Sheep slaughter tightens, lambs mixed

Market Morsel

The latest slaughter data shows that the sheep and lamb market is continuing to diverge as we move from February into March, with tightening sheep supply becoming more pronounced while lamb availability remains more uneven across the country.

Sheep slaughter trends across the major producing states reinforce the view that the post spring drawdown of stock is still underway and, in several regions, accelerating.

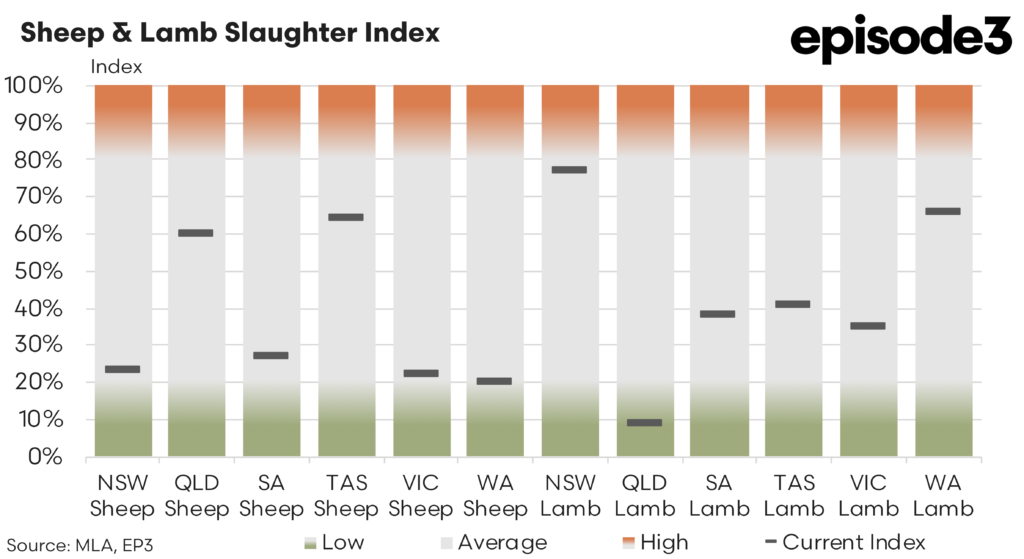

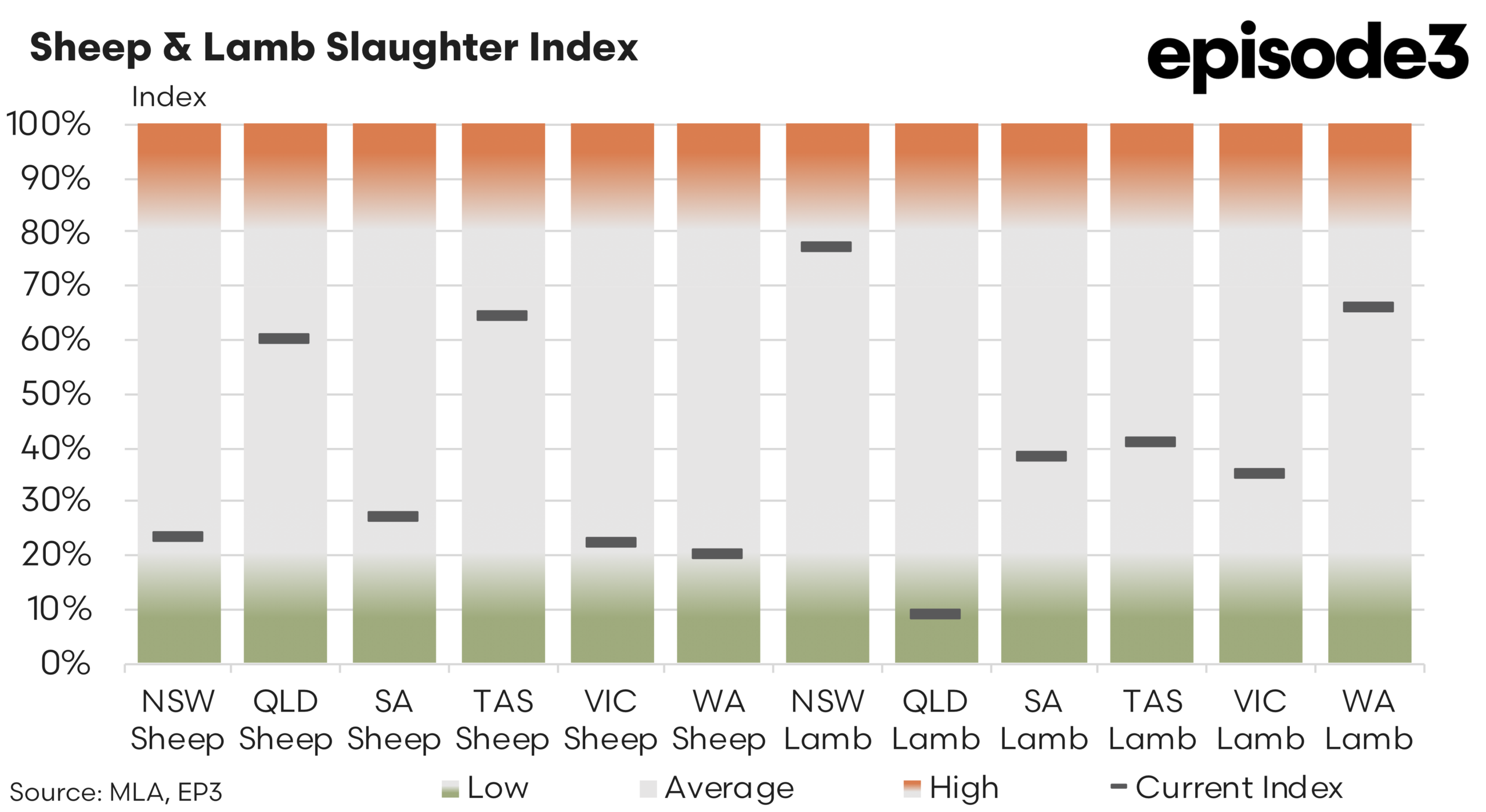

New South Wales sheep slaughter has fallen from 37 percent in February to 23pc in March, a significant drop that signals a clear tightening in availability as earlier turnoff has now worked through the system. Western Australia shows a similar pattern, easing from 25pc to 20pc, which points to a continued contraction in supply following relatively steady processing earlier in the season.

Tasmania has also seen a sharp decline, dropping from 91pc to 64pc, suggesting that even regions which were processing strongly are now seeing throughput come back as supply tightens.Victoria has followed the same direction, falling from 47pc to 22pc, reinforcing that the southern mainland is now firmly moving into a tighter sheep supply phase.

The exception to this trend is Queensland, where sheep slaughter has lifted from 57pc to 60pc, indicating that supply conditions there are lagging the southern states and that producers are still bringing stock forward. Although it is important to note that Queensland sheep meat processing is a fraction of the other key states of NSW, Victoria, SA and WA.

While sheep slaughter is clearly tightening, lamb slaughter trends present a more mixed and complex picture.

New South Wales lamb slaughter has surged from 51pc in February to 77pc in March, suggesting that processors are still able to draw on a solid pool of available lambs.Western Australia has also lifted from 53pc to 66pc, reinforcing that lamb supply in some regions remains accessible despite the broader seasonal shift.

South Australia has moved higher as well, rising from 24pc to 38pc, which suggests that producers may be favouring lamb turnoff over sheep as conditions tighten. In contrast, Queensland lamb slaughter has dropped sharply from 23pc to 9pc, indicating a rapid tightening in that state after earlier availability.

Victoria has also eased from 48pc to 35pc, pointing to a moderation in throughput even though volumes remain relatively solid compared to sheep. Tasmania shows a decline from 79pc to 41pc, highlighting that even regions with strong earlier flows are now seeing lamb supply ease.

The lamb data suggests that while the spring flush has clearly passed, there is still enough supply in parts of the country to keep processing levels elevated, particularly in New South Wales and Western Australia.

Weaker export demand since the start of 2026 in key mutton markets, like China, is flowing through to softer pricing despite the tightening mutton supplies. It also highlights that the sheep market often lags lamb in terms of price response, even when supply signals are pointing in the same direction. The divergence between sheep and lamb is one of the key features of the current market.

Sheep supply is tightening rapidly across most major producing regions, yet prices have only stabilised rather than lifted meaningfully. Lamb supply, while no longer expanding, remains sufficiently available in some regions to support strong processing levels, yet prices are already trending higher. This suggests that the lamb market is more responsive to tightening conditions, or that export demand dynamics for lamb are providing stronger underlying support.