Stock gets harder to find as yarding levels slide

Market Morsel

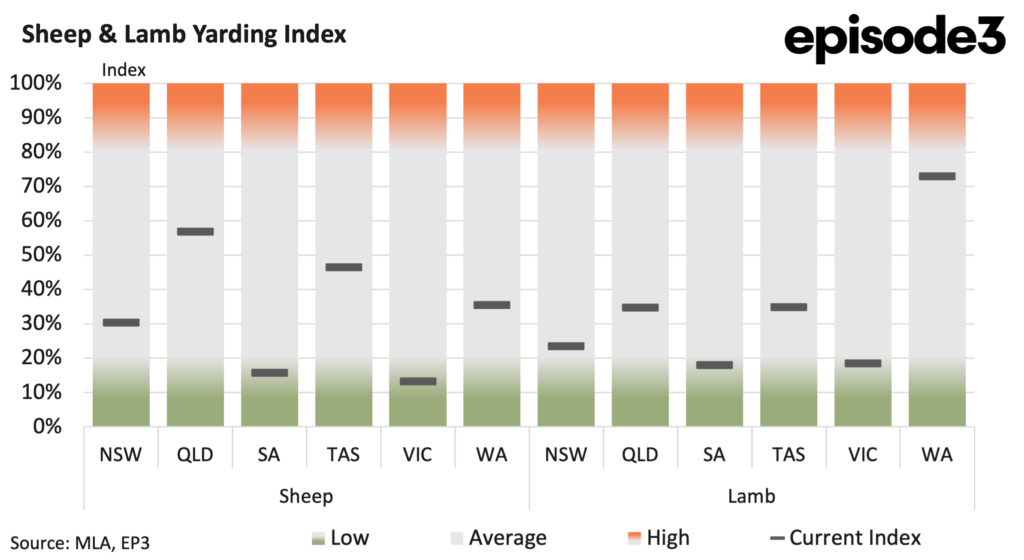

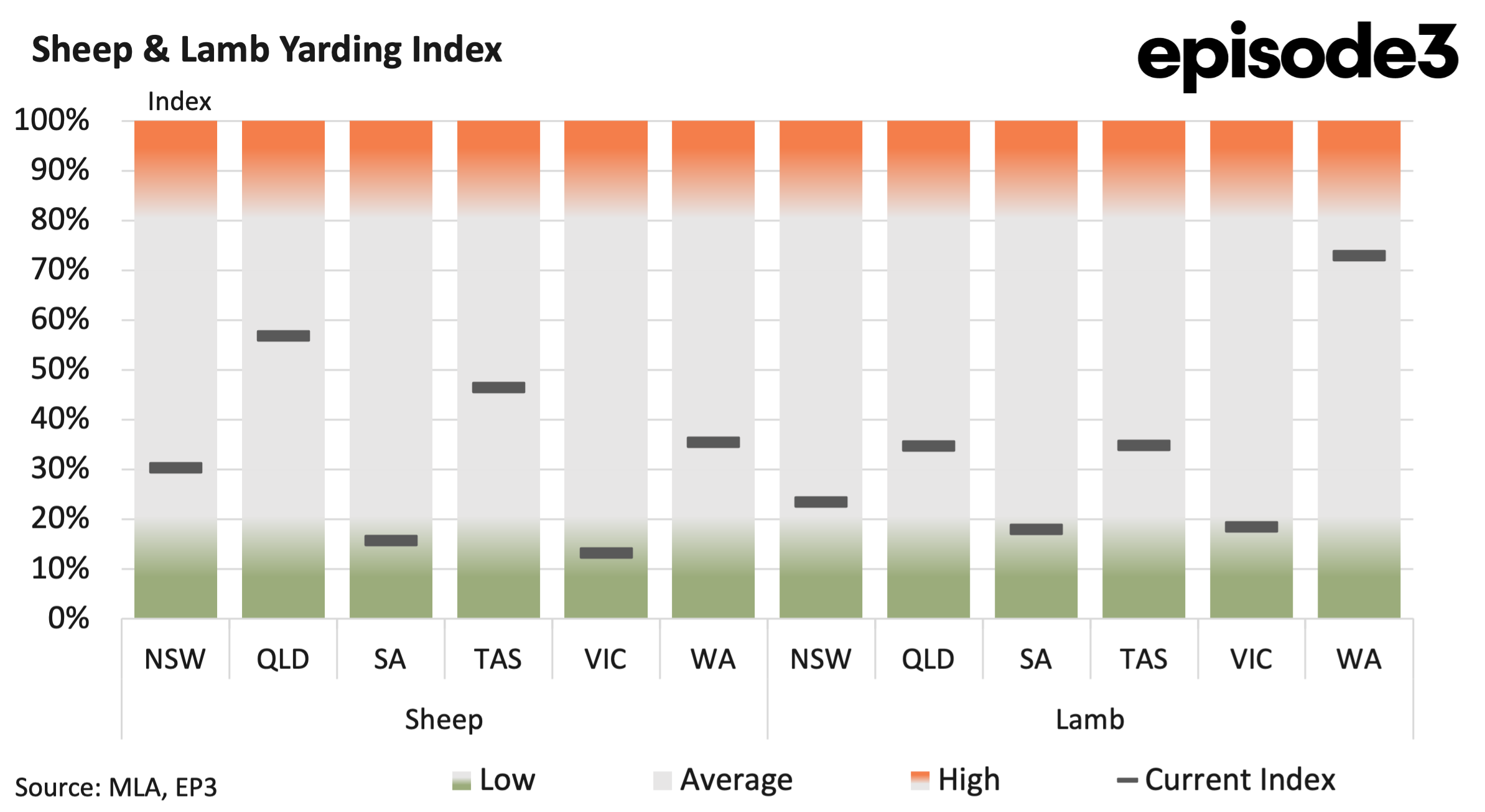

The latest Sheep and Lamb Yarding Index data shows that supply tightened noticeably during June, with sheep and lamb offerings declining across almost every major producing state. The broad-based reduction in throughput suggests that the modest supply improvement evident during May has largely run its course, leaving the market once again reliant on a relatively limited pool of available stock. Unlike previous months where regional trends often differed significantly, the June data shows a much more consistent pattern across the country.

For sheep, yardings declined in five of the six reporting states. New South Wales sheep yardings fell from 54pc in May to 30pc in June, indicating a substantial reduction in producer selling activity. Queensland eased from 78pc to 57pc and while it is a minor contributor to supply it followed the broader trend for winter tightening to recording a significant decline in throughput.

South Australia slipped from 28pc to 16pc, reinforcing the ongoing tightness that has characterised the state’s sheep market for much of the year. Tasmania also weakened, falling from 62pc to 46pc, while Western Australia declined from 60pc to 35pc. Victoria was the only state to record a modest increase, lifting from 10pc to 13pc.

However, even after this improvement, Victorian sheep yardings remain among the lowest in the country and continue to signal exceptionally constrained supply conditions. The sheep data suggests that the additional stock brought forward during May has largely been exhausted.

Queensland and Western Australia had previously provided a degree of support to national supply, but both states recorded substantial declines during June. This means the tightening is no longer confined to the southern mainland and is becoming more evident across the country.

The lamb market followed a similar pattern. New South Wales lamb yardings fell from 38pc in May to 23pc in June, indicating a significant reduction in available stock after the stronger throughput seen earlier in the season. Queensland declined from 51pc to 35pc, while South Australia eased from 25pc to 18pc.

Tasmania also weakened, slipping from 40pc to 35pc. Western Australia remained the strongest lamb supply region in the country, but even in the west throughput eased from 81pc to 73pc. Victoria followed the tighter trend too with a slip from 24% to 18% during June.

The June yarding data points to a market where livestock availability is becoming increasingly constrained. The widespread nature of the decline suggests that the reduction is not simply the result of regional seasonal factors but rather reflects a broader tightening in sheep and lamb supply.

The price data recorded over the same period provides further insight into how the market is responding. Mutton prices delivered one of the strongest performances, increasing by around 80c over the past four weeks to sit near 908c per kilogram carcase weight. This rise aligns closely with the decline in sheep yardings and reflects the increasingly limited availability of mature stock. With fewer sheep being offered across most states, processors have been forced to compete more aggressively to secure throughput.

Restocker lambs also recorded a strong gain, lifting by approximately 47c over the month. The strength in restocker values suggests confidence among producers that supply conditions are likely to remain relatively tight through winter.

Heavy lamb and trade lamb prices also moved higher, increasing by around 22c and 37c respectively. While these gains were more modest than those recorded for mutton and restocker lambs, they nevertheless indicate that the market remains supported despite softer export conditions. Importantly, the recent price gains have occurred despite sheep meat export performance remaining relatively subdued.

Export volumes during May were well below year ago levels, with shipments to China continuing to track lower and many Middle Eastern destinations remaining weaker than historical averages. If export demand was booming, the rise in prices would be relatively easy to explain. However, the export data suggests the opposite. This means the current market strength is being driven primarily by supply rather than demand.

Processors still require livestock to maintain production schedules, yet fewer sheep and lambs are being offered through saleyards. As a result, buyers are being forced to pay more to secure available stock, even though end market demand has not improved dramatically.

The contrast between the yarding and export data is important. The export market is providing support, but it is not providing exceptional growth. Instead, the dominant factor influencing prices appears to be tightening livestock availability.