Beef processors push hard as cattle flow shifts

Get short video updates on your phone

For quicker updates as markets move, follow @themeatwatcher on Instagram. I regularly post short summaries and charts breaking down what’s happening in meat proteins and broader ag markets so you can stay across the key moves without having to read through pages of analysis. If markets are moving quickly, that’s usually where the updates will land first.

Market Morsel

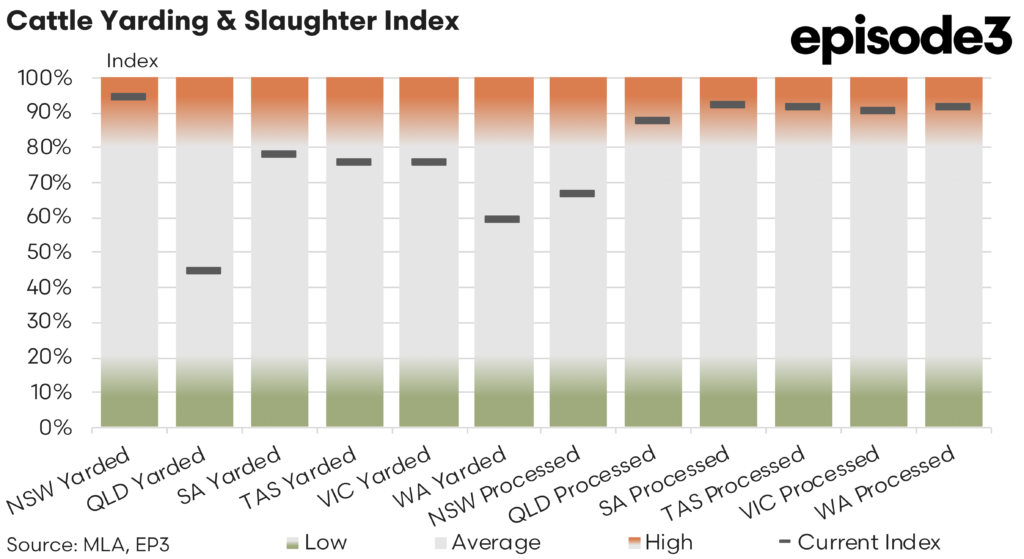

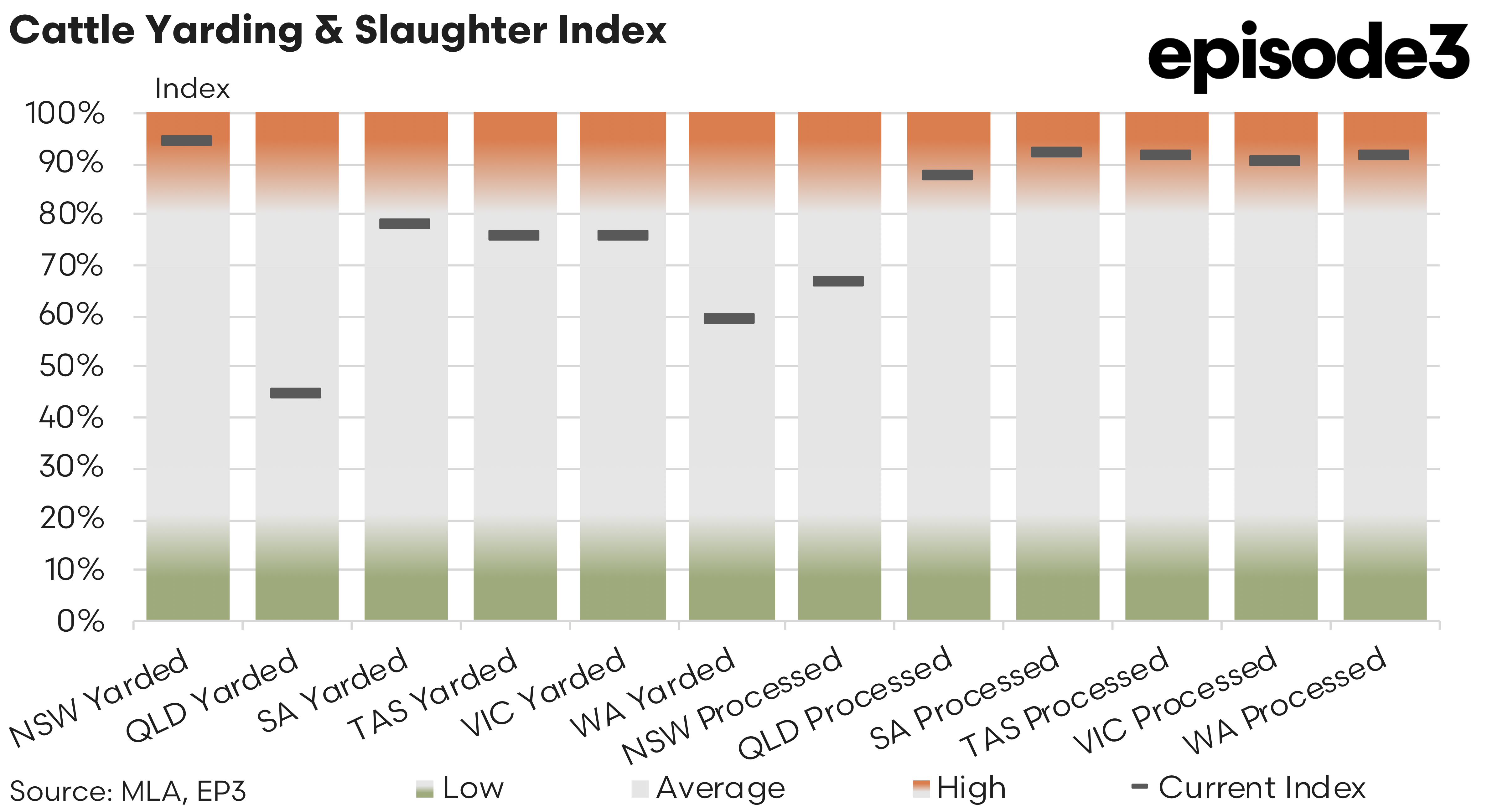

The latest movement in yarding and processing indicators between January and February provides a clearer picture of how the cattle market has settled into 2026, revealing a system that has normalised after the seasonal slowdown but is beginning to display the early characteristics of tightening supply. While activity has lifted sharply across most regions, the underlying story is less about abundance and more about changing producer behaviour and increasingly uneven cattle availability.

January traditionally represents the low point in physical market activity each year. Plant shutdowns, reduced saleyard operations and holiday disruptions suppress both yardings and slaughter, often giving a misleading impression of market weakness. The February index results confirm that this year followed the same pattern. Once normal operating conditions resumed, cattle flows recovered quickly across the country.

New South Wales yardings rose from an index level of 64 in January to 94 in February, effectively returning to near full seasonal capacity. South Australia and Victoria showed similar rebounds, lifting to 78 and 76 respectively, while Tasmania also recovered strongly. Queensland improved from extremely subdued January levels but remained comparatively lower at 45, reinforcing the emerging regional split in supply conditions. Western Australia moved in the opposite direction, with yardings easing from 71 to 59, suggesting local availability tightened even as eastern states saw improved flows.

Processing activity followed an even stronger recovery. Queensland processing surged from 15 in January to 87 in February as plants resumed normal kills following holiday interruptions. New South Wales lifted from 41 to 67, while Victoria, Tasmania and South Australia all operated close to or above 90 percent of normal processing capacity. Western Australia processing increased modestly from 85 to 91 despite lower yardings, indicating processors were maintaining throughput by drawing more heavily on available cattle rather than relying on increased marketings.

The index movements reinforce the theme that has been building through recent months. The national market is no longer moving uniformly. Instead, cattle supply is becoming increasingly regionalised, with southern processors carrying a larger share of slaughter activity while northern flows remain more variable. Seasonal conditions have played a central role in shaping this outcome. Rainfall across parts of the country has reduced selling urgency, allowing producers to hold cattle back even as processors attempt to rebuild chain speed following the summer break.

Weather has added another layer of complexity. Rainfall events have disrupted the timing of cattle movements, creating short term fluctuations in weekly supply without fundamentally altering broader availability. Some regions have seen marketing delayed as paddock conditions improve, while others continue to supply cattle steadily. The result is a market characterised less by volume swings and more by timing variability, forcing processors to adjust procurement strategies week by week.

The February data therefore does not point to a shortage of cattle in an absolute sense. Instead, it suggests the industry is transitioning away from the uniform oversupply conditions that defined the liquidation phase. Processors are running hard, yardings have rebounded seasonally, yet pricing remains firm and in some cases strengthening. Historically, this combination signals that forward supply visibility is becoming less certain even before total numbers decline.

What emerges is a market entering the middle stage of the livestock cycle. The liquidation phase that drove elevated slaughter across recent years appears to be fading, replaced by a more balanced environment where regional conditions, seasonal confidence and procurement competition play a larger role in price formation. Southern states currently hold the throughput advantage, but tightening signals are beginning to appear beneath the surface.

If these trends persist, the implication for the remainder of 2026 is gradual rather than abrupt change. Slaughter volumes may remain relatively strong in the near term as cattle already in the system continue to flow, yet the underlying breeding base is no longer expanding supply at the same pace. As producer retention slowly increases and marketing becomes more selective, competition for suitable slaughter cattle is likely to intensify.