Processor trading conditions update

Beef Processor Trading Conditions - January 2026 update

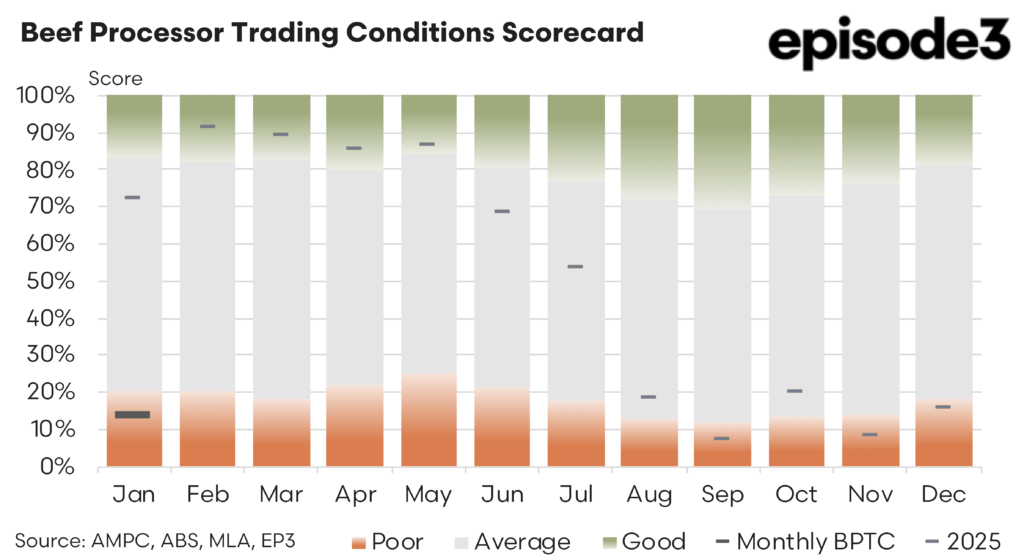

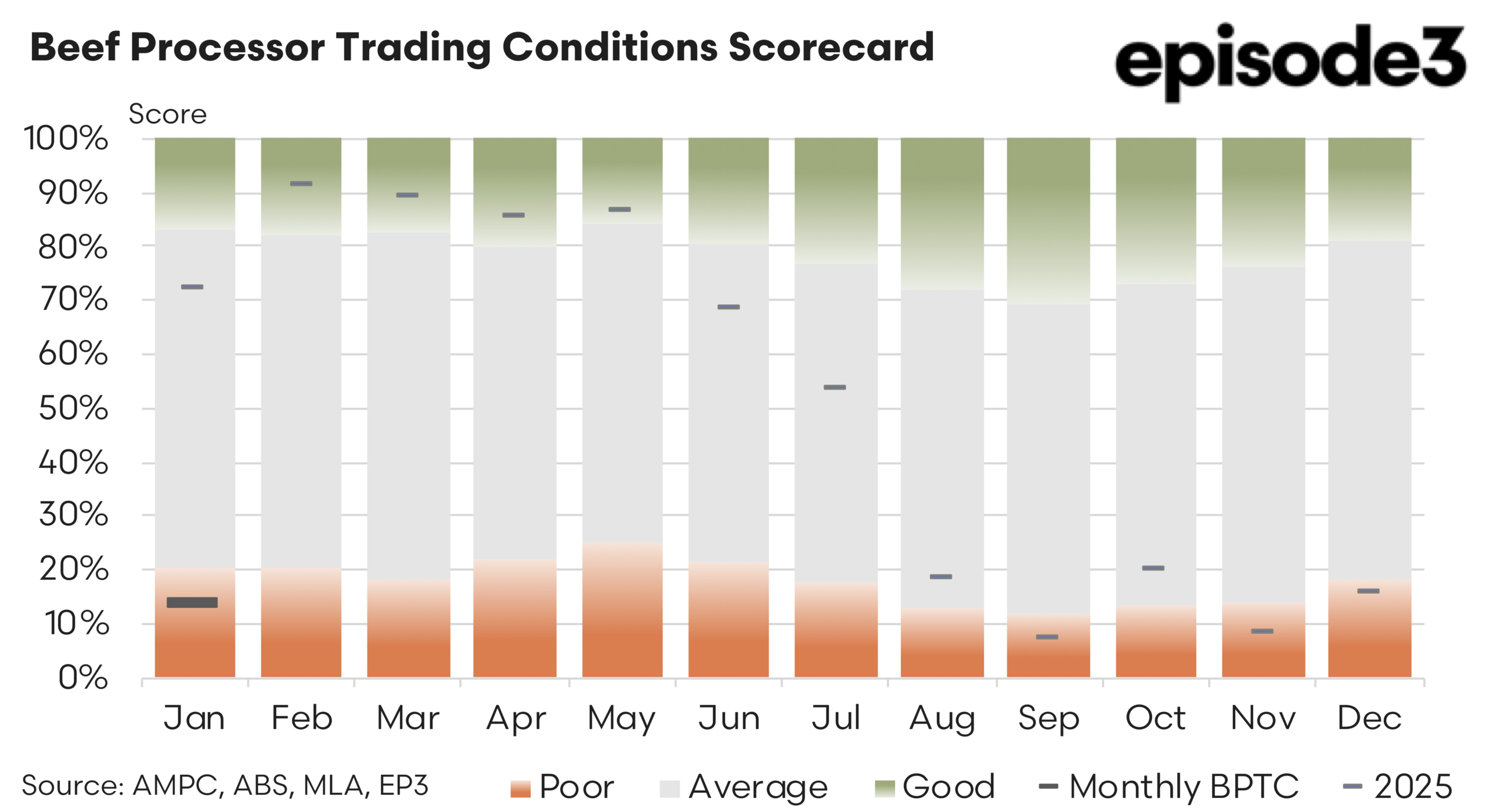

Beef processor trading conditions eased through January 2026, with the BPTC index slipping to 14 percent, down from 16pc in December. This marks a continued cooling in processor margins and a stark contrast to the elevated conditions seen just twelve months earlier, when the index sat at 72pc. The shift highlights how quickly the processing sector has moved from highly favourable conditions into a more constrained operating environment.

While margins remain positive, the compression over the past year has been significant and broad based. Cattle input prices were mixed across categories, but generally moved against processors. Heavy steer prices declined by 1.1pc over the month, offering some modest relief in procurement costs. Young cattle prices also softened, with the category easing by 2.2pc. However, this easing was not sufficient to materially improve processor margins. Processor cow prices fell by 2.2pc, which typically provides some support to manufacturing beef margins, but again the magnitude of the move was limited.

The more meaningful pressure came from the export side of the ledger. Returns across key international markets weakened through January, directly impacting revenue. The United States, a cornerstone market for Australian beef, saw returns decline by 3.5pc. Japan experienced a sharper fall, down 9.8pc, reflecting softer demand conditions and increased competition. South Korea also moved lower, easing by 4.5pc over the month. China was the only major market to record an increase, rising by 1.1pc. However, this was not enough to offset the broader declines across the export complex. When combined, the top four export markets recorded a decline of 4.0pc. This aggregate move underscores the extent to which weakening global demand has weighed on processor returns.

On the cost side, there were modest increases in key areas. Manufacturing costs in the food sector rose by 1.0pc, adding incremental pressure to processing margins. Retail beef prices lifted by 1.5pc, which may support downstream returns, but does little to offset immediate processor cost pressures. At the same time, other cost components remain elevated, even where monthly changes appear modest.

Energy, labour, and compliance costs continue to sit at levels that are materially higher than historical averages. Co-product values were not updated for the month, but remain an important swing factor in processor profitability. In prior periods, co-product strength has provided meaningful support to margins, and any change in this component would further influence overall conditions. The net result of these movements is a continued tightening in processor margins.

While cattle prices have shown some softness, the decline in export returns has had a larger impact on the overall margin equation. This dynamic is critical. Processor profitability is not driven solely by input costs, but by the spread between livestock prices and export values and during January, that spread narrowed. The decline in the BPTC index reflects this compression.

At 14pc, conditions remain positive, but only marginally so when compared to the highs of the previous year. The comparison to January 2025 is particularly telling. At that point, processors were operating in an environment of strong global demand, supportive co-product values, and relatively stable input costs. The 72pc reading reflected a period of exceptional profitability.

Twelve months on, the environment has shifted. Global demand has softened across several key markets. Input costs for cattle remain elevated and trading margins have weakened. This suggests that the sector has moved back into a more typical operating range, where profitability is more sensitive to incremental changes in market conditions.

Looking forward, the trajectory of processor conditions will depend on several key factors. Export market performance remains critical, particularly in the United States and North Asia. Any further softening in these markets would place additional pressure on margins.

Cattle supply will also play a role. If availability continues to improve, processors may gain further leverage on procurement costs. However, this must be balanced against the risk of weaker prices impacting producer behaviour and turnoff decisions. Cost pressures are another ongoing consideration. Even small increases in manufacturing or operating costs can have a disproportionate impact when margins are already compressed.

The January result therefore reflects a market that is finely balanced. Processor conditions are no longer being driven by strong tailwinds. Instead, they are being shaped by a combination of softer demand, mixed input price movements, and persistent cost pressures. The BPTC at 14pc captures this transition clearly. It is a market that remains functional, but far less forgiving than it was a year ago.