Cattle availability builds as processor leverage returns

Market Morsel

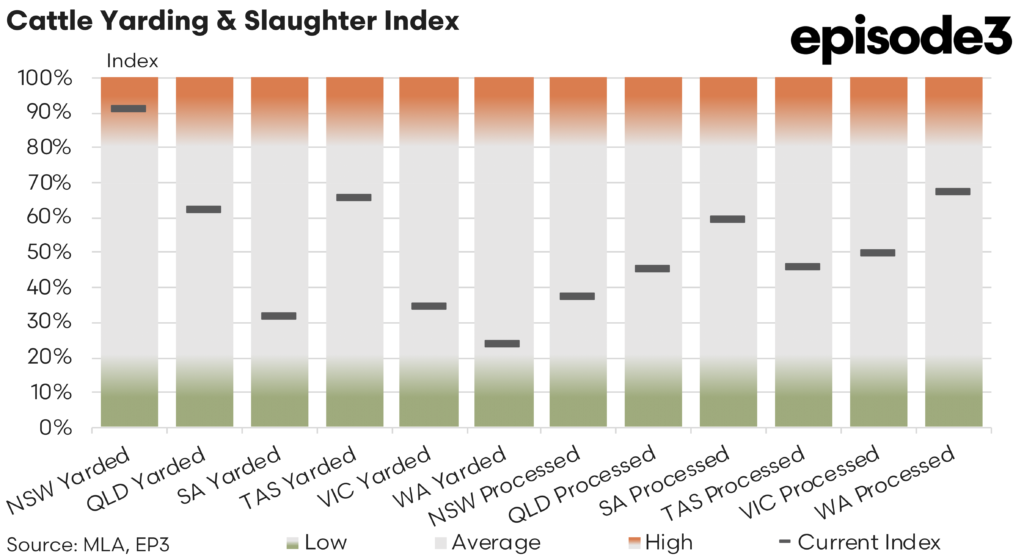

Cattle market signals through March and April show a system that has shifted rapidly, with rising supply now translating into heavy price pressure and a more uneven national picture. The latest yarding and slaughter indices reinforce that the lift in throughput seen through March has flowed directly into a noticeable reset in pricing. Through March, processors pushed hard to lift kills, particularly in New South Wales and Queensland.

Yardings in New South Wales reached 98 percent while Queensland sat at 55pc, providing the foundation for increased throughput. Processing activity followed, with New South Wales at 89pc and Queensland at 80pc, reflecting a period of strong operational intensity. This lift was not uniform across the country. Victoria, South Australia and Western Australia remained tighter, with lower yardings and less aggressive processing levels. The result was a fragmented supply picture where cattle availability improved, but not evenly.

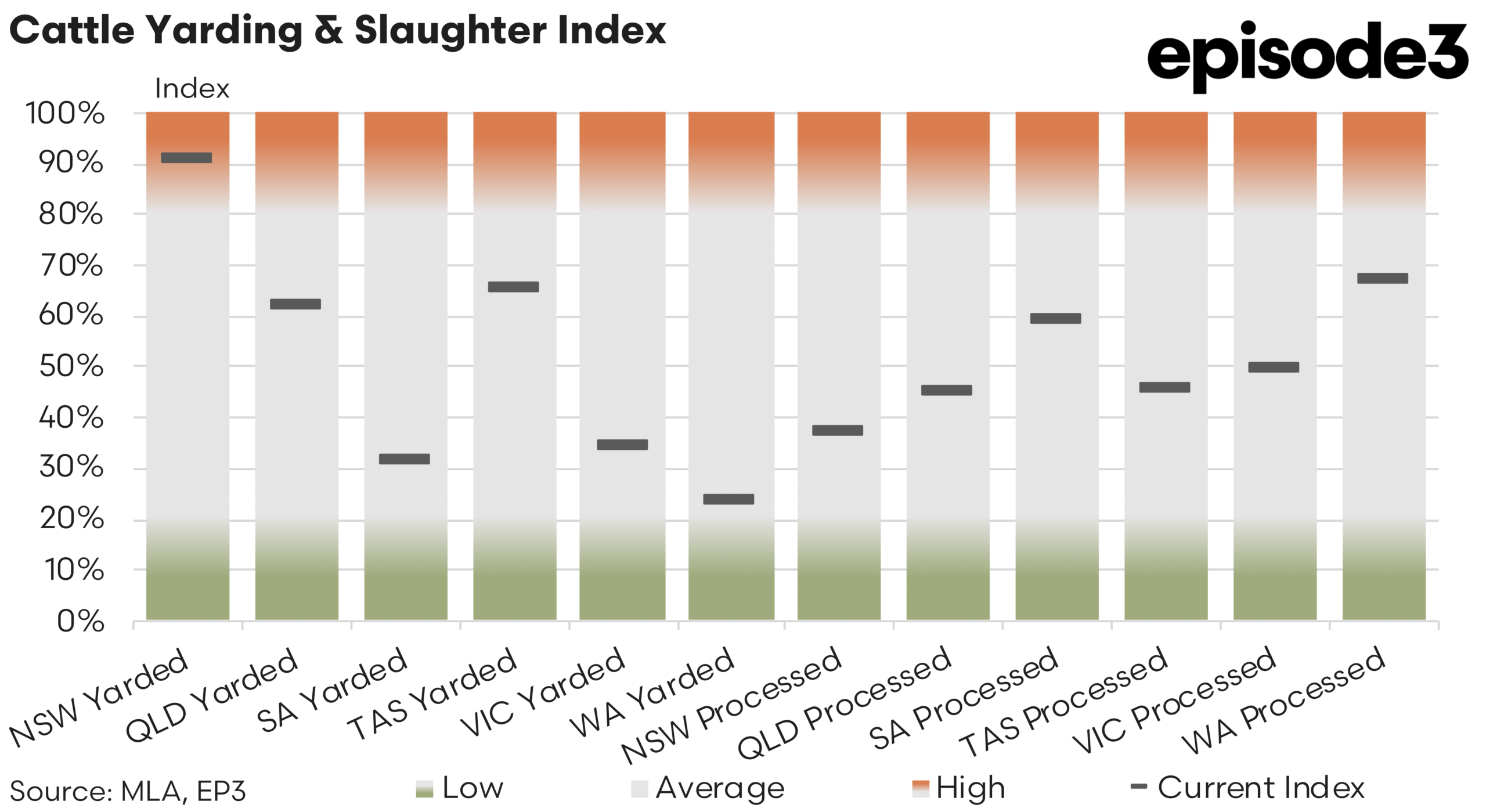

Moving into April, the data shows a clear change in both supply distribution and processor activity. New South Wales yardings eased from 98pc to 91pc, remaining elevated but off their peak. Queensland continued to build, rising from 55pc to 62pc, further consolidating its position as a key supply driver. Elsewhere, supply tightened significantly. Victoria fell from 61pc to 35pc, South Australia from 50pc to 32pc, and Western Australia from 47pc to 23pc. Tasmania also eased from 76pc to 65pc. This confirms that the supply story has become more concentrated. NSW and Queensland is carrying a larger share of cattle flow, while southern and western regions have tightened materially.

Processing activity in April fell sharply across all states. New South Wales dropped from 89pc to 37pc and Queensland from 80pc to 45pc. Tasmania declined from 78pc to 46pc and Victoria from 71pc to 50pc. South Australia eased from 75pc to 60pc, while Western Australia slipped from 76pc to 67pc.

The scale and consistency of these declines point strongly to a calendar driven effect. Shortened operating weeks associated with Easter have reduced kill days across the country, pulling down throughput figures. However, the supply side signals suggest that the underlying market has not tightened. Queensland yardings have continued to lift, and New South Wales remains at historically high levels. This indicates that cattle availability has not materially contracted despite the drop in processing.

The price data provides the clearest indication of what is occurring beneath the surface. Over the past four weeks, processor cow prices have fallen by 19 cents. Heavy steer prices have also declined, falling just 3 cents over the same period. While not as extreme as cows, this points to improving availability of finished cattle.

This broad based decline highlights a second layer to the market shift and it is not only supply increasing, but demand stepping back. Restocker demand has weakened significantly, suggesting producers are becoming more cautious. Seasonal uncertainty and rising input costs are likely contributing to reduced appetite for younger cattle.

Feedlot demand has held firm snd remains more resilient than restocker demand, as reflected in the relative performance of feeder steers. The data shows a market loosening rapidly from the bottom up. Cows have led the decline, followed by younger cattle, with finished stock also moving lower. This sequence aligns with the earlier lift in slaughter.

Processors were able to increase throughput on the back of higher cow turnoff, which has now flowed through into lower prices across the board. External factors continue to shape the market environment. Logistical challenges and trade constraints are influencing both cattle movement and processor behaviour. At the same time, export market conditions have softened, limiting the ability of processors to maintain higher grid prices. The balance of power has shifted with processors no longer chasing cattle as aggressively.

Instead, increased availability has allowed them to push prices lower to manage intake and protect margins. The April processing data, while distorted by Easter, does not alter this underlying trend. It reflects a temporary reduction in operating days rather than a structural change in demand. As full operating weeks return, the focus will shift back to how much cattle continues to come forward.