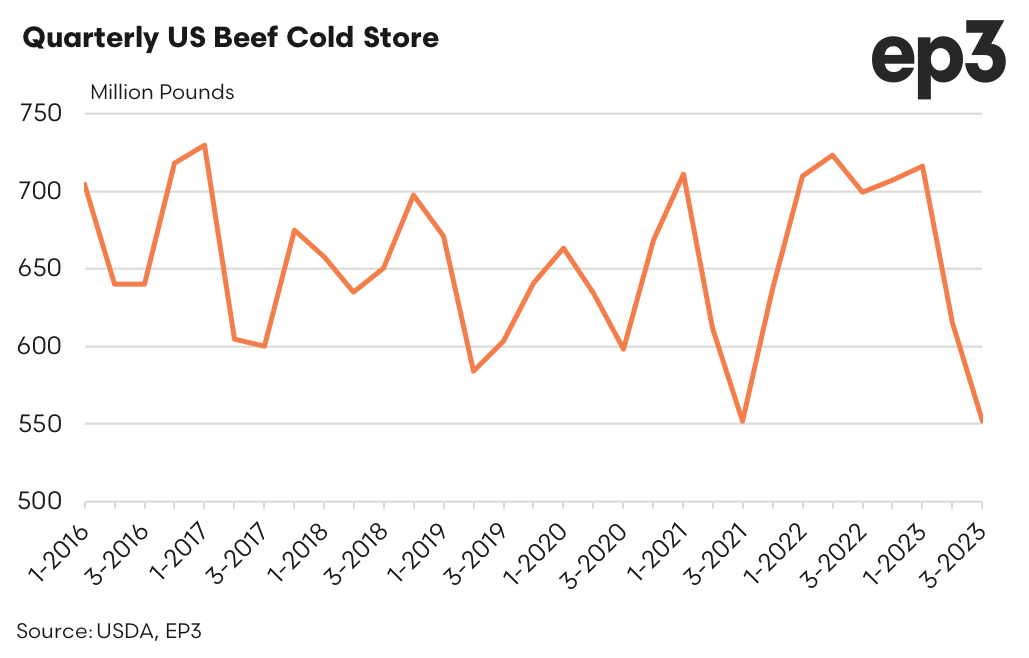

Furthermore, the United States’ herd status and beef production cast a long shadow over global meat markets. The US is entrenched in its fourth consecutive year of herd liquidation, and by the latter months of 2023, it had begun to draw down its beef cold stores and curtail beef production. This tightening supply has propelled US cattle prices to record high levels, encouraging increased beef and sheepmeat imports from nations such as Australia.

Should the US embark on a herd rebuild in 2024, it would further strain their domestic red meat provision, enhancing opportunities for Australian beef and sheepmeat producers to expand their market share in the US and to compete more effectively against US beef in important beef export markets like Japan, South Korea, and China.

The commercial rapport between Australia and its largest trading partner, China, has also undergone a notable evolution. The latter stages of 2023 were characterised by a discernible warming in diplomatic and trade relations, culminating in the reinstatement of access to the Chinese market for select Australian red meat export abattoirs. As we progress into 2024, the prospects for a continued enhancement of this trade relationship appears promising.

However, casting a shadow of uncertainty is the state of the Chinese economy. Grappling with an economic growth rate that languishes below their usual dynamism, China is actively implementing measures to invigorate its economy and stave off recessionary pressures. The success of these measures is pivotal; should China stabilise its economic ship, we can expect a bolstering of consumer confidence, which in turn should sustain a robust demand for agricultural imports from Australia.

The Australian livestock sector is navigating through a period of recalibration after riding the wave of record highs. The shifting patterns of climate, global market dynamics, and international trade relationships will be instrumental in charting the course for the livestock markets. Vigilance and adaptability will be the watchwords for producers as they steer through these fluctuations, with the hope that 2024 will unfold into a year of recovery and prosperity for the Australian livestock industry.