Government backs fertiliser imports, farmers gain certainty, taxpayers take the exposure

The Snapshot

- Government underwriting should help ensure fertiliser arrives ahead of planting

- It reduces risk for importers and encourages cargoes onto the water

- Farmers benefit from improved supply certainty at a critical time

- The structure raises unanswered questions around pricing and oversight

- Taxpayers are effectively carrying the downside risk if markets move

The Detail

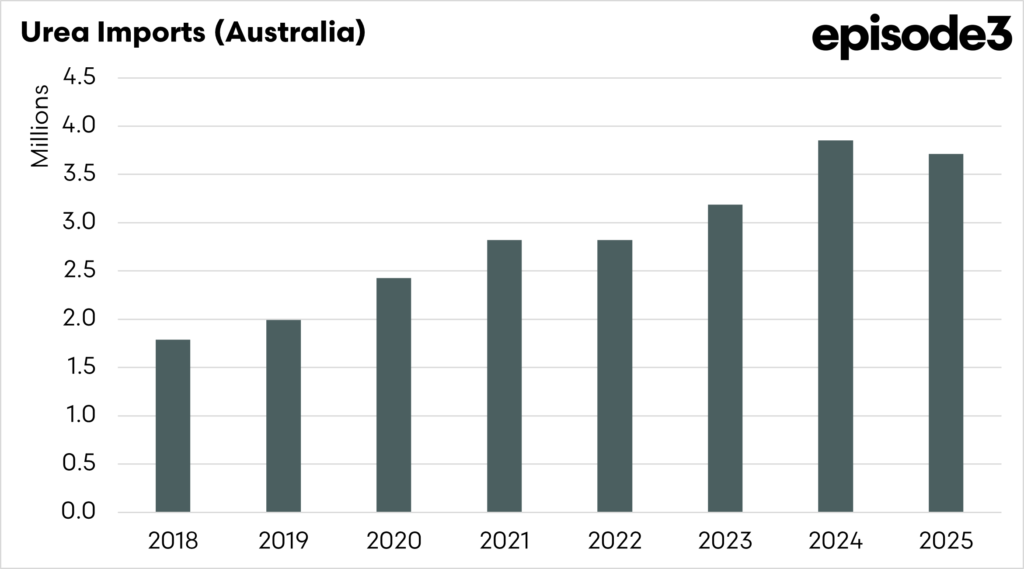

The federal government’s move to underwrite fertiliser imports is, at its core, a practical response to a stressed system. With disruption through the Strait of Hormuz tightening global supply chains and pushing volatility into both fuel and fertiliser markets, the private sector has been reluctant to take on large import positions. In that context, stepping in to de-risk the equation makes sense. Farmers need product on farm, and timing is everything.

The mechanism itself is relatively straightforward from what we have seen so far. The government is acting as a backstop. If an importer commits to cargo at elevated global prices and the market falls before it is sold domestically, the loss is absorbed or offset. That shifts the downside risk away from the importer and onto the public balance sheet. In effect, it changes the decision from high-risk speculation to a more managed trade.

From a farmer’s perspective, this is clearly positive. The biggest immediate risk in recent weeks has not just been price, but availability. Without fertiliser, yield potential falls quickly, and in some cases, planting decisions are deferred or cancelled altogether. By encouraging importers to move, the policy improves the likelihood that tonnes actually land in Australia in time for the season. That alone restores a degree of confidence across the supply chain.

It also aligns with the broader reality that Australian agriculture is heavily dependent on imported inputs. When global trade flows are disrupted, the domestic system has limited buffers. Policies that smooth volatility can play an important role in maintaining production, particularly in years when seasonal risk is already elevated.

However, once you move past the immediate benefit, the structure raises a second set of questions, and these sit squarely with taxpayers rather than farmers.

The first is the nature of the support itself. While not a direct payment, underwriting losses behave like a subsidy in economic terms. It lowers risk and changes behaviour. Importers are more willing to commit to volume because the downside is partially removed. That is the intended outcome, but it also means public funds are now exposed to market movements that would normally be borne by private companies.

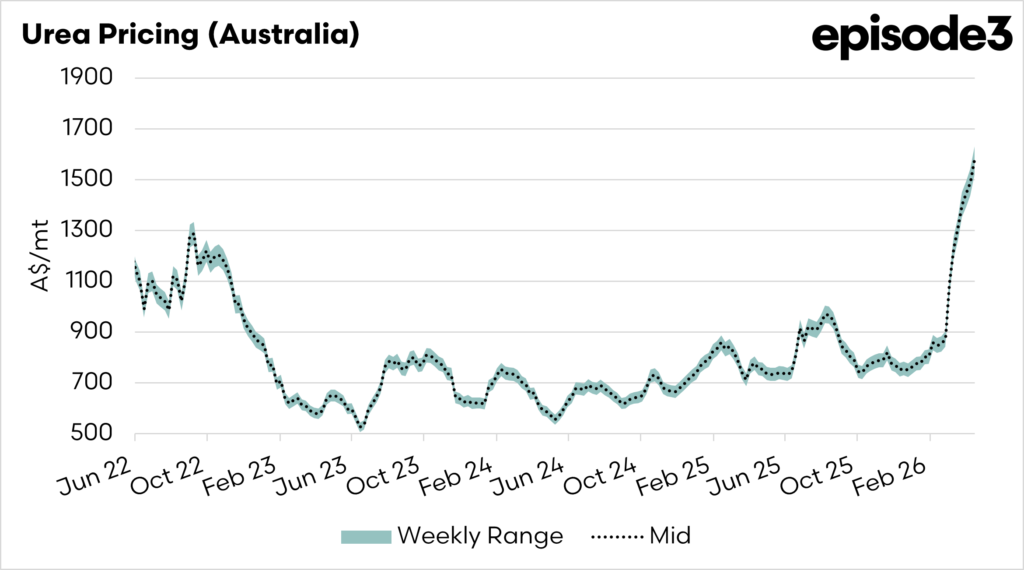

The second, and more complex issue, is price discovery. Fertiliser markets are not as transparent as grain or oil markets. There is no single domestic benchmark that clearly defines value at any given point in time, other than the Episode 3 pricing model. Pricing is based on a mix of international references, negotiated cargo values, and the timing of sales. In that environment, determining when a loss has actually occurred is not straightforward.

This leads directly to the key governance question. Who verifies the numbers? Who determines the import price? Who determines the realised sale price? And what benchmark is used to bridge the two? Without clear answers, the scheme relies heavily on internal processes that are not visible to the broader market.

That is where the question of oversight becomes unavoidable. If taxpayers are underwriting the downside, there needs to be confidence that the system is robust, consistent, and independently verifiable. Otherwise, even if the policy works as intended, it risks creating unease about how fairly the risk and reward are being shared.

There is also a longer term consideration. Measures like this, while justified in a crisis, can blur the line between market function and government intervention. Under the framework of the World Trade Organisation, the policy is likely defensible as a temporary response to supply disruption rather than a direct export subsidy. But design and transparency will matter, particularly if trading partners begin to scrutinise how support flows through the system.

There is a recent precedent that highlights how these situations can evolve. In 2020, China imposed tariffs on Australian barley, arguing that domestic support measures had distorted trade and pricing. While the fertiliser underwriting is structurally very different, being aimed at inputs rather than outputs, it shows how quickly policy settings can be interpreted through a trade lens when relationships deteriorate. The risk here is not that this measure directly breaches rules, but that it could be viewed, rightly or wrongly, as part of a broader pattern of support that enhances competitiveness. In a more strained geopolitical environment, that feeling alone can be enough to trigger scrutiny.

The immediate outcome is clear. This increases the probability that fertiliser arrives when it is needed, and that is a win for farmers heading into a critical planting window.