Sheepmeat export update Aprill 2026

April 2026 - Sheep Meat Export Update

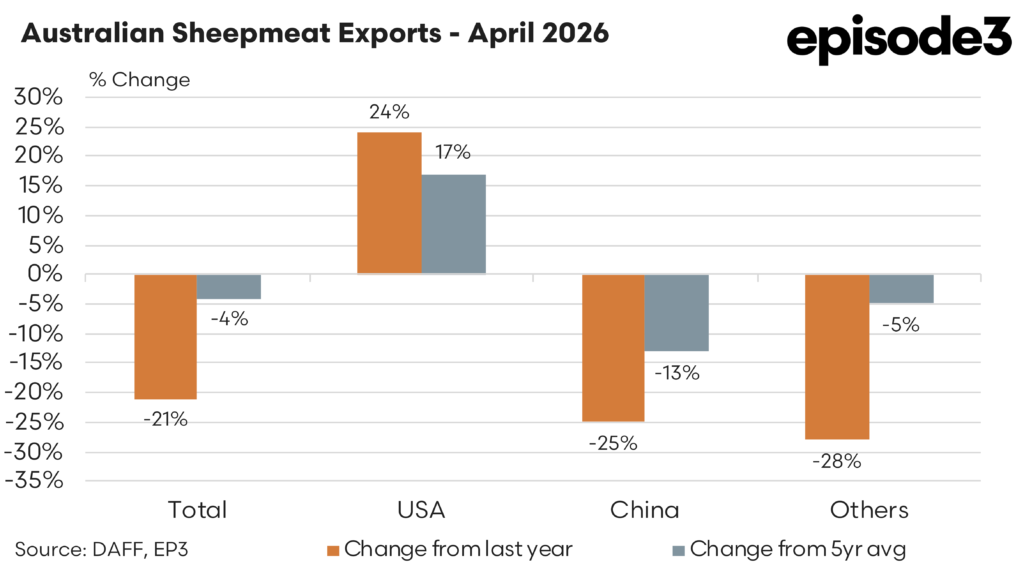

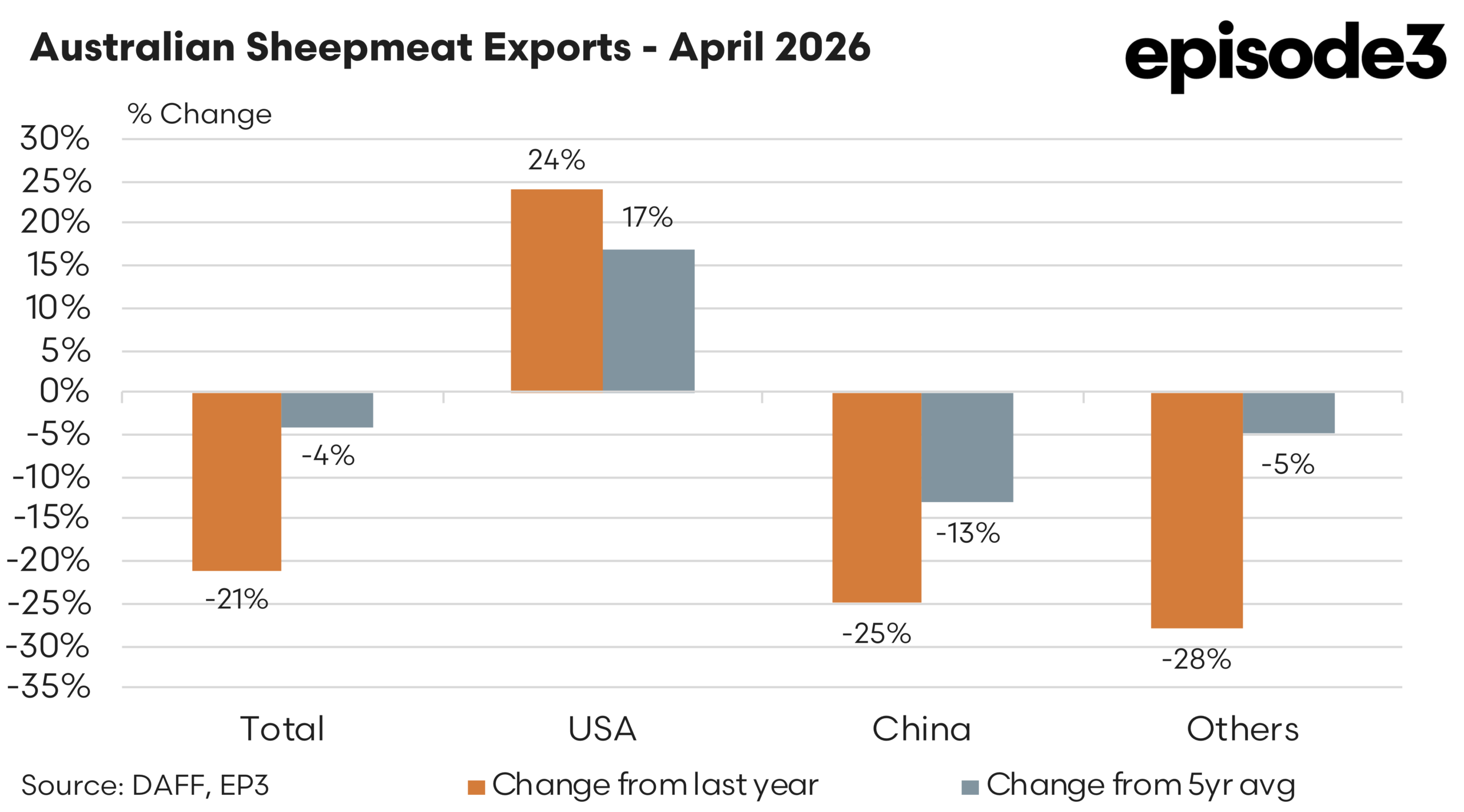

Australian sheepmeat export flows remained subdued in April 2026, with total combined lamb and mutton shipments reaching 38,866 tonnes. This represented a 21 percent decline compared with April last year and placed exports 4pc below the five year average for the month.

The result continues the softer trend that emerged through March and reflects ongoing disruptions across several key markets, particularly within the Middle East and North Africa (MENA) region. Despite this, export demand remains relatively balanced across the major destinations, helping to cushion the broader decline in flows

The United States again stood out as the strongest performing major market for Australian sheep meat. Exports totalled 8,035 tonnes in April, up 24pc compared with last year and 17pc above the five year average.

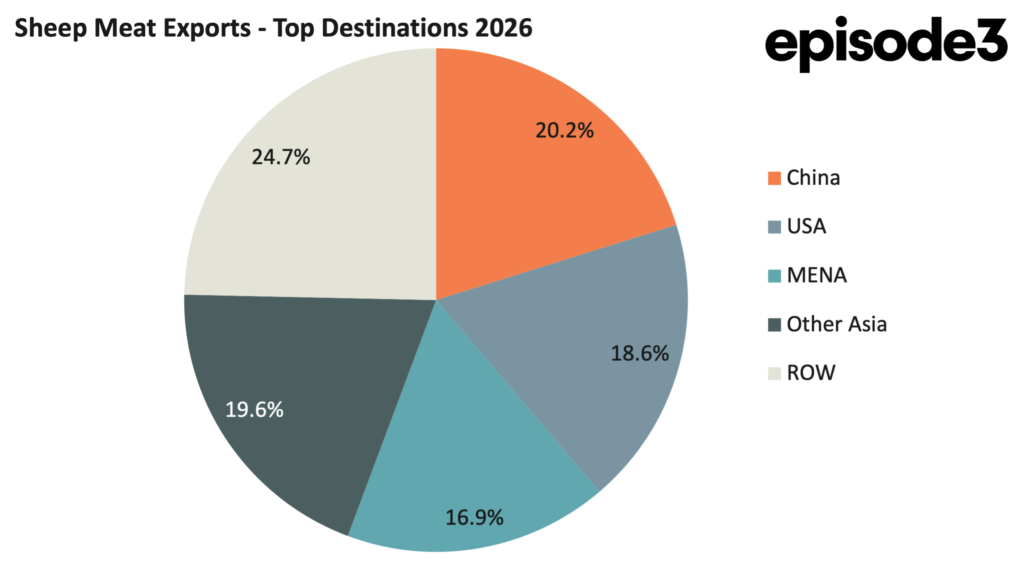

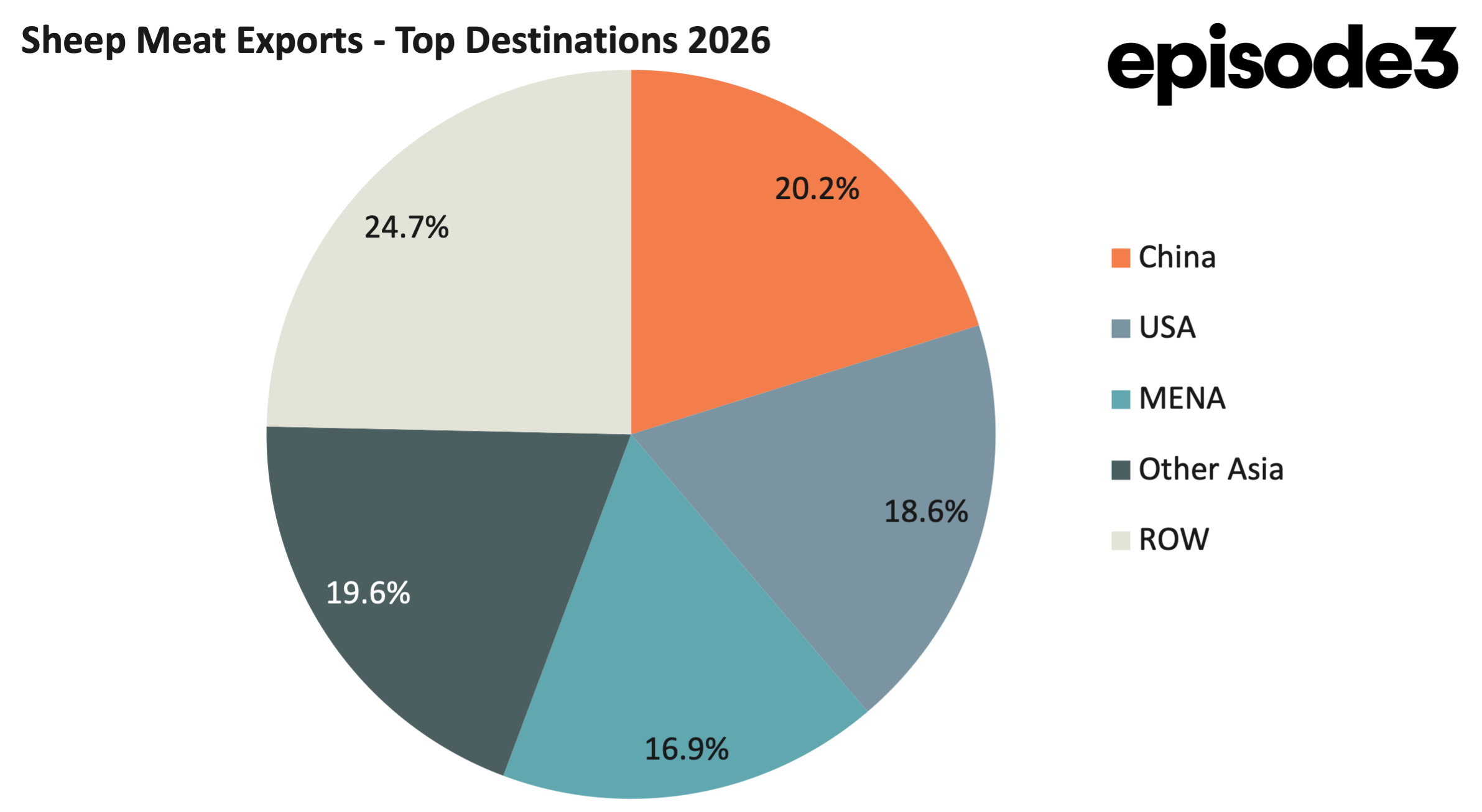

The continued growth into the US highlights the structural strength of demand, particularly for higher value lamb cuts, and reinforces the market’s growing importance within Australia’s export mix. The US now accounts for 18.6pc of total sheep meat exports in 2026, sitting only marginally behind China and confirming its role as one of the core pillars of the trade.

China remained the largest individual destination in April, taking 8,810 tonnes of lamb and mutton combined. However, export volumes softened materially compared with earlier in the year, declining 25pc from April last year and sitting 13pc below the five year average. Despite the decline, China still accounted for 20.2pc of total exports year to date, highlighting its ongoing significance even amid more volatile monthly demand patterns.

Exports to all other destinations combined totalled 22,021 tonnes in April. Volumes were 28pc lower than last year and 5pc below the five year average. Much of this weakness again stemmed from ongoing disruptions and reduced buying activity across the MENA region, particularly within lamb markets.

Lamb exports to Qatar were 42pc below the five year average for April, while lamb shipments to the United Arab Emirates were down 40pc and Jordan was 20pc lower. These declines continue the pattern of subdued trade flows into parts of the region that first became apparent in March.

The picture for mutton exports across the MENA region was more mixed. Saudi Arabia recorded mutton flows 32pc above the five year average for April, while the United Arab Emirates also saw stronger mutton demand, with exports running 26pc higher than normal levels.

In contrast, Oman remained significantly weaker, with mutton shipments 69pc below the five year average, while Kuwait sat 19pc lower.

This divergence between lamb and mutton demand suggests the disruption across the region is not uniform and may reflect differing consumption patterns, pricing dynamics or access conditions between product categories and individual markets.

The broader distribution of export market share continues to highlight the relatively diversified nature of Australia’s sheep meat trade in 2026. China holds a 20.2pc share of year to date exports, closely followed by the United States at 18.6pc. The MENA region still accounts for 16.9pc despite the recent disruptions, while other Asian markets contribute 19.6pc.

The remainder of the world collectively accounts for 24.7pc of shipments. This relatively even spread across destinations provides an important degree of resilience, ensuring that weakness in one region does not entirely dictate overall export performance.

April 2026 confirms that Australian sheep meat exports are navigating a more challenging trading environment than was evident earlier in the year. Strong demand from the United States continues to provide support, but softer Chinese buying and ongoing disruptions across parts of the MENA region are weighing on total volumes.

The relatively balanced export portfolio remains a key strength, though the pace of recovery in Middle Eastern demand will likely play an important role in shaping export performance through the remainder of 2026.