Middle East War Threatens Australia’s Fertiliser Supply

The Snapshot

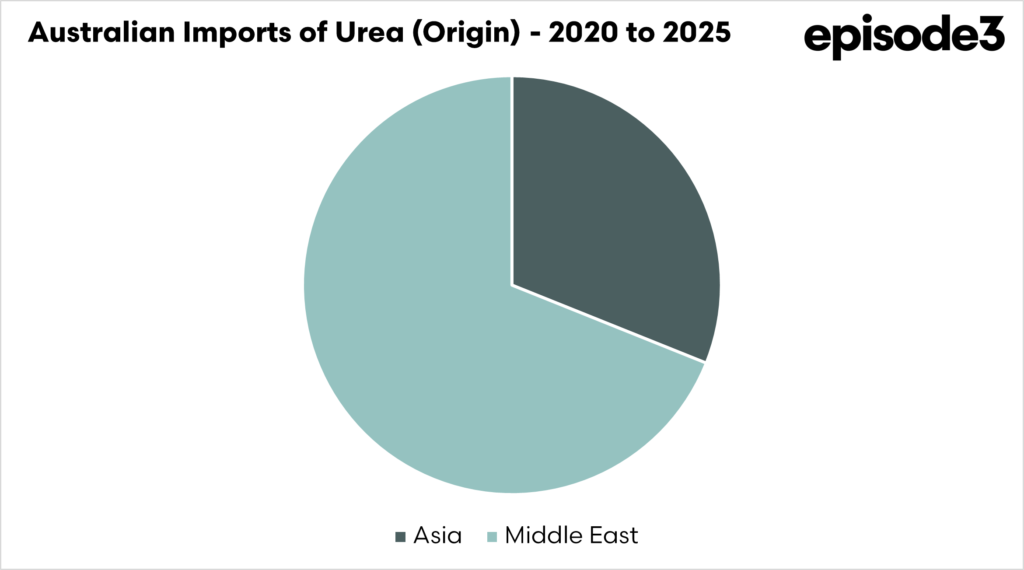

- Australia relies heavily on the Middle East for urea, with about 69% of imports coming from the region, leaving supply exposed to disruption.

- Shipping through the Strait of Hormuz has effectively stopped, cutting off the main route for Gulf fertiliser exports.

- Major production disruptions have occurred, including middle eastern plants in other countries, and wider afield in Bangladesh and Europe seeing potential production cuts due to the high price of energy.

- Even if production resumes and shipping restarts, supply will take time to recover, as plants restart operations and vessels cautiously return to the region.

- Australian urea prices are exceeding A$1200, but with many distributors providing a price, with no guarantee of access.

Get short video updates on your phone.

For quicker updates as markets move, follow @thewheatwatcher on Instagram. I regularly post short summaries and charts breaking down what’s happening in grain, fertiliser and broader ag markets so you can stay across the key moves without having to read through pages of analysis. If markets are moving quickly, that’s usually where the updates will land first.

There is a huge amount of uncertainty at the moment in relation to the US-Israel attack on Iran, but we are in for a world of pain. This conflict seems to have no endpoint, and we are already seeing significant impacts on the cost of agricultural inputs. We thought it would be worthwhile to put out some analysis on the situation, and please be aware that this situation will evolve quickly.

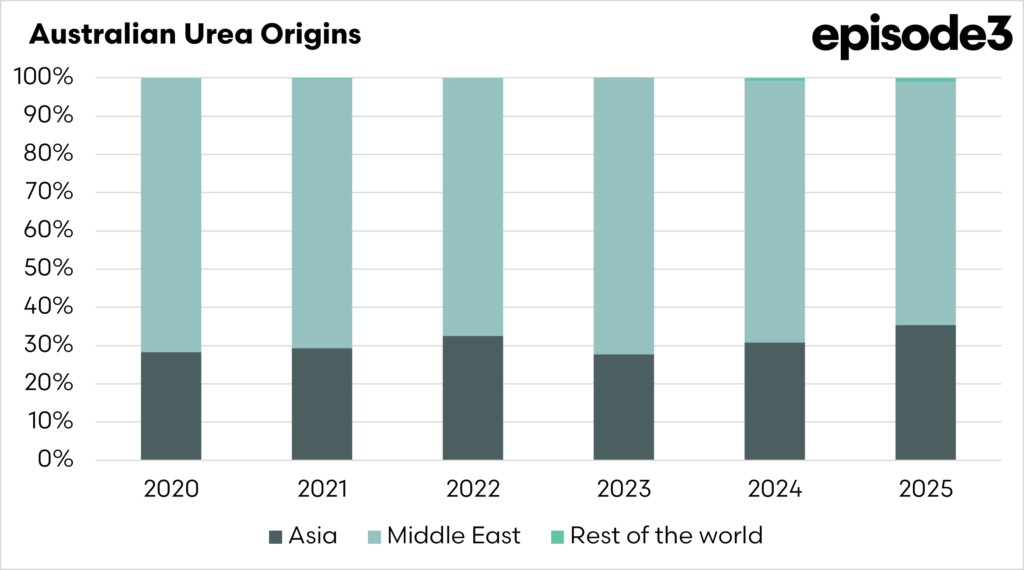

Where does our urea come from

Australia’s fertiliser supply chain has long been built on the assumption that global nitrogen markets will remain open and accessible. The data show that we are heavily reliant on the Middle East for our urea supplies, and with the conflict in the Middle East seemingly without an end in sight, we are in for a world of pain.

Over the past six years, the overwhelming majority of Australia’s imported urea has come from two regions: the Middle East and Asia. The Middle East, in particular, dominates supply, accounting for 69% of our urea. The major suppliers to Australia are Qatar, Saudi Arabia, the United Arab Emirates, Oman, and Bahrain

Asian suppliers form the second pillar of the market, though their role is more variable. Indonesia and Malaysia have been consistent exporters, while Brunei has rapidly increased shipments in recent years. China has historically been a supplier, but its exports fluctuate significantly in response to domestic policy and food security priorities. We do not expect China to come to the rescue by opening up exports in the coming months. When China restricts fertiliser exports, as it has done at times in recent years, global availability tightens quickly.

This concentration matters because many Middle Eastern suppliers are located within or near one of the world’s most strategically sensitive shipping corridors: the Strait of Hormuz. This corridor is effectively closed.

We may be able to adjust and increase our purchasing from Asia. However, with the Middle East effectively out of action, other nations will compete for this scarce supply from Asia (and other sources). As I have always said, you can always get access to whatever you want, provided you are willing to pay for it, but we don’t have unlimited resources.

In Australia, the Perdaman Urea Project, which will apparently start operations in the coming years and produce over 2 million tonnes of urea, would help address supply concerns. Whilst this urea would be priced on global values, the reality is that if, in the future, we had a supply issue of a similar extent, the government could, under emergency powers, ensure that the facility was required to keep supplies within the country, which would reduce our risk of shipping disruptions.

How much do we have in the country?

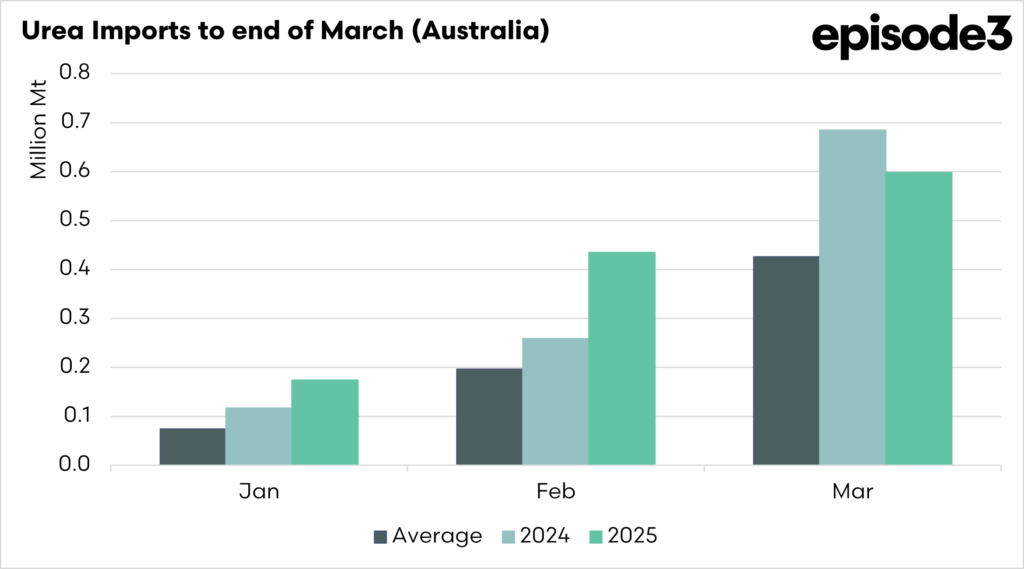

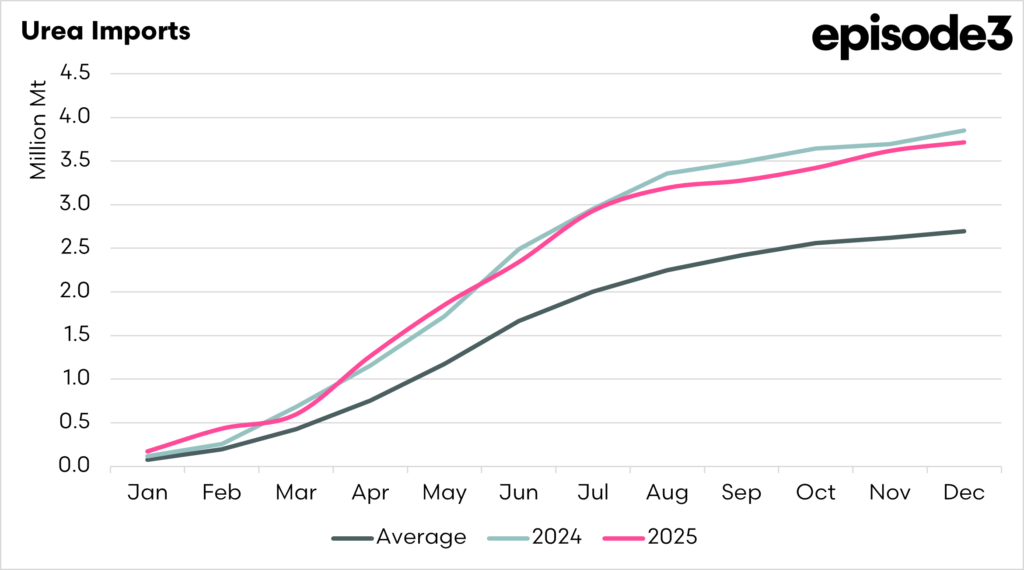

Australia’s urea import program follows a very distinct seasonal pattern, with shipments ramping up sharply through the first half of the year ahead of winter cropping demand. On average, total annual imports amount to around 2.7 million tonnes, but only a relatively small portion of that supply typically arrives in the opening months of the year.

Based on the recent historical average, cumulative imports reach around 74,000 tonnes by the end of January, representing only 2.8 per cent of the annual total. By the end of February, this rises to roughly 196,000 tonnes, or about 7 per cent of annual imports. The first meaningful build in supply occurs in March, when cumulative volumes reach approximately 426,000 tonnes. Even at that point, however, only about 16 per cent of Australia’s typical annual urea imports have arrived in the country. This is based on the five-year average.

We expect that supplies from last year, along with current volumes imported so far in 2026 and on the way, will allow us to cover around 20-25% of our requirements. This may be optimistic.

The key, though, is the volumes imported after March. By the end of April, cumulative imports climb to around 752,000 tonnes, equivalent to roughly 28 per cent of the annual supply. The pace then increases rapidly as winter crop planting approaches. By the end of May, imports typically exceed 1.17 million tonnes, meaning around 44 per cent of the year’s fertiliser requirement has been delivered. By June, cumulative imports reach about 1.66 million tonnes, or close to 62 per cent of the annual total.

For the Australian fertiliser market, the key question is timing. While only a modest share of annual imports typically arrives by the end of March, the bulk of shipments required for the winter cropping season normally occur in the April to June window. If Middle Eastern supply remains restricted into April, importers will have to scramble to source alternative tonnes from Asia or other producing regions.

The real pressure point for the supply chain, therefore, sits between late April and early May. Beyond this point, shipping lead times begin to collide with fertiliser application schedules. If a significant Gulf supply is still unavailable by then, the market could face increasing difficulty replenishing stocks before winter crop demand peaks.

When will the supply arrive?

The conflict in the Middle East has triggered a chain reaction across global urea production, not only impacting production in Iran but also affecting other production plants. The most significant outage has occurred in Qatar, where production at a major facility has been halted following strikes on energy facilities. This plant alone has a capacity of roughly 5.6 million tonnes per year, meaning its closure immediately removes a large volume from the global export market.

The situation in Iran is also highly uncertain, with the war raging on and communications severely limited due to internet blackouts. However, due to the damage to energy infrastructure, we can expect little production and no safe access at present.

Further afield, the conflict has also created indirect production losses. In Bangladesh, a gas shortage linked to wider energy disruptions has forced the shutdown of five of the country’s six urea fertiliser plants, leaving only one facility operating. We are also hearing that European plants are reducing their output due to high gas prices.

Even if these plants resume production, supply will not return immediately. Fertiliser factories require time to restart operations and stabilise output, while many producers will first move existing stock before rebuilding export volumes. Shipping adds another layer of delay. Although some assurances have been discussed regarding vessel security through the Strait of Hormuz, shipowners and insurers are likely to remain cautious. As a result, even if transit resumes soon, freight flows will likely recover slowly, creating a lag before normal supply patterns return to the market.

The key to getting supply back in order is a sharp resolution to this conflict. A major conflict in the Middle East was always going to lead to price escalation due to supply constraints. The longer and more destructive the conflict, the longer and more impactful it will be on Australian producers.

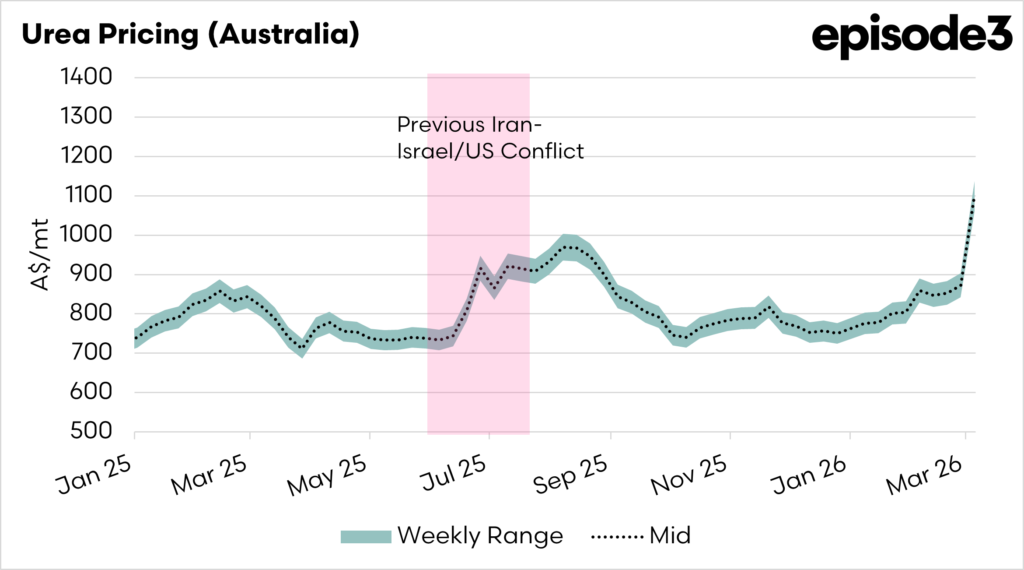

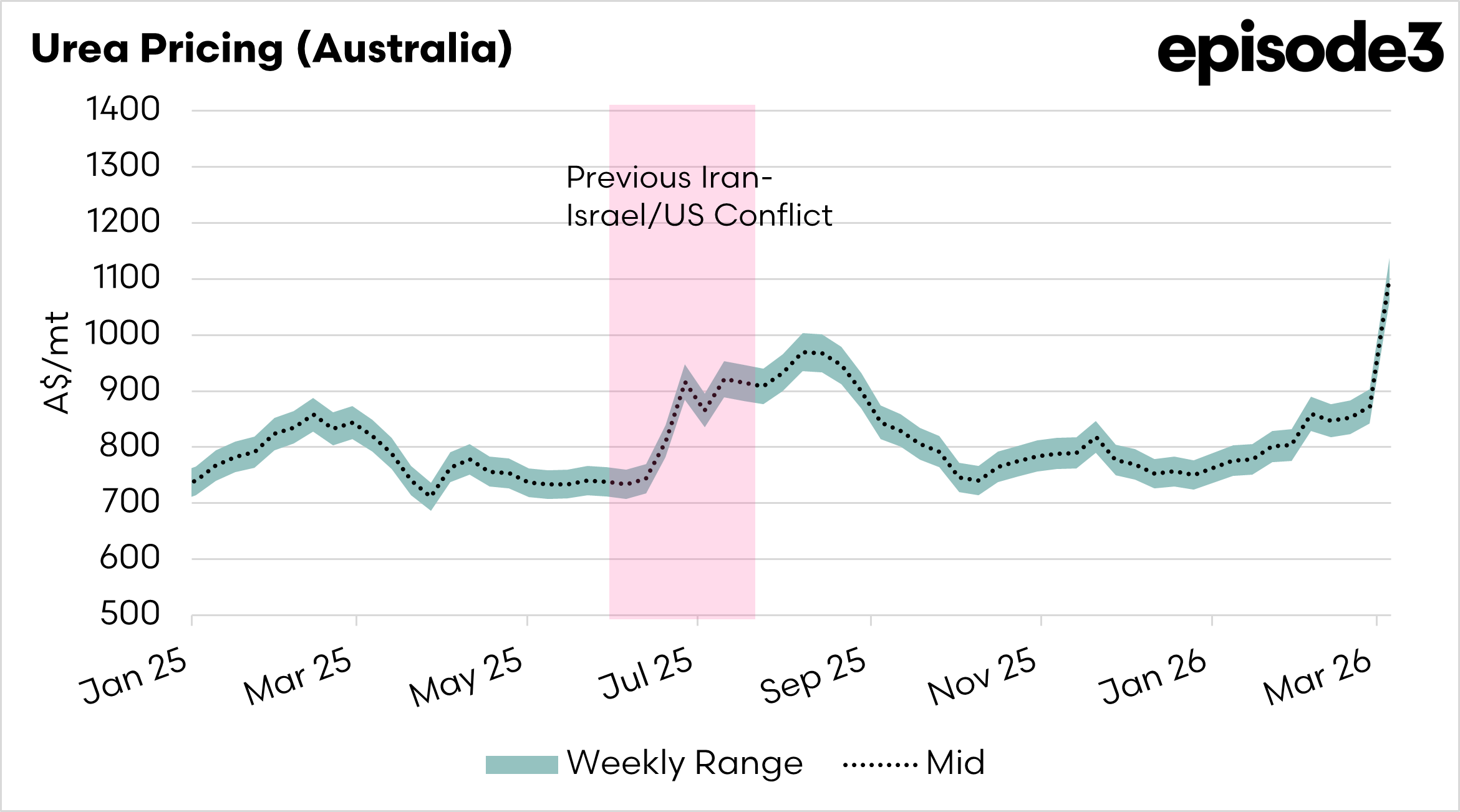

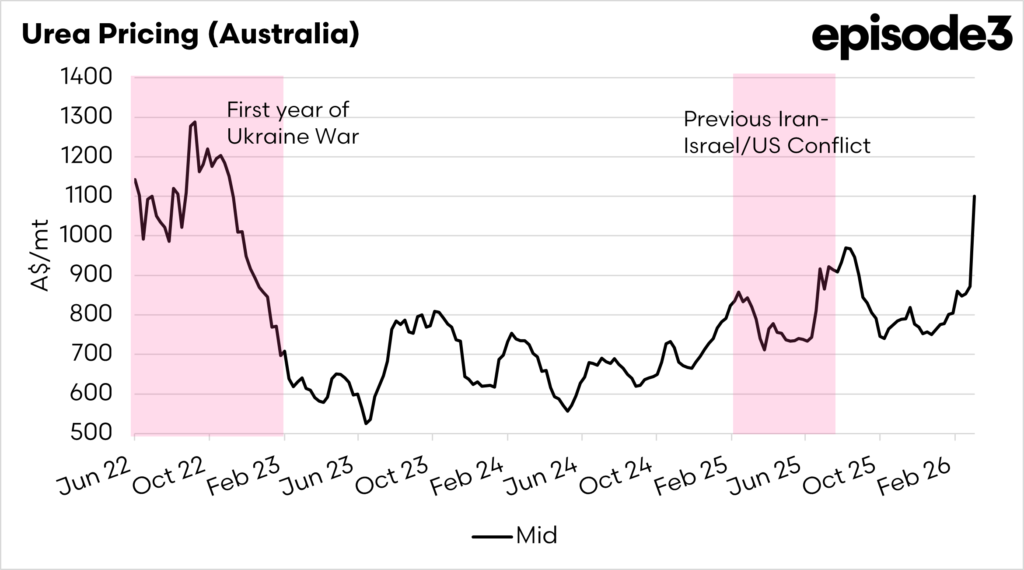

What is the price doing?

At episode3.net, we publish a fair value model for Australian urea each week, which we have provided to the industry since mid-2020. This was launched in response to the lack of transparency in the local fertiliser industry.

This provides an independent, data-centric view of the price of urea in Australia; we don’t trade the commodity. To provide this, we gather the price of purchasing urea in the Middle East, along with the cost of freight, unloading, and a margin, which we have calculated from our urea census. This is then assessed against the ABS import average price, which is released every couple of months.

The current model price from the end of last week, which uses a week average price, is now sitting above A$1100/mt. which has been an increase of over A$200 in the past week. The bad news is that I think this is likely to go higher this week. The reality is that the prices being quoted are unlikely to be ‘real’ prices. Whether this urea is accessible remains the question as we move into the second week of this conflict, with a resolution far off and prices rising further. It would not be surprising to see this conflict exceed the highs experienced during the early days of the Ukraine invasion, where gas prices rose significantly.

Fundamentally, the current situation is far worse than during the Ukrainian invasion, which will place us in a world of pain going forward. Price is an issue and makes cropping expensive, but the lack of access to supply will be far worse.