Where are we at in the livestock cycle?

Market Morsel

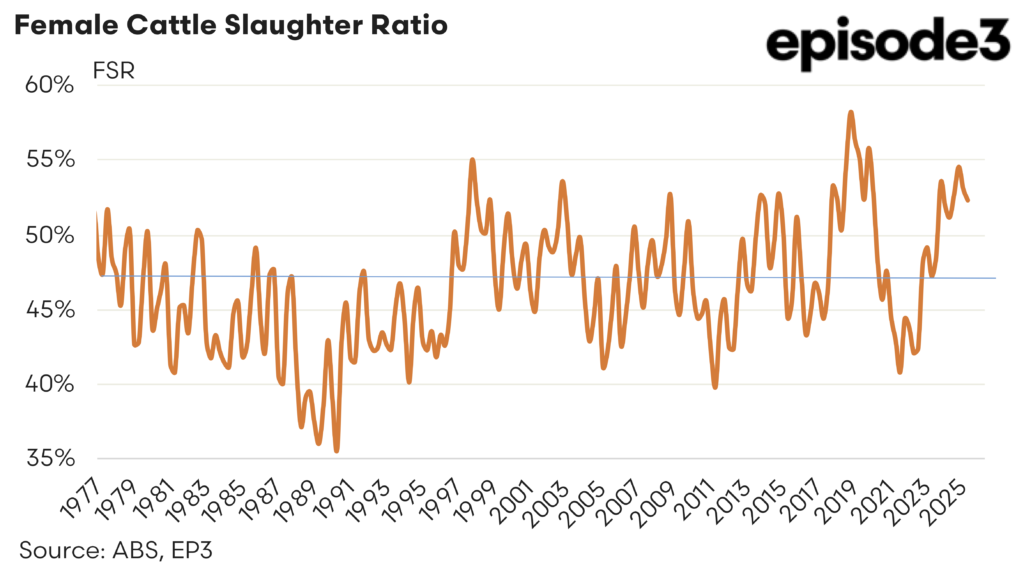

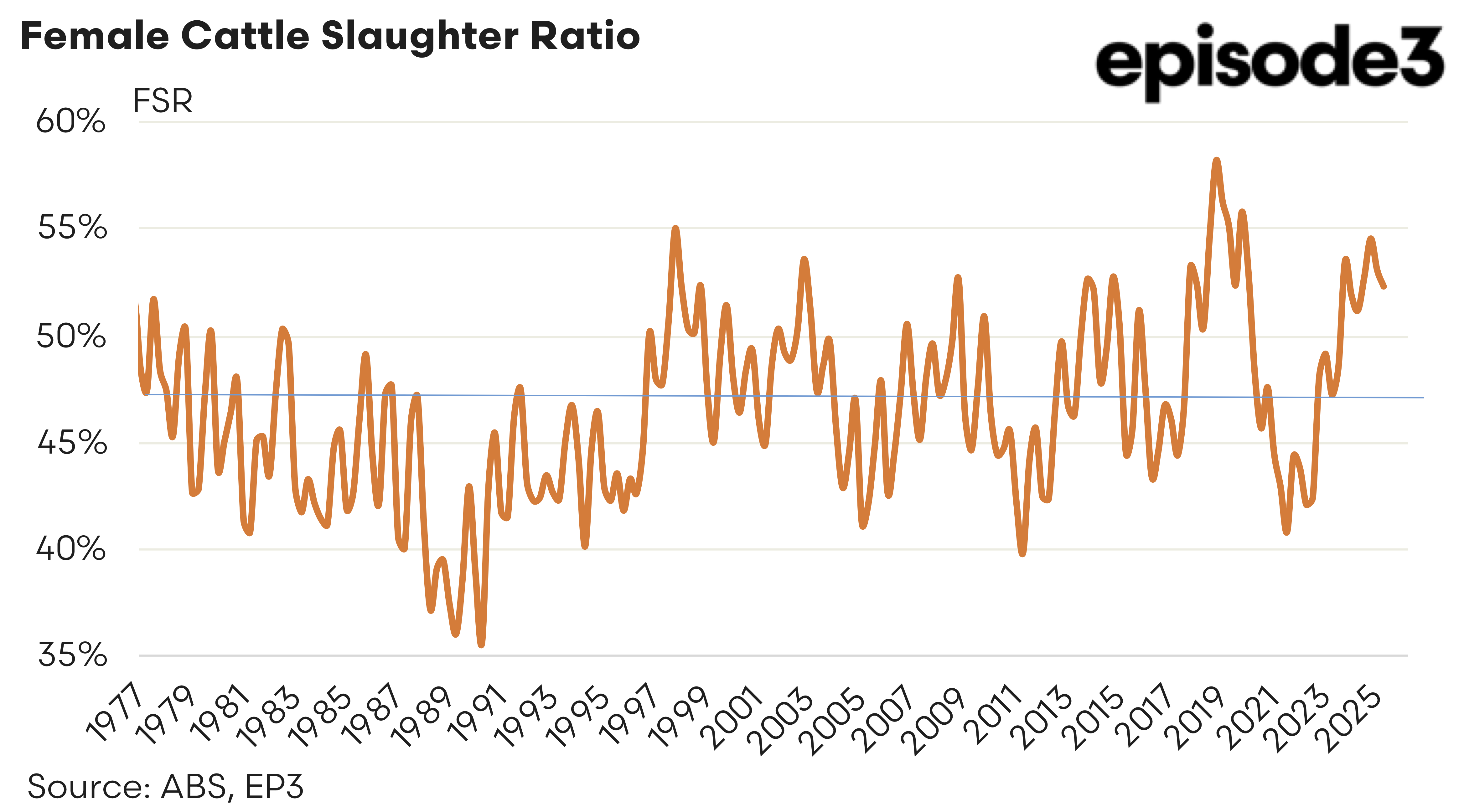

The cattle sector remains technically in liquidation, but the trend is shifting. The Female Slaughter Ratio averaged 53.1 percent across the 2025 season, with the final quarter recording 52.3 percent, as shown in the female slaughter ratio chart. Historically, the rebuild threshold sits near 47 percent. When the ratio remains above that level, it indicates producers are still sending a relatively high proportion of breeding females to slaughter, preventing herd expansion. On that measure alone, the national herd has not yet entered a rebuilding phase.

However, focusing solely on the threshold risks missing the more important signal emerging in the data. The quarterly easing in the FSR from 53% in Q3 to 52.3% in Q4, 2025 points to a gradual change in producer behaviour. Earlier in the cycle, elevated slaughter reflected forced destocking driven by seasonal pressure, high operating costs and weak confidence. The recent moderation suggests those liquidation drivers are fading. Producers are beginning to slow female turnoff, which historically occurs before herd numbers stabilise.

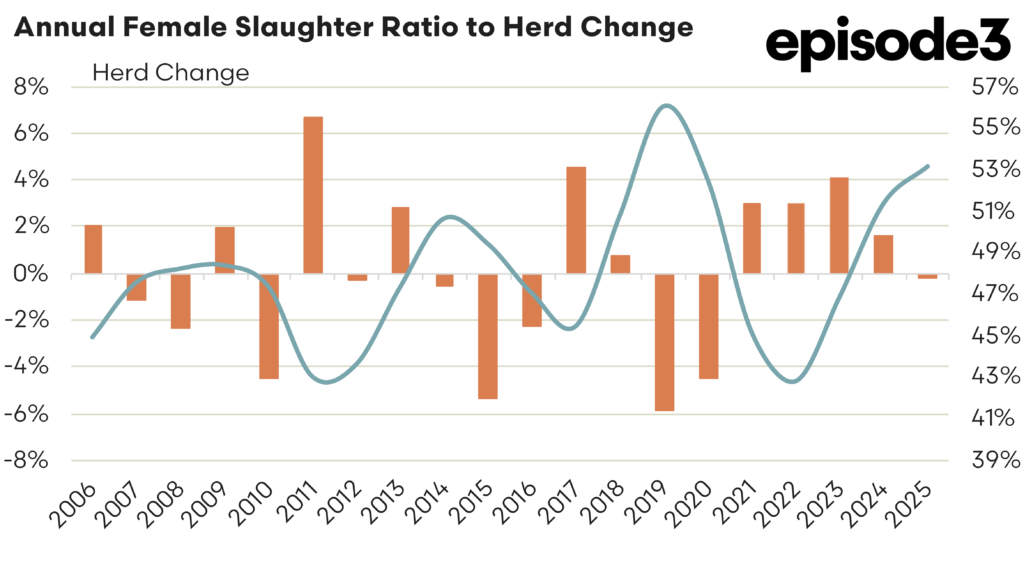

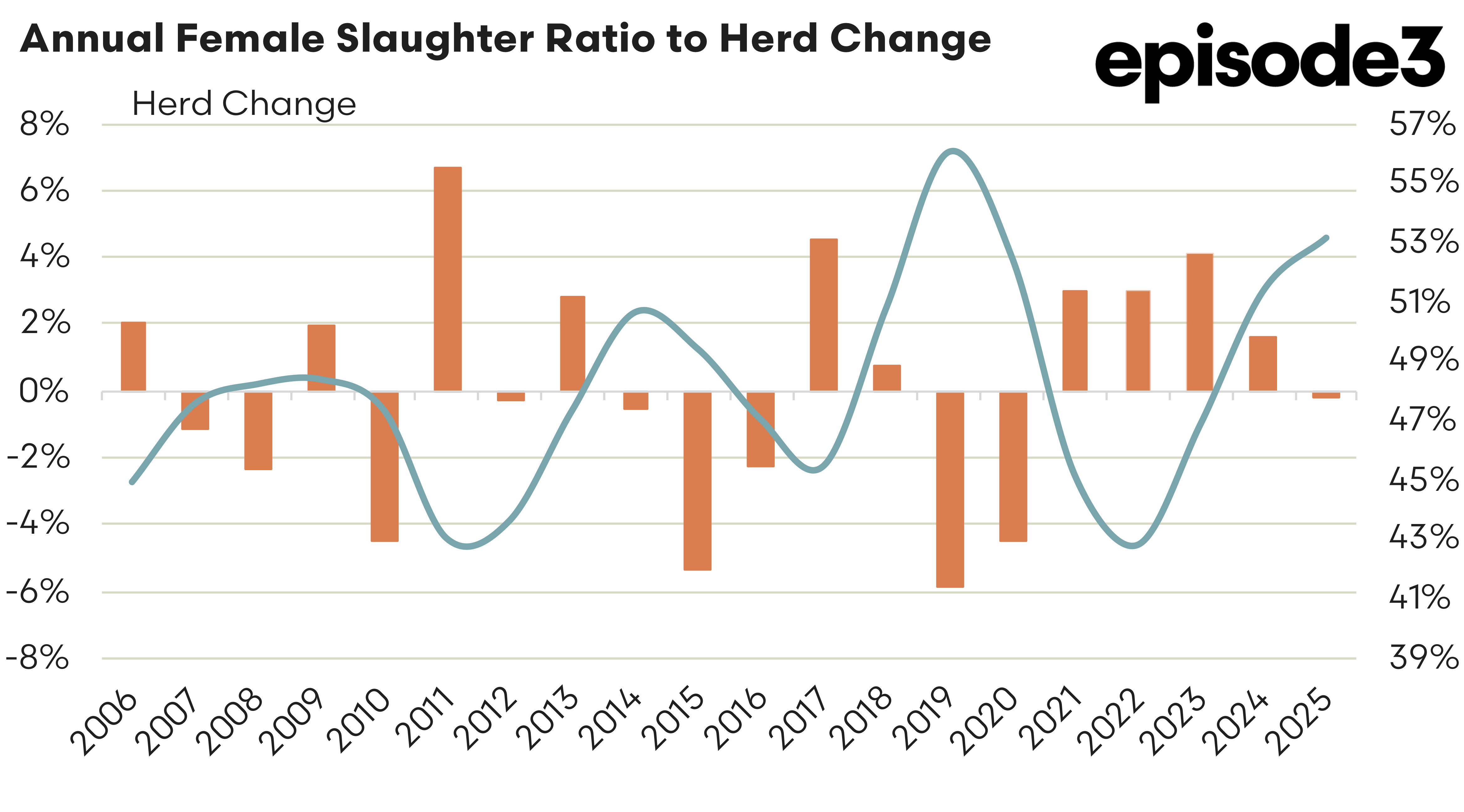

The longer term relationship between female slaughter and herd change, illustrated in the annual FSR versus herd change chart, helps explain why this matters. Periods of falling FSR typically precede improvements in herd growth rather than coincide with them. In other words, the data is signalling direction rather than confirming outcome. The herd is not rebuilding yet, but the conditions required for rebuilding are starting to form.

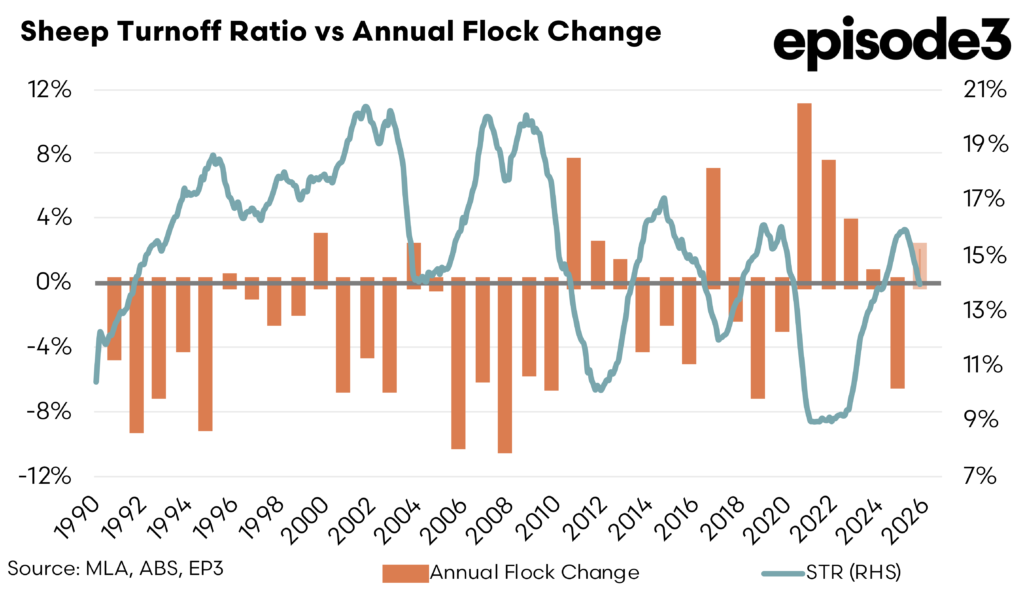

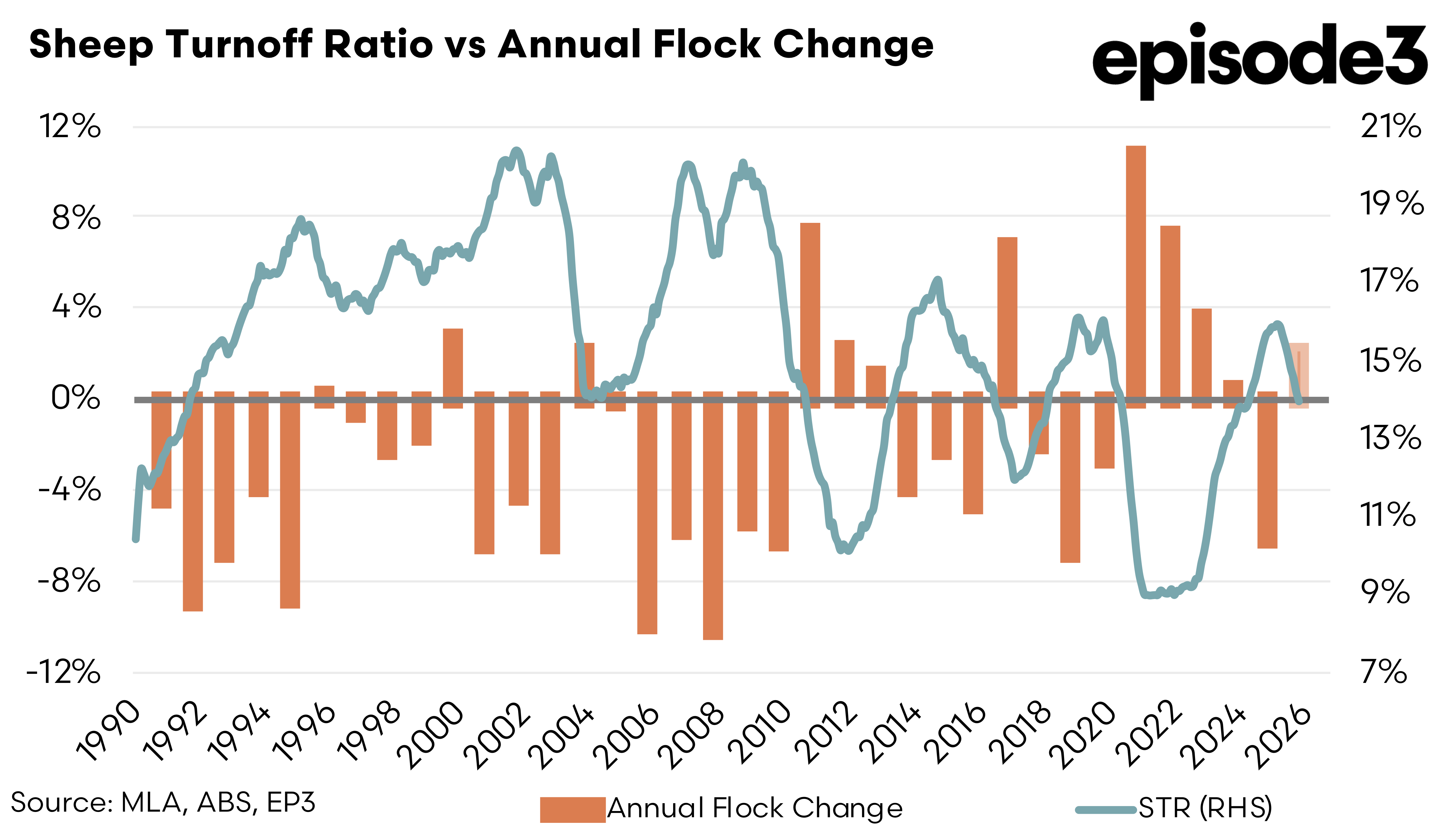

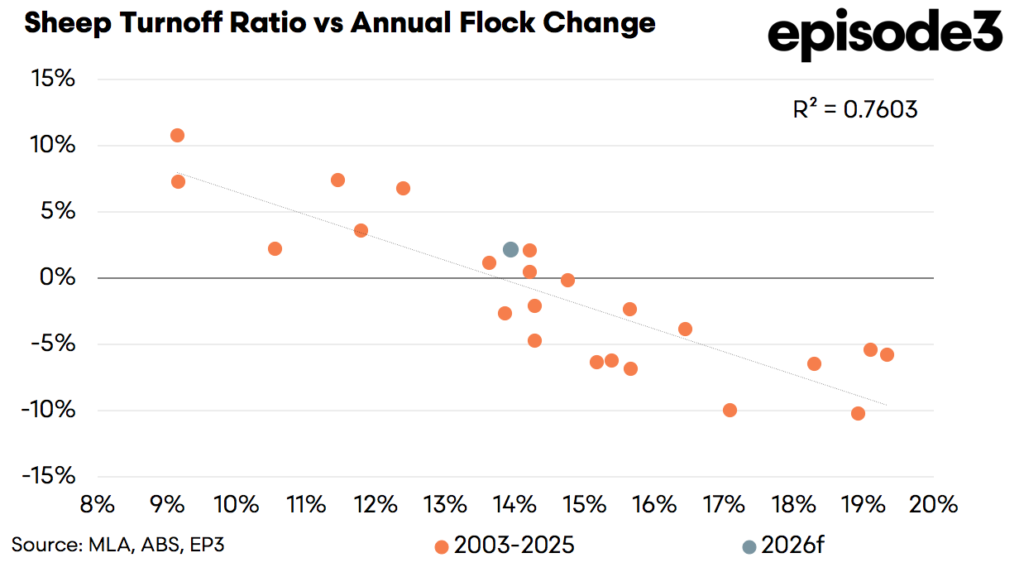

The sheep sector appears slightly further advanced along the cycle. The Sheep Turnoff Ratio declined to 13.9 percent heading into the end of 2025 and start of 2026. As shown in the turnoff ratio charts, lower STR levels are strongly associated with stabilisation or growth in the national flock. The historical relationship between STR and annual flock change demonstrates that once turnoff falls toward this range, flock contraction typically slows and eventually reverses.

This decline in turnoff suggests producers are retaining more breeding stock after several years of heavy selling. The earlier liquidation phase was characterised by elevated slaughter as producers reduced exposure amid dry conditions and difficult market settings. The recent fall in STR indicates that phase has largely run its course. While not yet indicative of rapid expansion, it does point to the beginning of a tentative rebuild.

The cattle and sheep indicators describe an industry moving through the same cycle at slightly different speeds. Sheep producers appear to have reached the turning point first, with behaviour now consistent with early rebuilding. Cattle producers, by contrast, remain in late stage liquidation, though the downward trend in the FSR suggests the shift toward retention is underway.

This staggered transition is not unusual. Biological lags, enterprise flexibility and differing market conditions often mean sheep respond more quickly than cattle. Sheep enterprises can adjust numbers faster, while cattle rebuilding requires a longer period of retained females before herd growth becomes visible in national statistics.

For markets, the implications are significant. Slaughter volumes may remain relatively elevated in the short term as animals already in the production pipeline continue to flow through processors. Yet the underlying breeding base is beginning to tighten. Historically, once both FSR and STR move lower simultaneously, future livestock availability becomes constrained, laying the foundation for firmer prices and improved producer margins.

The latest data therefore supports the view that the Australian livestock sector is on the turn rather than already in recovery. Sheep are showing early signs of rebuilding, cattle are approaching the same point, and the broader cycle appears to be shifting from contraction toward stabilisation. Whether this develops into a sustained rebuild will depend largely on seasonal conditions and producer confidence through the coming year, but the statistical signals now suggest the worst of the liquidation phase has likely passed.