Sheepmeat export update May 2026

May 2026 - Sheep Meat Export Update

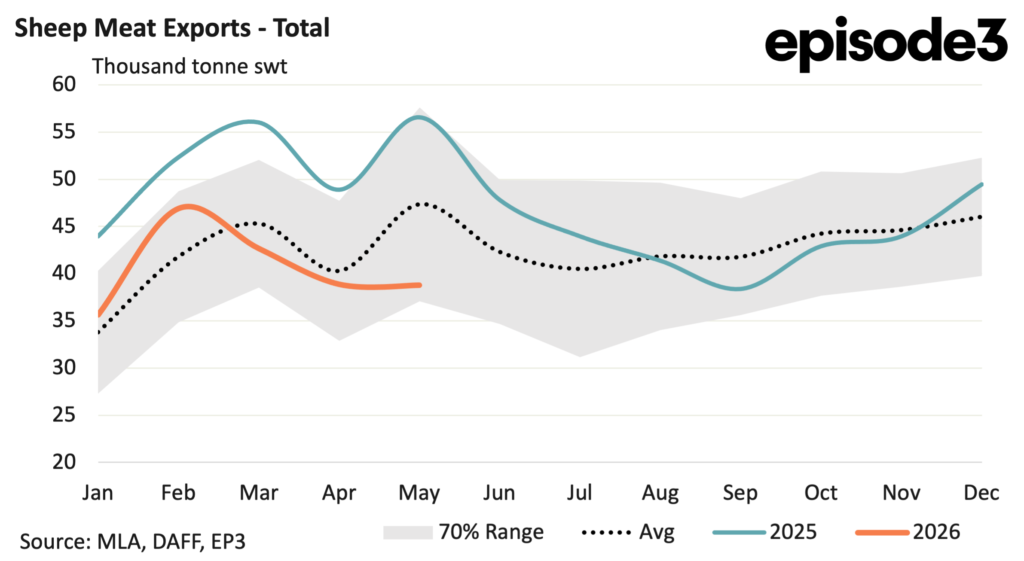

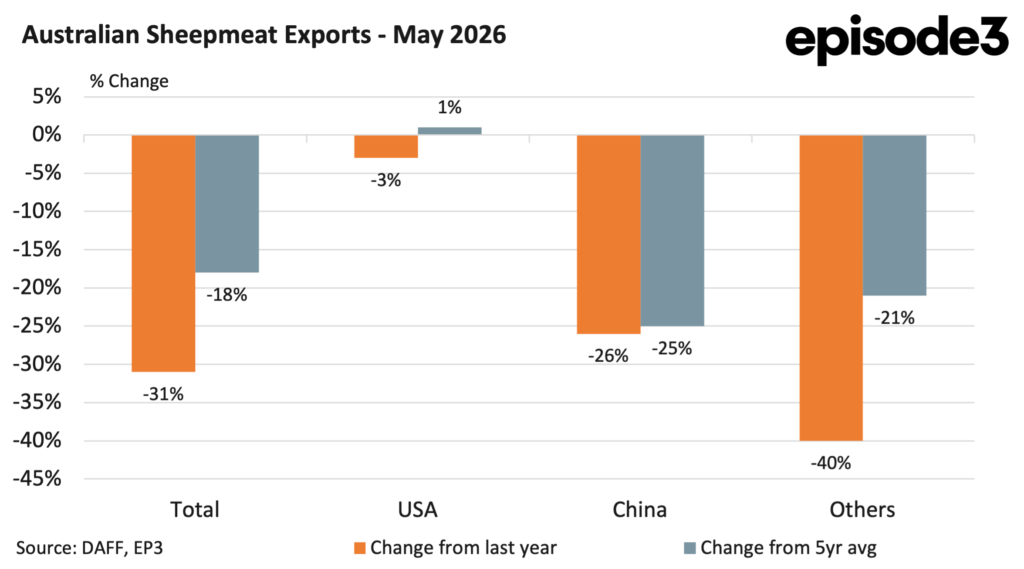

Australian sheep meat exports remained under pressure during May 2026, with total shipments reaching 38,767 tonnes. While export volumes were largely unchanged from April, they remained 31pc below May last year and 18pc below the five-year average for the month.

The result continues a trend that has emerged through much of 2026, with sheep meat exports tracking below both last year’s elevated levels and historical averages despite generally strong global demand and record livestock prices.

Unlike the beef sector, where exports continue to push to record highs, sheep meat exports are facing a combination of tighter domestic supply, elevated livestock costs and softer demand from several traditionally important destinations.

China remained Australia’s largest sheep meat customer during May, taking 8,585 tonnes. Despite retaining the number one position, shipments to China were 26pc below the same month last year and 25pc below the five-year average.

The decline reflects a broader moderation in Chinese sheep meat imports following several years of exceptionally strong buying. China remains Australia’s largest sheep meat destination, but the market is no longer providing the same level of growth support seen earlier in the decade.

The United States was Australia’s second-largest market during May, receiving 7,944 tonnes. Exports to the US were only 3pc below last year and sat 1pc above the five-year average, making it one of the few major destinations to maintain relatively stable demand.

The resilience of the US market continues to stand out. While volumes are not growing at the pace seen in beef, the American market has become an increasingly important outlet for Australian lamb and continues to absorb close to one-fifth of total sheep meat exports.

Outside China and the US, conditions were considerably more challenging.

The “other markets” category accounted for 22,238 tonnes and the trade volumes into these destinations were 40pc lower than last year and 21pc below the five-year average, highlighting the broader weakness evident across several key export regions.

A significant portion of that weakness continues to come from the Middle East and North Africa region.

Lamb exports into several traditional Gulf markets remained well below normal seasonal levels during May. Shipments to the United Arab Emirates were 30pc below the five-year average, while exports to Jordan were 35pc lower. Qatar remained particularly weak, with lamb exports sitting 57pc below average levels, while flows into Bahrain were almost non-existent at 97pc below the five-year average.

The weakness in lamb demand across much of the region continues a pattern that first became evident earlier in the year. While some destinations have shown signs of stabilisation, volumes remain substantially below historical norms.

Mutton trade presented a more mixed picture.

Exports to Kuwait were marginally stronger than normal seasonal levels, sitting 2pc above the five-year average. However, several other key destinations remained softer. Mutton exports to Oman were 47pc below average levels, while shipments to Saudi Arabia were 15pc below average and exports to the UAE were 4pc lower.

The contrasting performance between lamb and mutton highlights the differing market dynamics across the region, although overall demand remains weaker than historical standards.

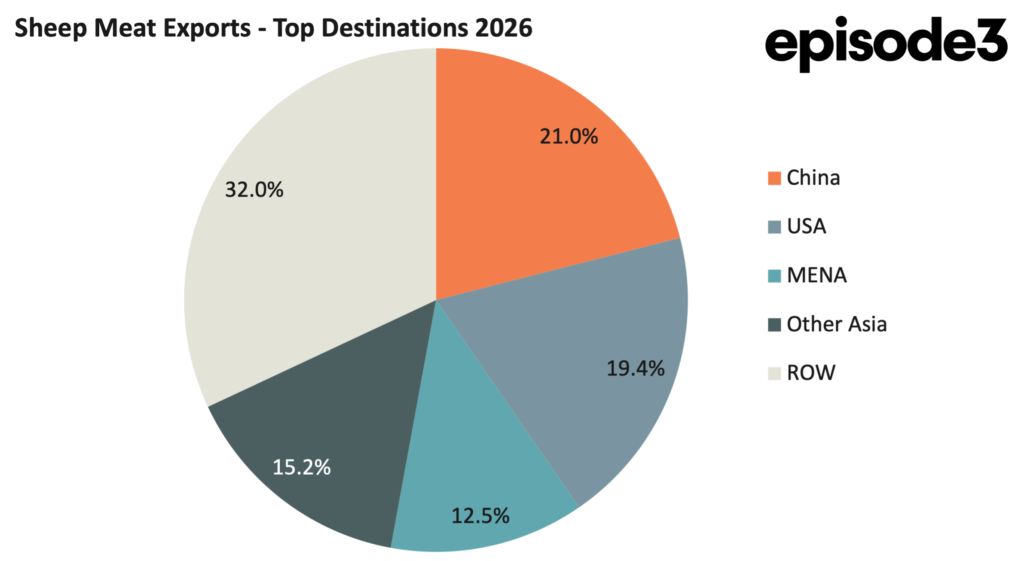

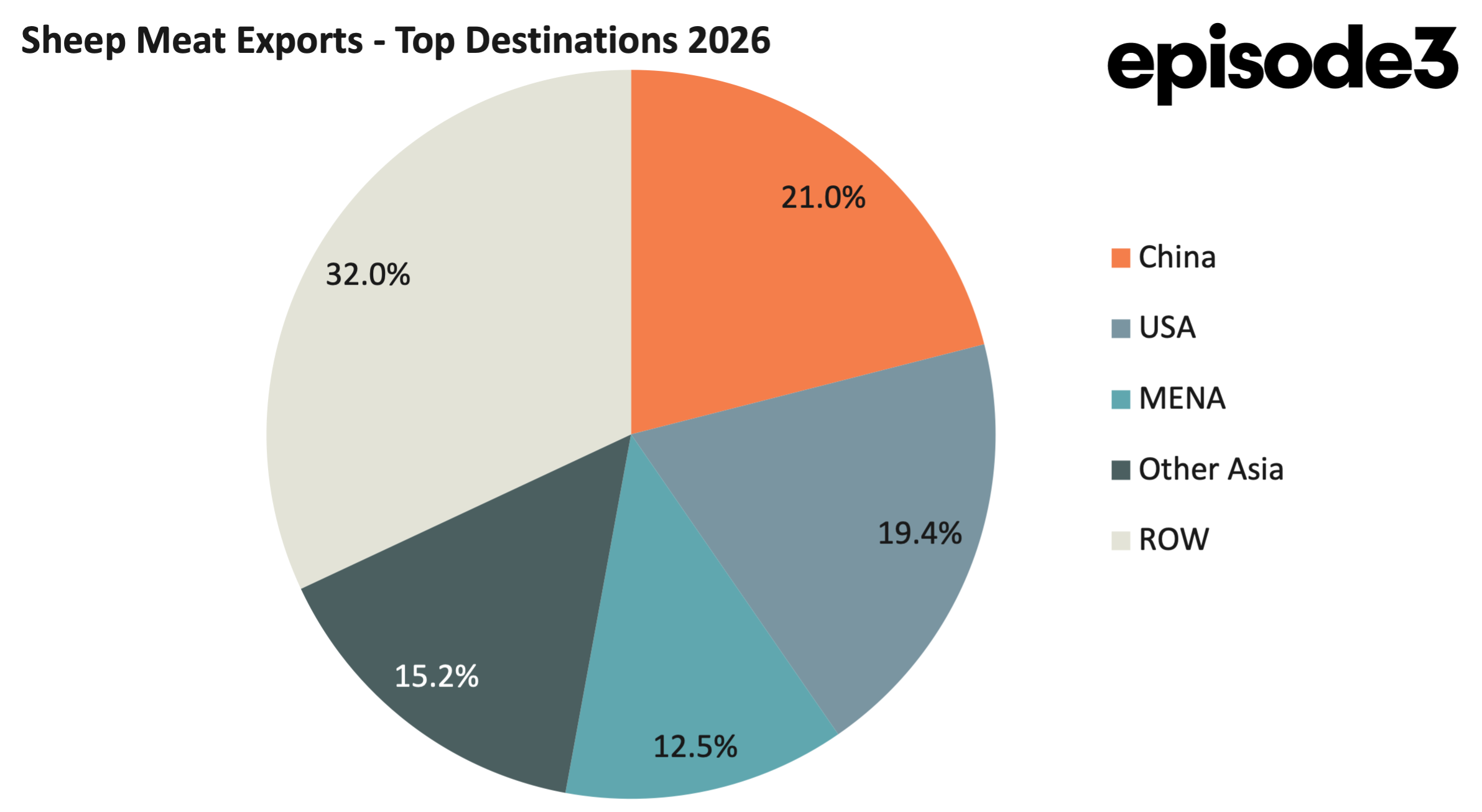

Looking at the broader distribution of exports so far in 2026, the sheep meat trade remains relatively diversified despite recent challenges. China accounts for around 21pc of exports, the US 19pc, MENA markets 13pc and other Asian destinations 15pc, with the remainder spread across a range of global markets.

That diversification has helped soften the impact of weaker demand in individual destinations. However, unlike the beef sector where multiple markets are simultaneously expanding, sheep meat exports are currently relying on only a handful of destinations to maintain volume.

The May result also highlights the contrast between strong livestock prices and export performance. Australian lamb and mutton prices remain historically elevated, yet export volumes continue to track below average levels. That combination suggests the industry is being constrained more by supply availability than demand.

As the industry moves into the second half of 2026, attention will remain focused on whether Middle Eastern demand begins to recover and whether China stabilises at current import levels. Until then, sheep meat exports appear likely to remain below the record pace achieved during recent years, even as global demand for Australian product remains broadly supportive.