Small gains reversed for sheep meat processors

Sheep Processor Trading Conditions Model

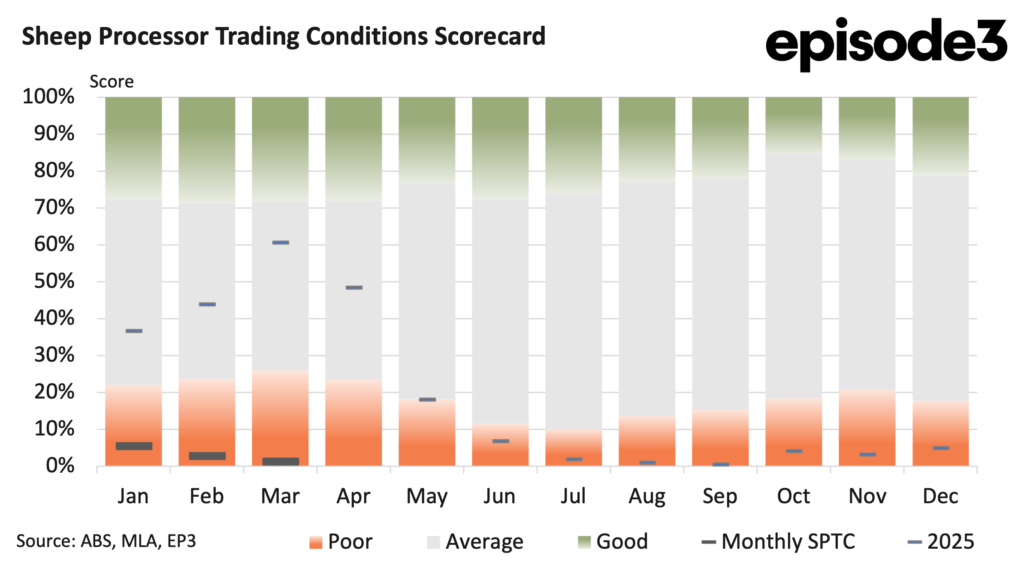

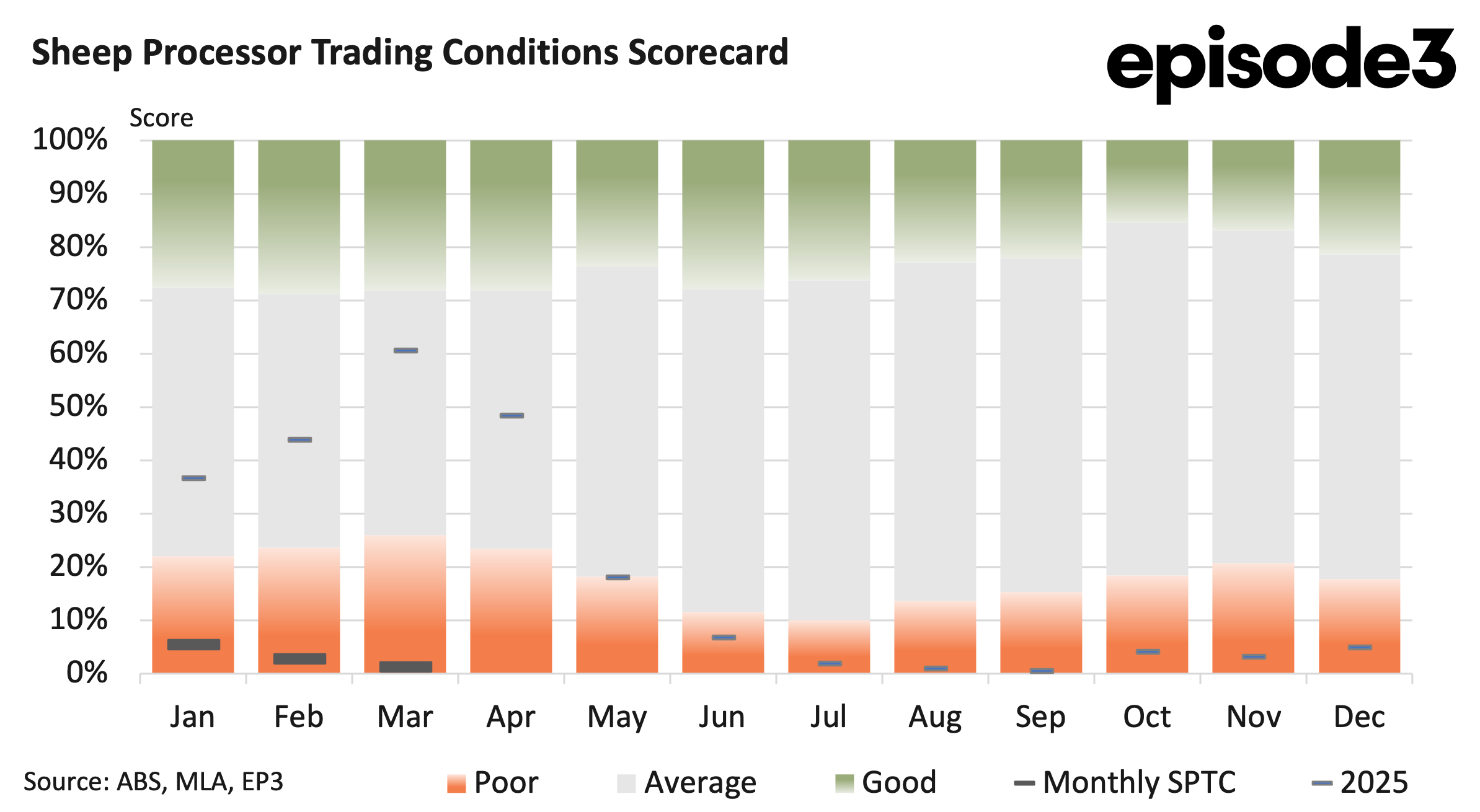

The latest revision to the Sheep Processor Trading Conditions index paints a more challenging picture for processors than previously reported, with updated export values revealing that margins have continued to deteriorate through the first quarter of 2026 rather than improve.

Following adjustments to export pricing data sourced from the Department of Agriculture, Fisheries and Forestry, the February SPTC result has been revised lower, changing the narrative around processor performance during the opening months of the year. Rather than lifting from January levels, the revised data shows the SPTC falling from 5.4pc in January to 2.7pc in February. Conditions deteriorated further in March, with the index slipping to just 1.3pc. That result marks the weakest monthly trading conditions recorded since September 2025 and reinforces the significant pressure currently facing the processing sector.

The decline also means the annual average SPTC for the first quarter of 2026 sits at just 3pc. This compares with an annual average of 47pc at the end of the first quarter in 2025, highlighting the dramatic shift in processor profitability over the past twelve months. The contrast between the two periods demonstrates just how rapidly the margin environment has deteriorated as livestock prices have continued to rise.

The March result is particularly noteworthy because it occurred despite generally stronger revenue outcomes across several key export destinations. Export returns improved across all of the major markets included in the index during March. Average export values into China increased by 3.7pc compared to February.

The United States recorded an even stronger gain, rising by 7.3pc over the month. Malaysia improved by 3pc, while the United Arab Emirates posted the largest increase, lifting by 13.1pc. The sharp rise in UAE values appears to reflect tightening regional sheepmeat availability associated with disruptions to trade flows from Iran, which has traditionally been a significant supplier into Middle Eastern markets.

Ordinarily, a broad-based increase in export values would be expected to support processor margins. However, the gains in export revenue were more than offset by rising livestock procurement costs and higher operating expenses.

Livestock prices continued to move higher during March, further increasing the cost of processing stock. Heavy lamb prices lifted by 2.9pc over the month. Light lamb values rose by 2.4pc. Trade lamb prices increased by 4pc, while mutton prices climbed by 3pc. These increases add to what has already been a period of substantial livestock price inflation over the past year.

For processors, livestock procurement remains by far the largest cost component in the production chain. Even relatively modest monthly increases can therefore have a significant impact on overall profitability. The challenge facing processors is that livestock prices are rising from an already elevated base. As a result, improvements in export values need to be substantial simply to maintain margins, let alone improve them.

March also delivered higher returns from the domestic market. Retail lamb prices increased by 1.4pc during the month, providing some additional support to processor revenues. However, as with export values, the increase in retail pricing was insufficient to offset the rise in livestock costs.

Adding further pressure were increases in a range of operating expenses. Transport costs moved higher during March as fuel related expenses continued to influence freight rates. Energy costs also increased, adding to processing overheads. Labour expenses continued their upward trend as wage costs rose across the sector. Individually, these increases may appear relatively modest.

Collectively, however, they compound the margin pressure already being created by expensive livestock. The result is that processors are facing a situation where costs are rising across multiple parts of the business simultaneously. While revenue streams have improved, the pace of revenue growth has not matched the rate of cost escalation.This explains why processor margins continued to deteriorate despite stronger export and domestic pricing.

The March outcome highlights the difficult balancing act currently facing the sheep meat processing sector. Livestock supply remains relatively constrained, helping to underpin strong sheep and lamb prices. That is positive for producers but creates ongoing challenges for processors attempting to maintain profitability. At the same time, export demand remains supportive enough to sustain higher prices, but not strong enough to fully compensate processors for the increased cost of securing stock.

The revised February figures and weaker March result also serve as a reminder of how sensitive processor margins are to changes in export values. Despite stronger export returns, firmer domestic retail pricing and generally supportive market conditions, the relentless increase in livestock procurement costs and higher operating expenses have continued to erode margins during 2026.