Global cattle pricing update April 2026

Get short video updates on your phone

For quicker updates as markets move, follow @themeatwatcher on Instagram. I regularly post short summaries and charts breaking down what’s happening in meat proteins and broader ag markets so you can stay across the key moves without having to read through pages of analysis. If markets are moving quickly, that’s usually where the updates will land first.

Global cattle price update - April 2026

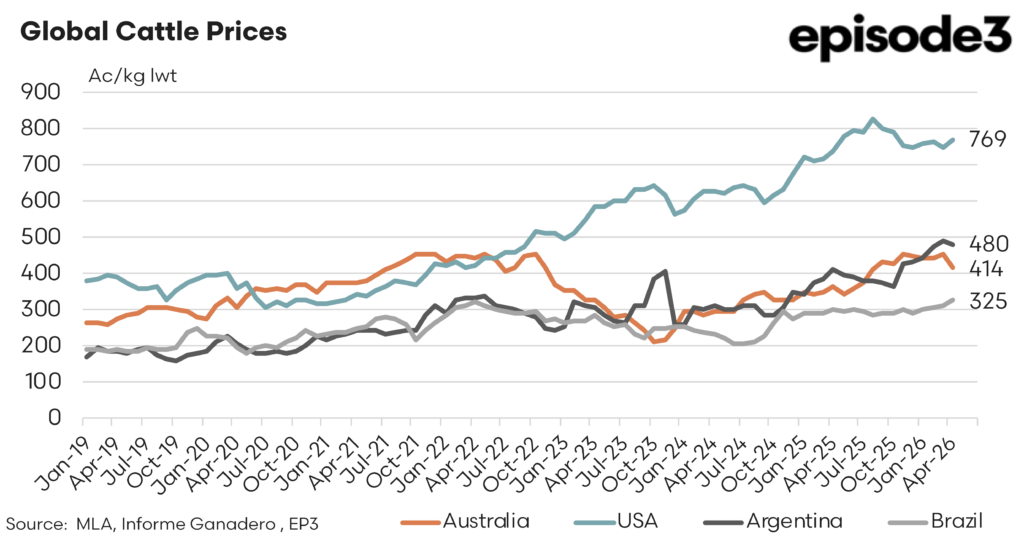

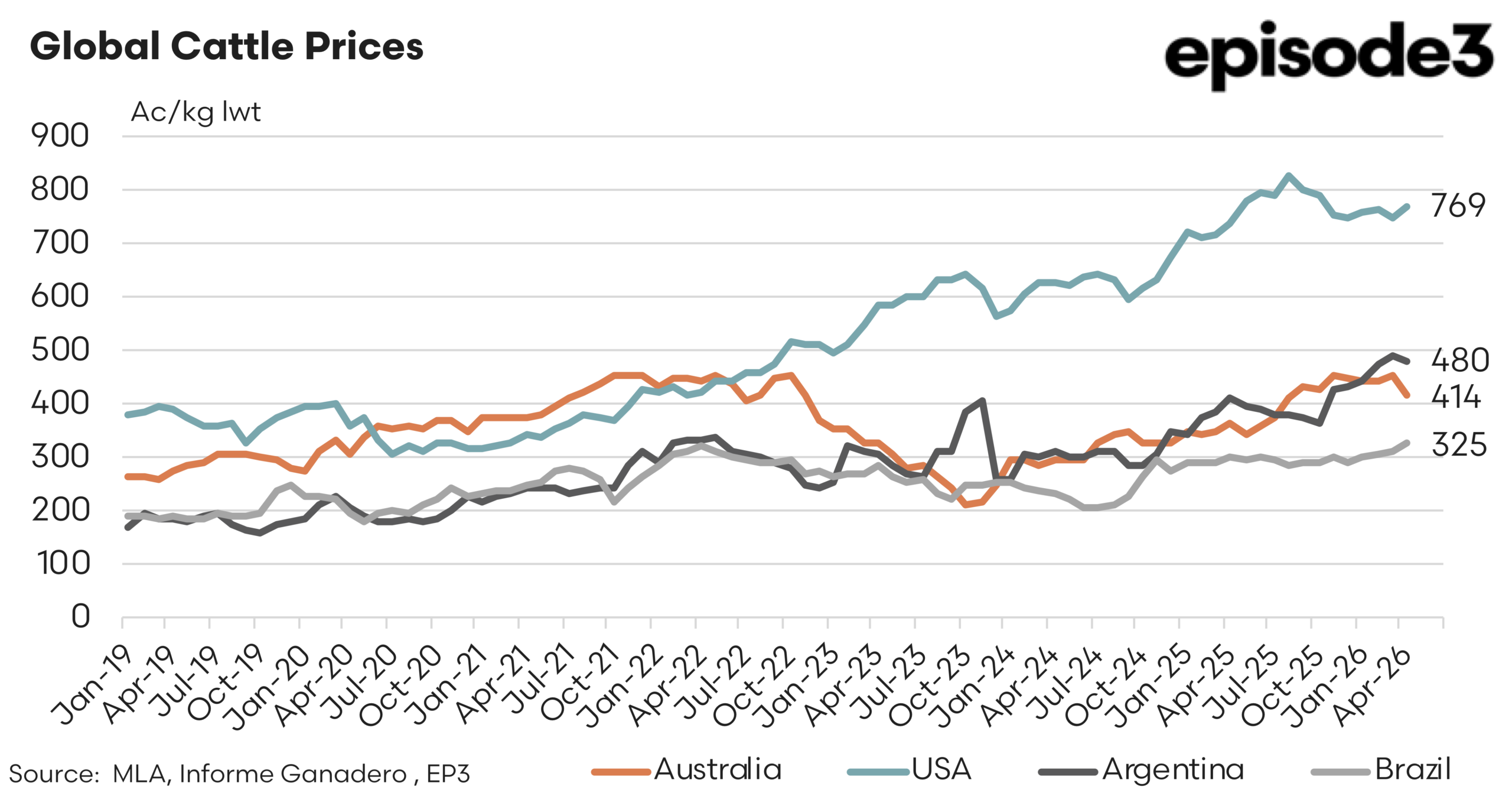

The latest update to EP3 global cattle price comparison shows the US remains well ahead of the pack, while Argentina has continued to strengthen and Brazil has also edged higher. Australia, by contrast, has softened from the start of the year, leaving local heavy steer prices further behind the US and Argentina, but still above Brazil.

The comparison is shown in Australian cents per kilogram live weight, which allows the major producing nations to be assessed on a broadly comparable basis. As of mid-April 2026, US heavy steer prices were sitting near 769Ac/kg lwt.

Argentina was around 480Ac/kg lwt and Australia was at 414Ac/kg lwt. Brazil was the lowest of the group at 325Ac/kg lwt. The headline change since the start of 2026 is that Australian prices have eased by 7pc. That is not a collapse, but it does mark a change in momentum after the recovery seen through much of 2025.

During the same period, US prices have edged higher by 2pc. Argentina and Brazil have both lifted by 9pc. This means Australia has not only lost some outright price ground, it has also slipped relative to its main competitors. At 769Ac/kg lwt, Australian finished cattle are trading 46pc below their US equivalents.

That price gap remains a major feature of the global beef market. The US is still dealing with the consequences of a heavily depleted cattle herd, following strong liquidation in earlier years. Tight cattle availability continues to underpin domestic US cattle prices, even as beef demand is being tested by high retail prices.

For Australian exporters, the high US cattle price environment is useful. It supports the value of beef internationally, particularly into high value grainfed and chilled beef markets. It also keeps US beef expensive relative to Australian product. That is helpful for Australian competitiveness in markets such as Japan, South Korea and China.

Argentina is the other market to watch closely. At 480Ac/kg lwt, Argentine heavy steer prices are now 14pc above Australian prices. The lift in Argentine cattle values since the start of the year has pushed it further above Australia. This matters because Argentina is a large beef producer with a strong export culture and a long history of supplying global beef markets when policy settings allow. Australia still has advantages in market access, product consistency, traceability and brand positioning. The narrowing or widening of price gaps against Argentina remains important when assessing global competitiveness, particularly into China.

Brazil continues to sit at the bottom of the comparison. At 325Ac/kg lwt for the Brazilian heavy steer, Australian prices are 27pc above Brazilian cattle . Brazil’s price advantage reflects its scale, large cattle herd, lower cost production base, cattle type and currency position. Even with a 9pc lift since the start of 2026, Brazil remains the cheapest major cattle market in the comparison. That low cost base continues to give Brazil a strong competitive position into more price sensitive markets. It also means Brazil remains a key benchmark for Australian beef, particularly in China and other destinations where price can be a major driver of trade flows.

For Australia, the picture is mixed rather than negative. The 7pc easing in local heavy steer values since the start of the year has reduced producer returns from the levels seen late in 2025 and early 2026. However, Australian cattle are still priced well below the US and Argentina. That supports export competitiveness against those two markets.

At the same time, Australia remains well above Brazil, which means there is still a limit to how aggressively Australian beef can compete on price alone. Australia is a premium, reliable supplier sitting below the extreme pricing pressure of the US, but above the low cost production base of Brazil. Thankfully in most of the major export markets Australia competes more directly with the US and Argentina than Brazil. Even into China, where Brazil is the largest beef importer Australia targets a different market segment that are more aligned to the market segments targeted by the US and Argentina.