Aye, Grain: Higher Costs, Half a Rally

The Snapshot

- Black Sea attacks and Sea of Azov restrictions drove a fresh wheat risk premium.

- Trump’s renewed conflict with Iran lifted energy, freight and fertiliser risk.

- French wheat conditions falling to 65 per cent supported the rally.

- Australian wheat prices rose only modestly because stocks and export competition are still heavy.

- Farmers face the risk of higher costs without receiving an equal lift in grain prices.

The Detail

Geopolitics finally moved the grain market this week, but Australian growers only received part of the benefit.

The immediate trigger was the renewed escalation between the US and Iran. Donald Trump, the inaugural FIFA peace prize winner, has effectively opened another war front in the Middle East, with US strikes on Iran, retaliation across the Gulf and a naval blockade due to begin around Iranian ports and oil terminals. The Strait of Hormuz is again sitting at the centre of the risk.

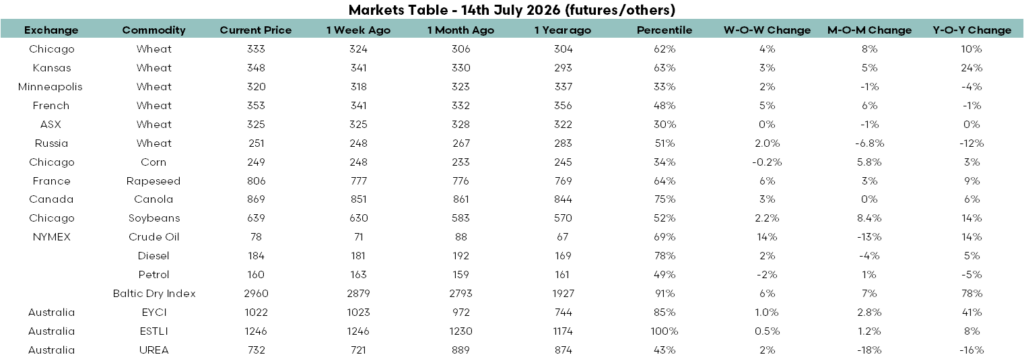

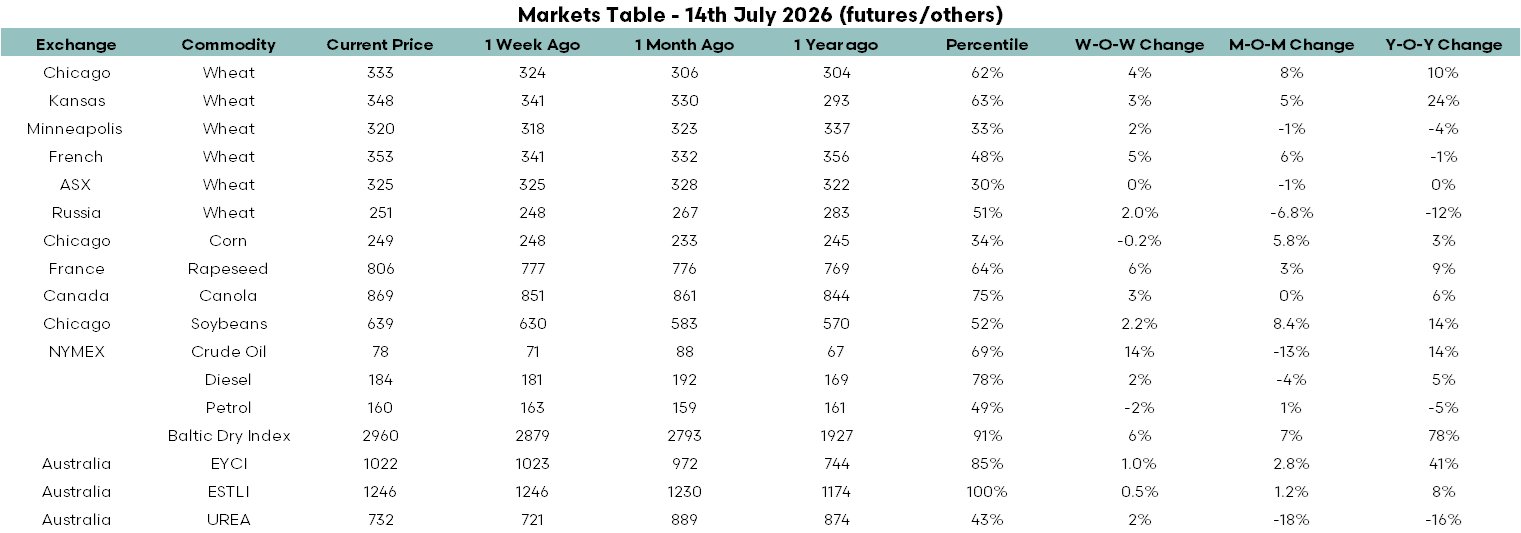

For agriculture, that matters well beyond oil. Hormuz is critical to global energy and fertiliser trade. Any serious interruption raises the cost of crude, diesel, urea, freight and marine insurance. Even where cargoes continue to move, the price of risk rises quickly. Crude oil jumped 14 per cent over the week, while the Baltic Dry Index rose 6 per cent and is now 78 per cent above year-ago levels.

Russia and Ukraine also decided to remind the market that the Black Sea is not immune to disruptions to the free flow of trade.

Shipping through the Sea of Azov was restricted following Ukrainian attacks on Russian commercial vessels. The route handles around a quarter of Russia’s grain exports. On the Ukrainian side, Kernel halted operations at Chornomorsk after repeated Russian strikes damaged grain, sunflower oil and meal infrastructure. Civilian vessels and port assets around Odesa were also hit.

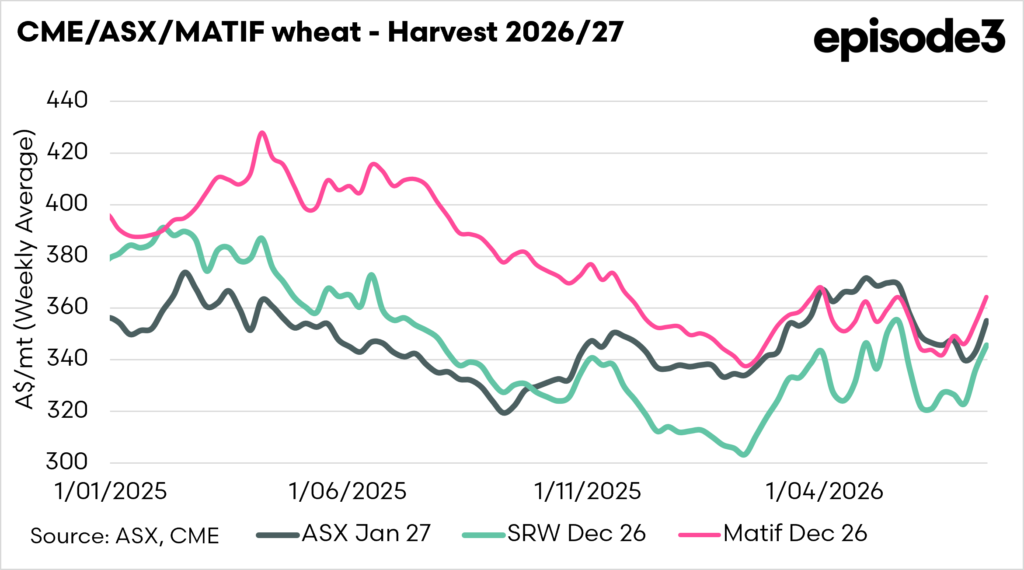

That combination pushed wheat sharply higher. French wheat rose 5 per cent over the week, Chicago gained 4 per cent, and Kansas wheat added 3 per cent. Traders were not pricing a confirmed shortage. They were pricing the chance that Russian or Ukrainian grain could be delayed, rerouted or stranded if attacks continue.

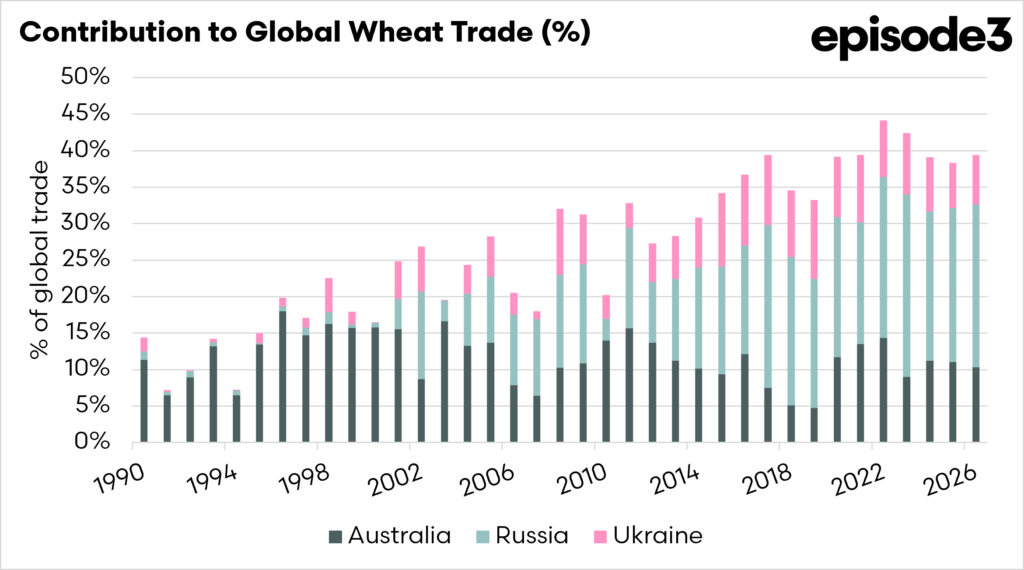

This is still important. Russia is the world’s largest wheat exporter, and the Black Sea remains central to price formation. A few days of disruption can be worked around. Several weeks of restricted access would be a different matter.

The rally also had some production support. French soft wheat conditions have fallen to 65 per cent good to excellent, down from 77 per cent a month ago. That does not make France a failed crop, but it weakens the comfortable supply story that had kept a lid on European wheat. When production confidence starts slipping, traders are more willing to hold a geopolitical premium.

The problem for Australian growers is that local wheat is carrying its own baggage.

Australian wheat exports rebounded to 2.09 million tonnes in May, up 46 per cent from April, but the broader export pace is still underperforming. Australian wheat has been uncompetitive in several destinations as Northern Hemisphere harvest pressure approaches.

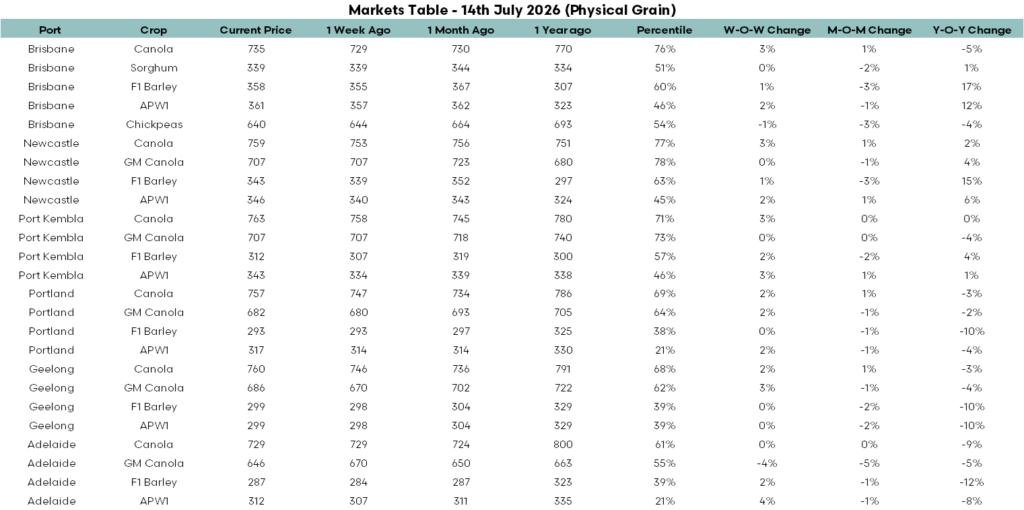

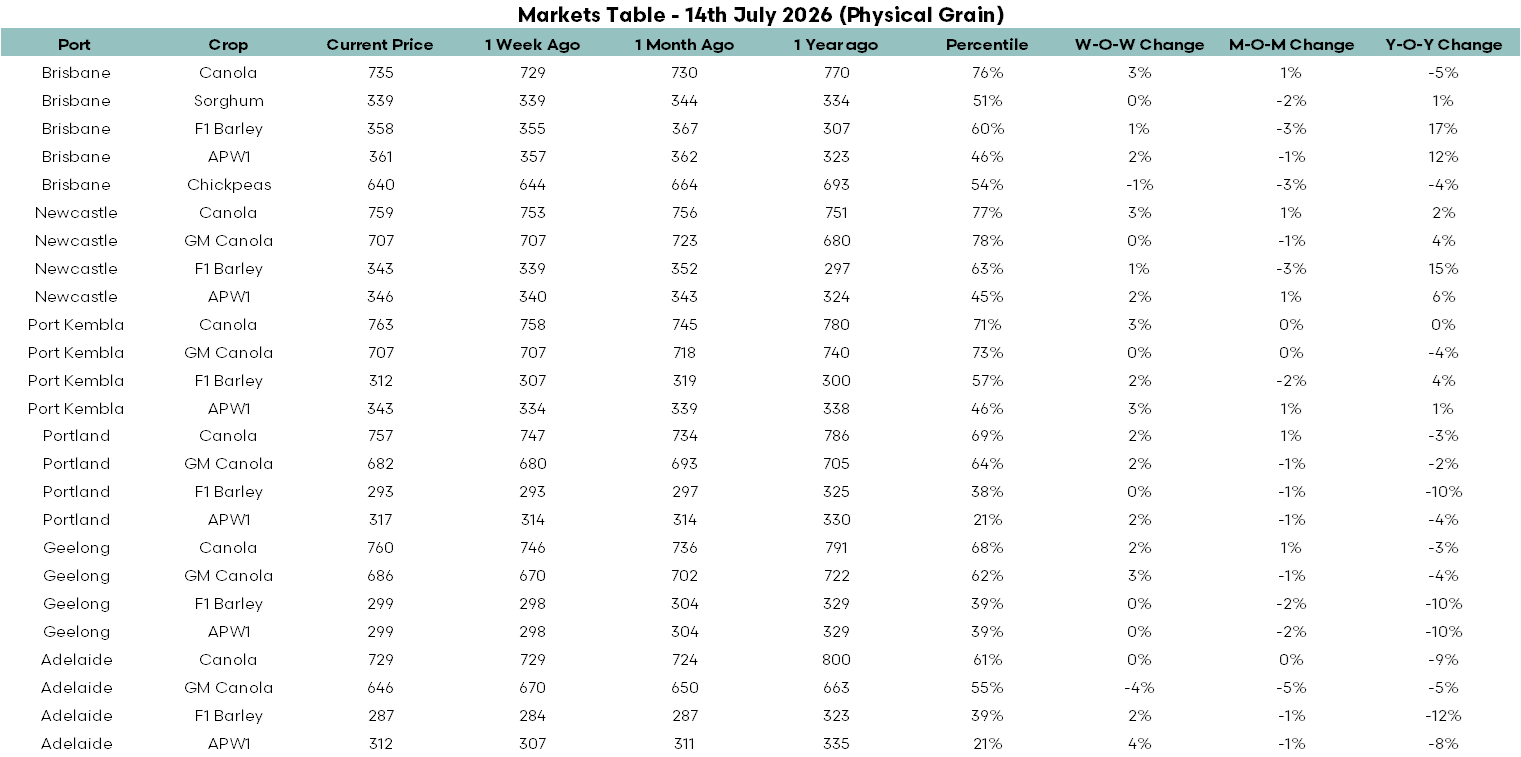

That is why Australian cash wheat only captured a diluted version of the overseas rally. APW1 gained across most eastern ports, but the moves were modest. Port Kembla and Adelaide were the strongest, while southern Victorian prices barely shifted. ASX wheat was unchanged at $325/t.

There is a temptation to see rising global wheat futures and assume Australian prices must follow. Recent weeks and months have shown that it doesn’t necessarily happen. Futures can rally on war risk while local basis weakens under the weight of stocks, sluggish export demand and the prospect of another large crop.

Canola responded more clearly. French rapeseed rose 6 per cent, Canadian canola gained 3 per cent, and Australian canola prices improved across most ports. Oilseed markets are more directly exposed to energy, vegetable-oil trade and Black Sea sunflower disruption, so the geopolitical connection is cleaner.

The most uncomfortable part of this week is that geopolitical instability will offer a catch 22, higher prices due to events in Russia helping grain prices, but the war in Iran extending the high input pricing environment.

The table tells the story plainly. Global wheat and oilseeds rose; Australian cash wheat edged higher; ASX wheat went nowhere; crude and freight jumped; and urea stopped falling. War added risk to the market, but Australia’s heavy balance sheet kept much of the wheat rally offshore.