Feedlot update Q4, 2025

December 2025 cattle on feed update

The December quarter tends to cut through the noise and show what actually mattered across the year. In 2025, the feedlot data does exactly that. Strip it back and the story is not just one of growth, but of a system that has become tighter, faster and more central to how Australian beef is produced.

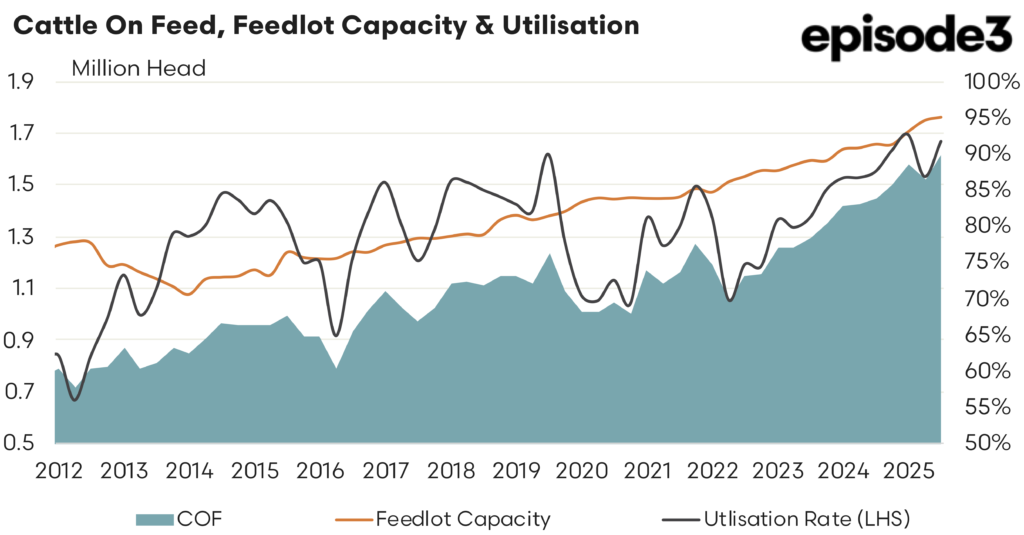

The headline numbers set the tone early. Feedlot capacity continued its steady climb, pushing out towards roughly 1.75 million head by the end of the year. At the same time, cattle on feed lifted to around 1.6 million head in the December quarter, leaving utilisation sitting in the low 90 percent range. When you line those three together, the message is clear. Expansion is still happening, but it is being absorbed almost immediately. The system is not building slack, it is running close to full.

Through the back half of the year, cattle on feed continued to push higher, tracking alongside that lift in capacity. The key point is how little daylight now exists between the two. When you look at the longer-term trend, the expansion has been consistent, but what stands out in 2025 is how quickly new capacity has been filled. This is no longer a sector building ahead of demand. It is one being pulled forward by it.

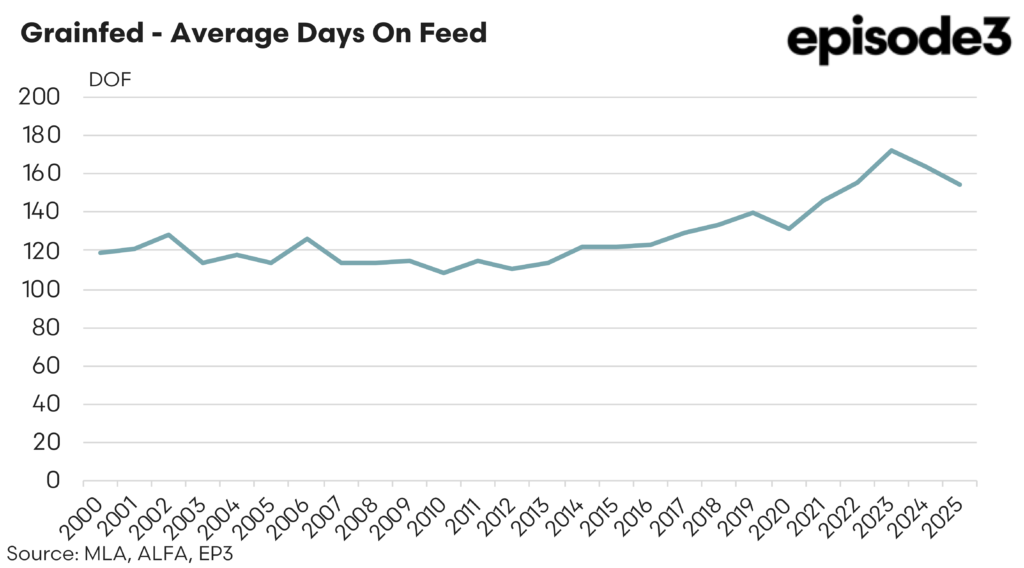

What changed more meaningfully over the year was not the size of the system, but how it was operated. Average days on feed pulled back from 164 days in 2024 to 155 days in 2025. After several years of cattle being held longer to chase weight and quality premiums, that shift lower signals a change in mindset. The long-run trend still shows a move towards longer feeding programs, but the recent peak and pullback highlights a pivot. Feedlots have not stepped away from production, they have simply become more conscious of how long they carry risk.

That adjustment makes sense in the context of the year that was. Feeder cattle prices lifted strongly, while input costs remained volatile. Holding cattle for longer became harder to justify when margins were under pressure. The response has been to increase turnover rather than stretch feeding periods. When you look at the data over time, the lift in days on feed through the early 2020s is clear, but so too is the correction in 2025. It is a small move in absolute terms, but a meaningful one in how the system behaves

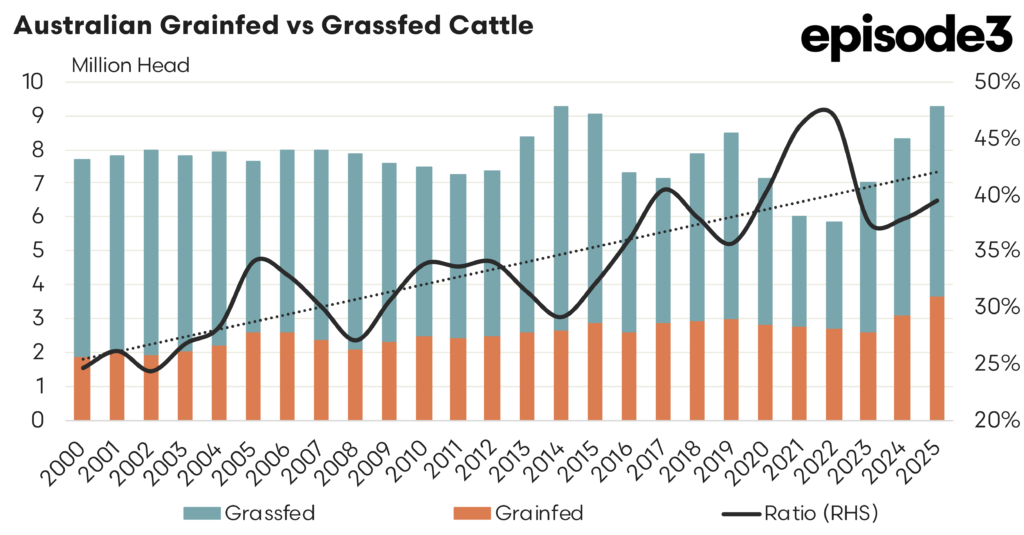

The other piece that defines 2025 is how much of the national kill is now coming out of feedlots. Total cattle slaughter reached 9.278 million head, and of that, 3.662 million were grain finished. That equates to 39.5 percent of the total kill, up from 37.9 percent the year before. The trend has been building for a long time, but the latest lift reinforces that grainfed production is no longer a niche or even a supplementary component. It is becoming the backbone of supply.

When you step back and look at the relationship between grainfed and grassfed production over time, the direction is clear. Grassfed still dominates in absolute terms, but the grainfed share continues to edge higher. The ratio has been climbing steadily, and 2025 adds another step in that progression. This is less about a decline in grassfed cattle and more about the role feedlots now play in delivering consistency to the market.

That consistency has become increasingly important. Export markets are demanding reliable volumes with tight specifications, and feedlots are the mechanism that delivers it. Seasonal variability still impacts the broader herd, but the feedlot system smooths that variability out. In a year where conditions and costs were far from stable, that role became even more pronounced.

The December quarter brings these themes together. High utilisation, strong placements and strong turnoff all occurred at the same time. The system was not easing off, it was operating at pace. The lift in grainfed share of slaughter, combined with shorter days on feed, points to a sector that is prioritising throughput and efficiency over simply holding cattle longer.

That is the key shift in 2025. The feedlot sector is still expanding, but it is also maturing. It is not just about adding capacity or pushing cattle to heavier weights. It is about moving more cattle through the system, more efficiently, and with tighter control over risk.

The end result is a sector that is larger, faster and more embedded in the supply chain than it has ever been. The December quarter does not change that story. It confirms that feedlots are now doing more of the heavy lifting in Australian beef production, and doing it with a sharper eye on margin than in years gone by.