Groundhog Day for Grain Markets

The Snapshot

- Grain markets continue to ignore mounting weather and geopolitical risks as comfortable global inventories dominate sentiment.

- A developing El Niño, European heatwaves and excessive US rainfall have failed to spark a meaningful rally in wheat, corn or soybeans.

- Black Sea exporters remain the world’s key price setters, with strong Russian and regional production keeping export competition intense.

- Major importers, including Egypt and Turkey, are reducing reliance on imported wheat thanks to improved domestic production.

- While grain prices remain under pressure, Australian growers are benefiting from sharply lower input costs, with urea down 28pc and diesel down 20pc over the past month.

The Detail

If grain traders are experiencing a sense of déjà vu, they are not alone. Another week delivered a fresh list of potentially bullish developments, from heatwaves in Europe and flooding concerns in the United States to an emerging Super El Niño and renewed escalation in the Russia-Ukraine conflict. Yet grain markets continue to behave as though none of it really matters.

The latest weather forecasts certainly contain enough reasons for concern. Parts of the US Midwest remain excessively wet, with Illinois forecast to receive another soaking at a time when only around one-fifth of the state’s winter wheat crop has been harvested. Across Europe, temperatures are forecast to push well above normal, with some regions of France expected to approach 40°C. French wheat conditions slipped from 77pc to 76pc good-to-excellent during the week, while maize ratings also deteriorated.

Adding to the weather story is the declaration of an El Niño. Historically, such events have been associated with droughts across Australia and parts of Asia, flooding through the Americas and significant volatility in global agricultural markets.

These developments should be enough to spark a meaningful rally. Instead, the market response is muted.

The reason is simple: the global grain pantry is well stocked. World wheat stocks are forecast to sit at their highest level in five years, while global corn inventories are expected to reach a three-year high. Rice stockpiles are sitting at record levels. Importers know grain is available and are showing little urgency in securing supply.

Egypt, one of the world’s largest wheat buyers, recently reported wheat imports falling from 13.2 million tonnes to 12.5 million tonnes as domestic production increased and government procurement reached record levels. Turkey is also expected to rely less on imports following an improved local harvest. When major importers become less active, exporters inevitably find themselves competing harder for available demand.

Russian wheat, the global benchmark, continues to set the tone for international pricing. Large crops in Russia, Ukraine and Romania are keeping export competition intense. Algeria’s recent purchase of more than 800,000 tonnes of milling wheat is expected to be sourced largely from the Black Sea, reinforcing the region’s importance.

At the same time, geopolitical risks can’t be ignored. Ukraine’s increasingly aggressive strikes inside Russia, including attacks on energy infrastructure, have raised concerns about potential retaliation against Ukrainian export facilities. Despite these risks, grain continues to flow from the Black Sea, and markets appear increasingly desensitised to developments in the region. For now, traders seem reluctant to price in disruptions that have not yet occurred.

Closer to home, the Australian production outlook is broadly favourable. Rainfall across parts of Western Australia over recent weeks has improved crop prospects following a dry May, while eastern Australia continues to receive useful moisture. Although a developing El Niño remains a risk later in the season, current crop conditions across much of the country remain relatively positive.

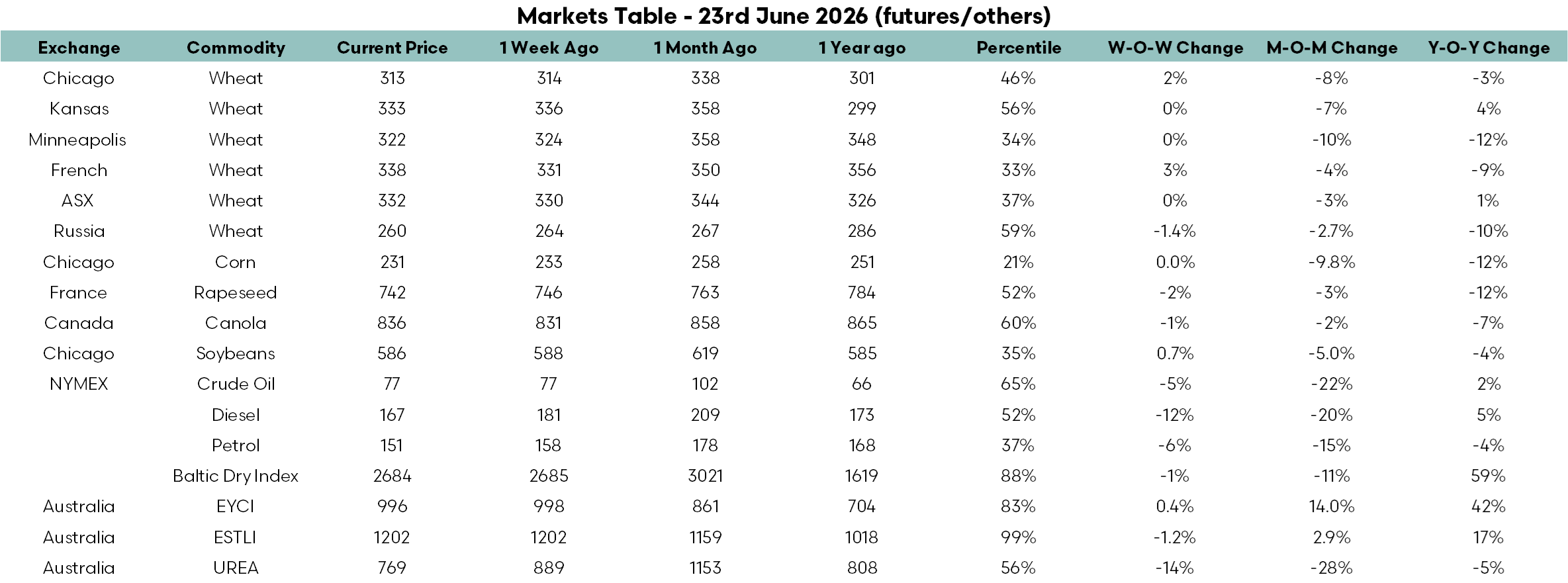

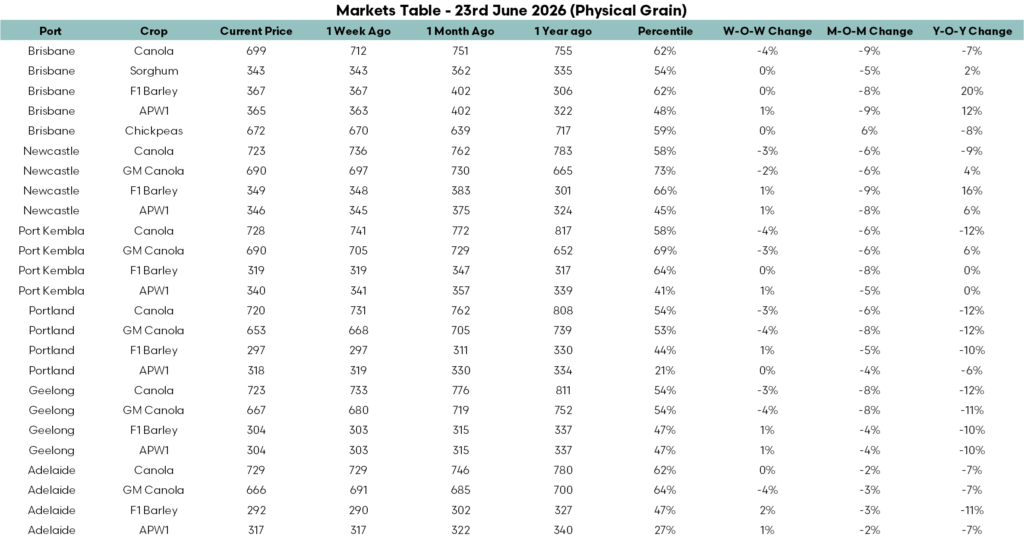

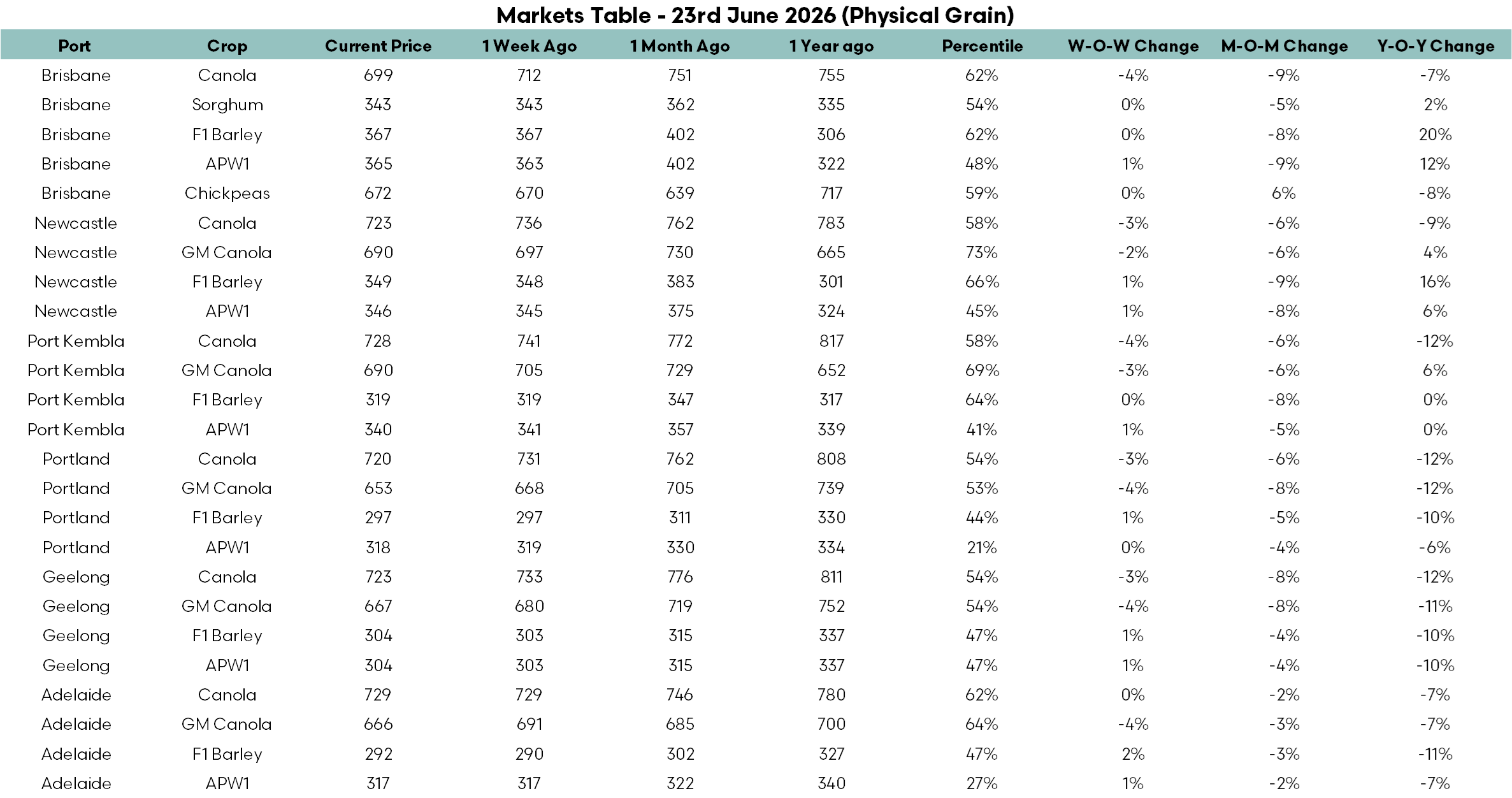

The accompanying market table reflects the broader mood. Australian wheat prices were generally steady to slightly firmer during the week but remain well below levels seen a month ago. Brisbane APW1 is down 9pc over the month, while Newcastle APW1 has fallen 8pc. However, wheat values remain broadly in line with, or above, year-ago levels across much of eastern Australia. Canola has been under greater pressure, declining by 6pc to 9pc over the past month and sitting 7pc to 12pc below year-ago levels across most ports as weaker crude oil prices weigh on the oilseed complex.

The more notable movement is occurring in costs. Diesel prices are down 20pc over the month, while the EP3 Urea Import Model has fallen a remarkable 28pc over the same period and 14pc in the past week alone. Urea is now sitting below year-ago levels for the first time since the Middle East conflict erupted. This is undoubtedly good news, although for many growers a significant portion of this season’s fertiliser requirements were purchased when prices were substantially higher. The benefit will be felt most by those still to buy, or as lower replacement costs gradually work their way through the supply chain.