Tight supply trumps soft sheep meat export demand

Market Morsel

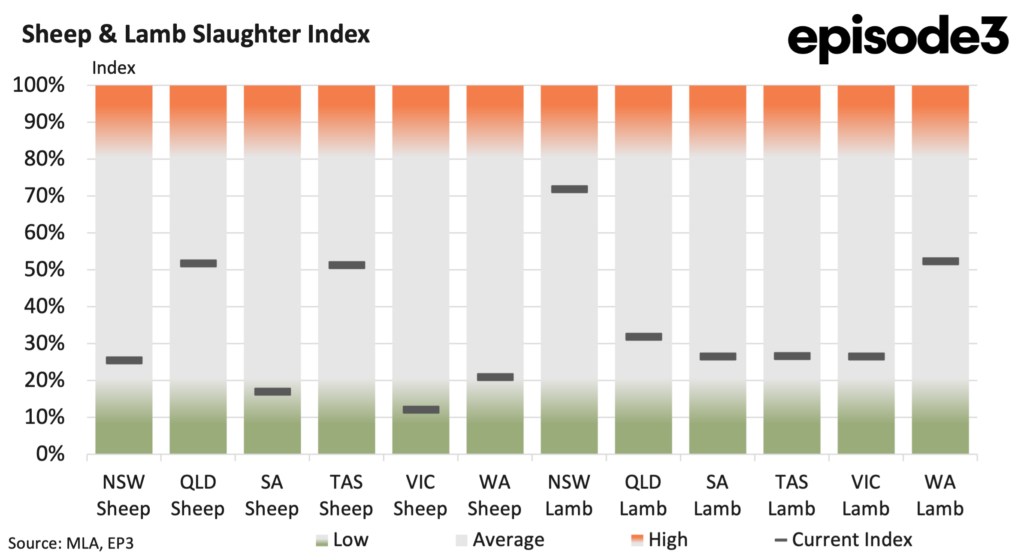

The latest Sheep and Lamb Slaughter Index data shows a modest improvement in throughput during May, but the broader picture remains one of relatively tight supply conditions across much of Australia. While slaughter levels increased in several states compared to April, the gains were generally recorded from a very low base, suggesting the market remains supply constrained despite the recent uptick in processor activity.

For sheep, slaughter increased across most regions during May. New South Wales lifted from 22 percent in April to 25pc in May, while South Australia improved from 15pc to 17pc. Tasmania rose from 47pc to 51pc and Western Australia increased from 13pc to 21pc. Victoria also improved modestly, moving from 10pc to 12pc. Queensland was the only state to ease slightly, slipping from 53pc to 52pc.

Although these movements indicate processors were able to source more sheep during May, the actual index levels remain relatively low across most regions. Victoria, South Australia, New South Wales and Western Australia all remain well below average historical slaughter levels, highlighting that sheep availability is still constrained despite the month-on-month improvement.

The lamb slaughter story was somewhat different. New South Wales recorded the most significant change, with lamb slaughter jumping from 51pc in April to 72pc in May. Queensland also improved from 17pc to 32pc, while South Australia edged higher from 25pc to 26pc and Victoria lifted from 24pc to 26pc. Against this, Tasmania fell sharply from 45pc to 27pc and Western Australia eased from 64pc to 52pc.

The standout feature of the lamb data is the strength in New South Wales. Unlike most of the other states where slaughter remains in the low to average range, New South Wales lamb throughput has moved into the upper end of historical levels. This suggests processors were able to access significantly more lambs during May than they had during April.

At first glance, the increase in slaughter would normally suggest that supply conditions are becoming easier and that prices should come under pressure. However, the pricing data over the same period tells a very different story.

Heavy lamb prices lifted by around 61c over the past four weeks. Trade lamb increased by approximately 80c, while light lamb gained around 78c and Merino lamb rose by close to 120c. Restocker lamb values also strengthened by roughly 81c. Perhaps most notably, mutton prices climbed by around 61c over the same period.

Ordinarily, rising slaughter and rising prices occurring simultaneously would imply stronger demand. However, the broader market data suggests that this may not be the case. The recent Sheep and Lamb Yarding Index data pointed towards tighter saleyard conditions across much of the eastern mainland during May.

Lamb yardings declined in New South Wales, Queensland, South Australia, Victoria and Tasmania, with only Western Australia recording a significant increase. The yarding data therefore suggests that fewer animals were being offered through traditional saleyard channels, particularly across the eastern states. This may help explain why prices strengthened despite higher slaughter levels. Processors appear to have been competing harder for available stock, even though overall market supply remained relatively constrained. The increase in slaughter may therefore reflect improved procurement success rather than a genuine surge in livestock availability.

In other words, processors managed to secure more stock during May, but they had to pay more to do so. Export performance provides another important piece of the puzzle. Australian sheep meat exports during May remained relatively subdued. Total exports were 31pc below the same month last year and 18pc below the five year average.

This is important because it challenges the idea that stronger export demand was responsible for the price rally. Instead, the export data points towards a market where supply remains the dominant influence. Processors continue to face relatively tight livestock availability despite recent improvements in slaughter levels.

At the same time, export volumes remain constrained and are not providing the type of demand growth that would normally accompany a widespread rise in prices. The result is a market that appears to be balancing on limited supply rather than expanding demand. The May slaughter data demonstrates that processors were able to increase throughput in several regions, particularly for lambs in New South Wales.

However, the broader supply picture remains tight, especially for sheep. The accompanying yarding and export data suggest that the recent price gains are less about booming demand and more about competition for a relatively limited pool of available livestock. The latest figures point to a sheep meat sector where supply remains constrained despite modest improvements in slaughter levels. Prices have strengthened because processors continue to compete for stock, not because export markets are experiencing exceptional growth.