Why Grain Traders Keep Ignoring the Warning Signs

The Snapshot

- Speculative funds continue to increase bearish grain positions despite mounting weather and geopolitical risks across key producing regions.

- Russia’s forecast 91 million tonne wheat crop and comfortable global inventories continue to outweigh production concerns elsewhere.

- Europe’s heatwave and India’s delayed monsoon are shifting weather risk from wheat towards corn and oilseed crops.

- Australian crop prospects continue to improve following widespread rainfall, supporting the outlook for another solid winter crop.

- Grain prices remain subdued, but lower fuel and fertiliser costs are providing welcome relief to Australian growers’ cost of production.

The Detail

The grain market is becoming increasingly one-sided. Traders have spent weeks selling wheat and corn on the assumption that another large global harvest is inevitable. Yet almost every day seems to deliver another potential threat, from European heatwaves and delayed Indian monsoons to geopolitical tensions and historically poor US winter wheat conditions. The question is no longer whether risks exist, but whether the market is paying enough attention to them.

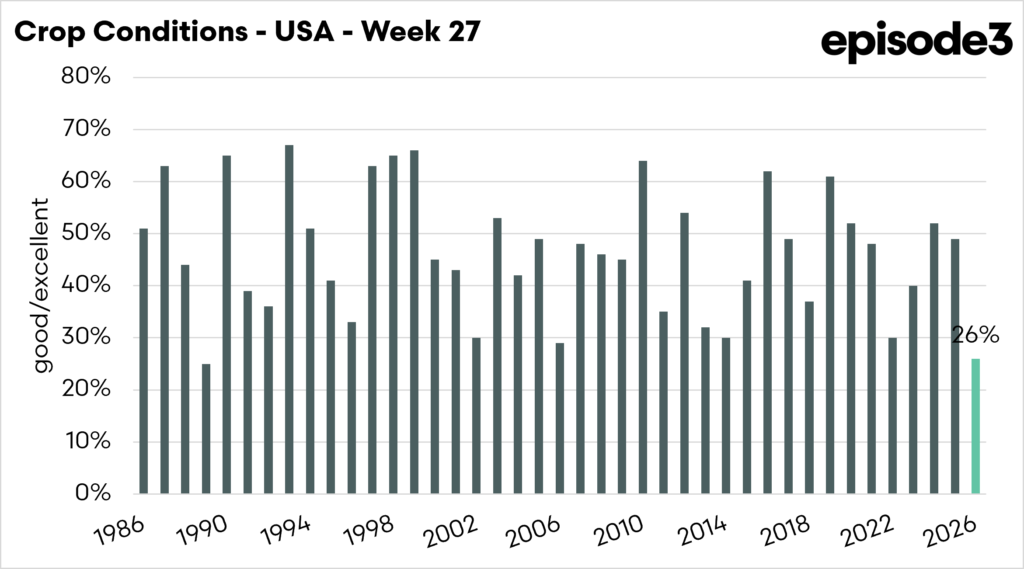

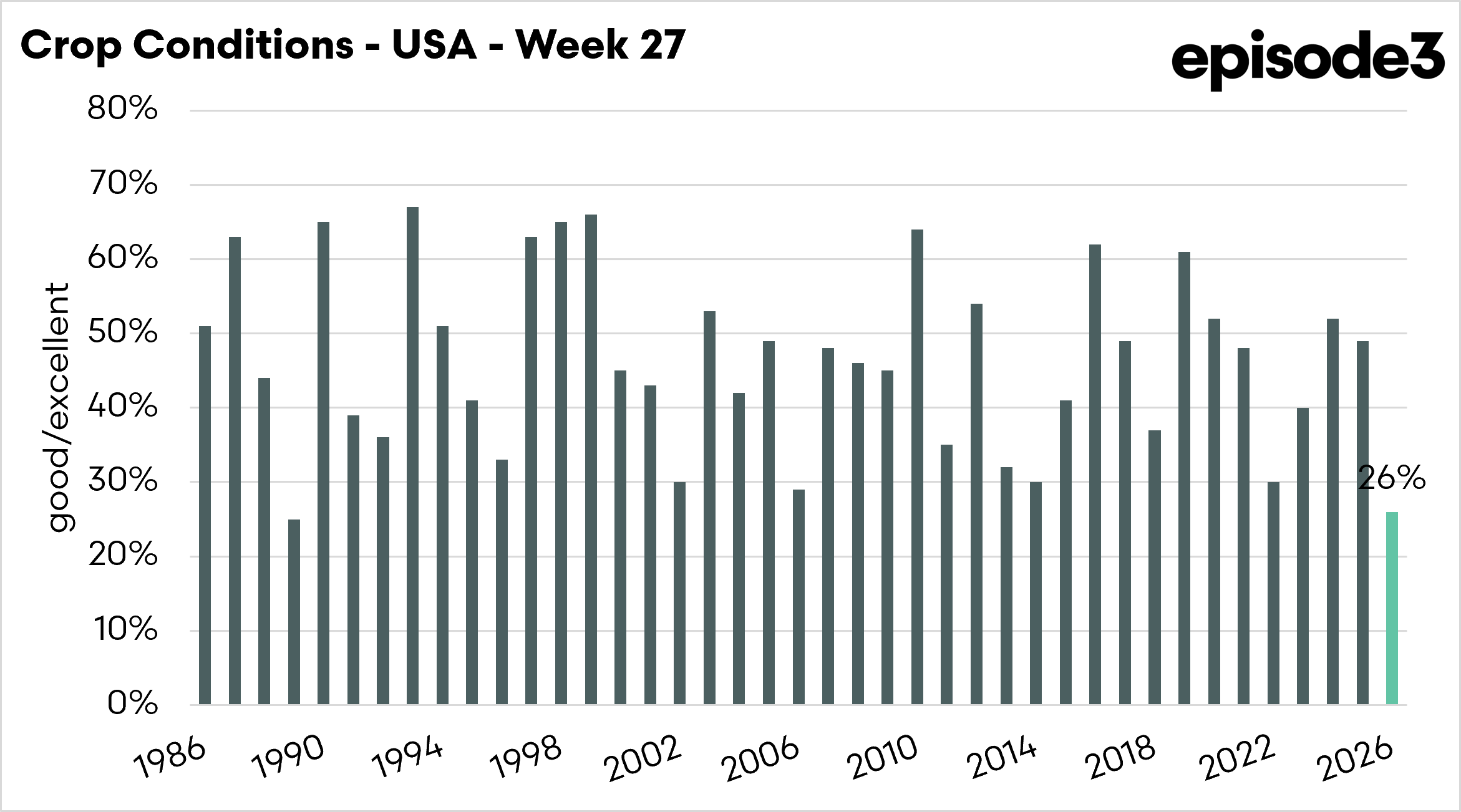

The latest US crop update was mixed. Corn and soybean condition ratings eased slightly but still point to solid production if favourable weather continues through July. Spring wheat conditions improved to 59 per cent good-to-excellent, while winter wheat stays historically poor at just 26 per cent. Harvest has also progressed more slowly than expected, raising concerns around quality rather than outright production. The market, however, appears comfortable with a smaller US winter wheat crop, as larger crops elsewhere offset the loss.

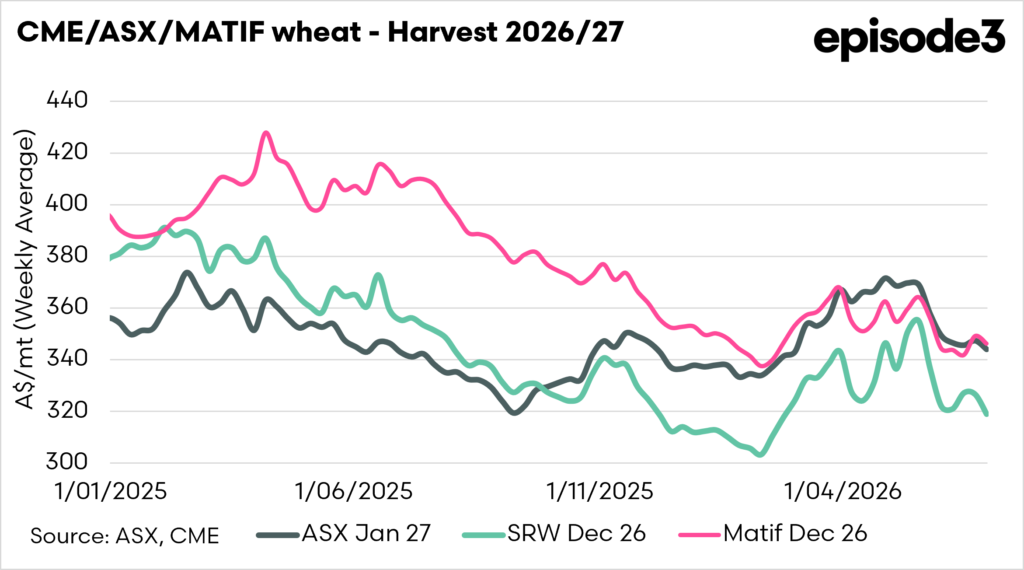

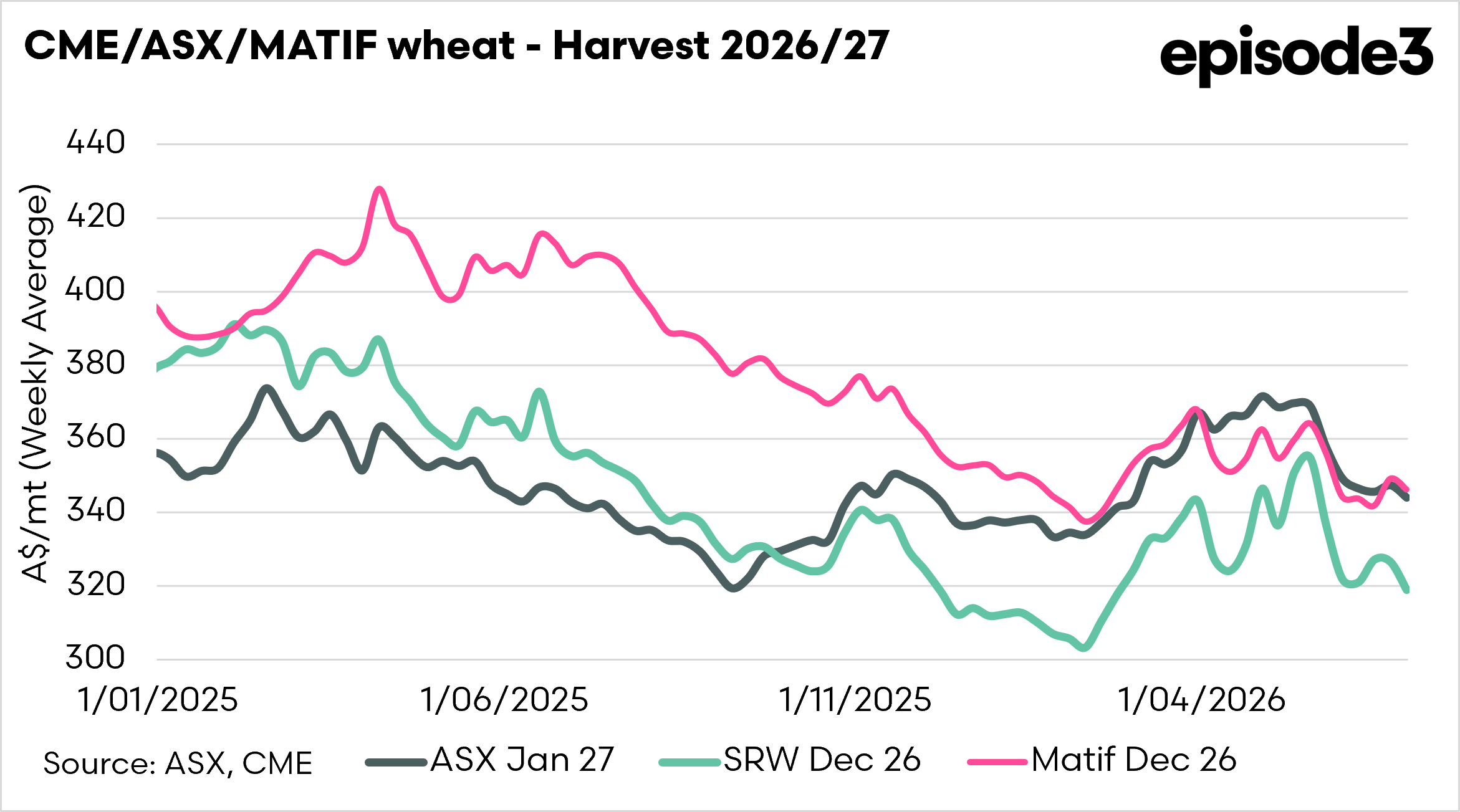

That “elsewhere” continues to be Russia. Another production upgrade now places the Russian wheat crop above 91 million tonnes, one of the country’s largest harvests outside the record 2022 season. Harvest is underway, and Black Sea export competition remains fierce, with Russian export prices continuing to edge lower. As long as Russian wheat keeps flowing, it is still difficult to build a sustained bullish case for global wheat.

Attention is also shifting away from wheat and towards summer crops. Europe’s heatwave has had only a modest impact on wheat, much of which is approaching maturity or already being harvested. Corn, however, is a different story. French maize conditions have deteriorated sharply, and estimates suggest production could fall heavily if hot, dry conditions persist. Oilseeds such as sunflower and soybeans are also becoming more vulnerable. India’s delayed monsoon has also left summer crop plantings well behind last year, with rice, corn and soybean area all significantly lower than normal. July rainfall will now be critical.

Despite these risks, grain markets have shown little concern. Funds continue to add to short positions across wheat and corn, suggesting traders remain confident that comfortable global inventories can absorb regional production setbacks. Global wheat stocks are ample, corn supplies are expected to be comfortable, and import demand from major buyers has been relatively subdued. The market is effectively betting that weather problems will remain regional rather than global.

Australian growers remain in a relatively favourable position. Widespread rainfall has further improved seasonal conditions across much of the southern grain belt, while NDVI readings suggest crop biomass is well above average across parts of the nations wheatbelt. Conditions in Western Australia also remain encouraging following useful rainfall in June. A developing El Niño still warrants close attention later in the season, but the domestic production outlook has improved in recent weeks.

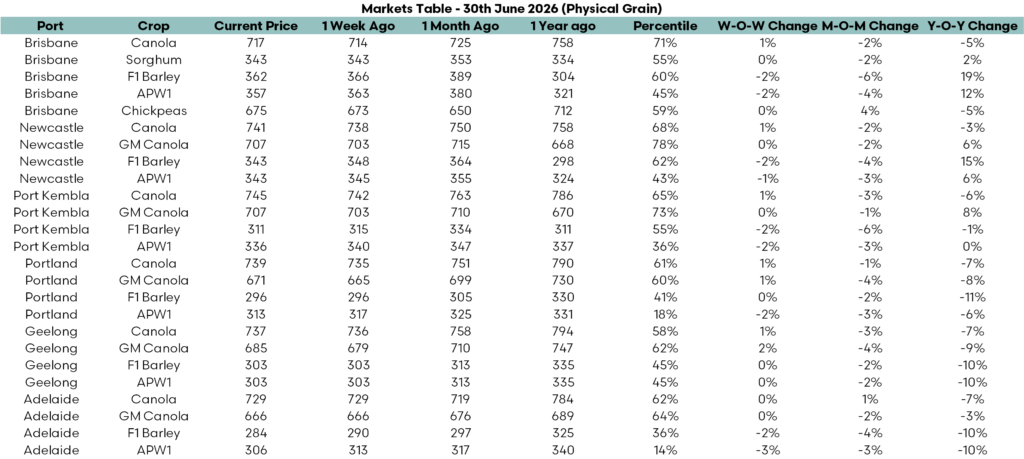

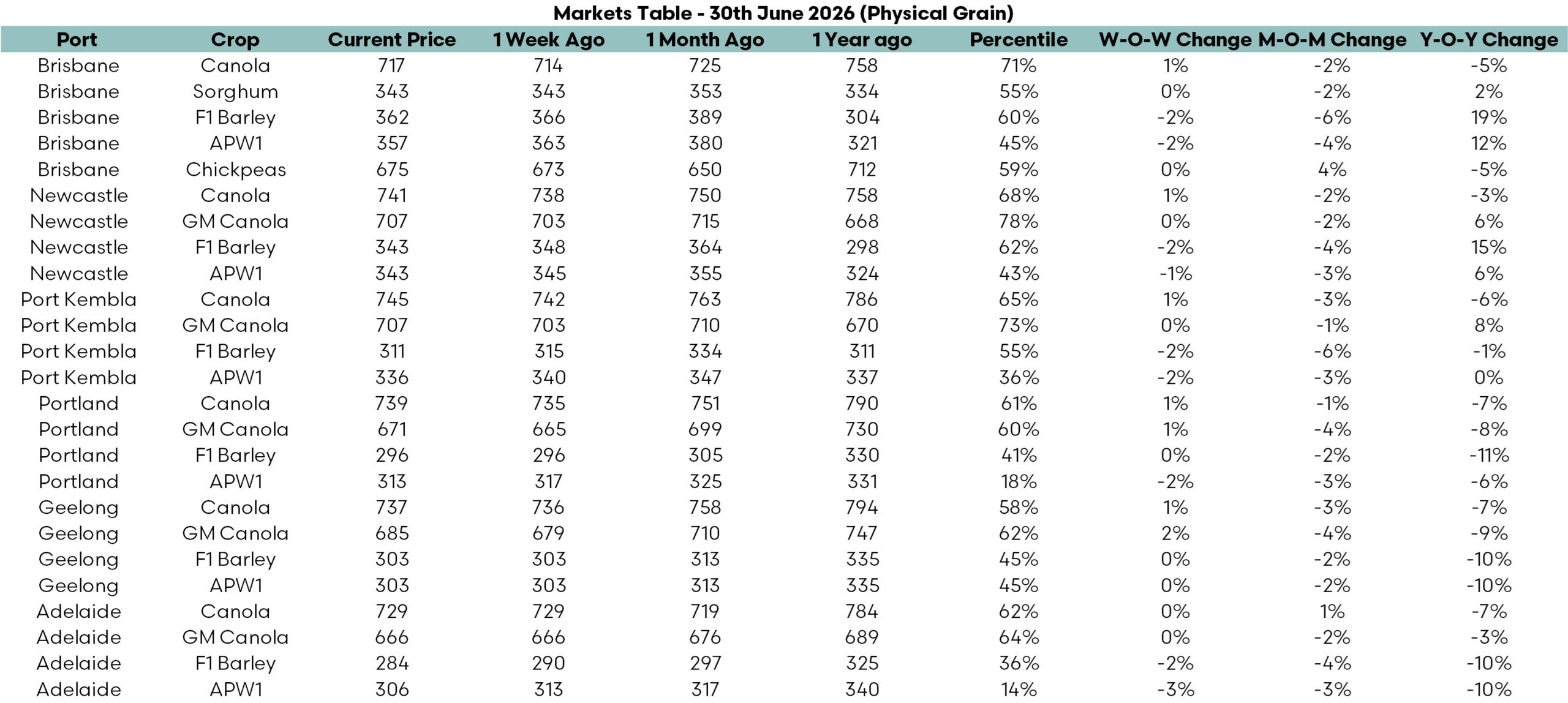

The accompanying market table reflects these competing influences. Australian wheat prices softened modestly over the week, with Brisbane APW1 easing 2 per cent and Newcastle APW1 slipping 1 per cent. Canola proved more resilient, recording small weekly gains across most ports. Internationally, Russian wheat fell another 3.3 per cent as harvest pressure intensified, while Minneapolis wheat dropped 7 per cent as improving spring wheat conditions weighed on prices. Encouragingly for growers, the cost side of the ledger continues to improve. Urea prices are now 29 per cent lower than a month ago and 17 per cent below year-ago levels, while crude oil remains around 21 per cent lower than a month earlier despite renewed instability in the Middle East.

For now, the market is still comfortable betting on another year of abundant global supply. Weather risks are building, and speculative short positions are becoming crowded, but until those risks translate into meaningful production losses, grain prices are likely to remain driven by supply rather than uncertainty.