Food inflation update Feb 2026

Food Inflation Update - Feb 2026

Food inflation continues to fragment, and February reinforces the shift away from broad-based price pressure toward category-specific movements.

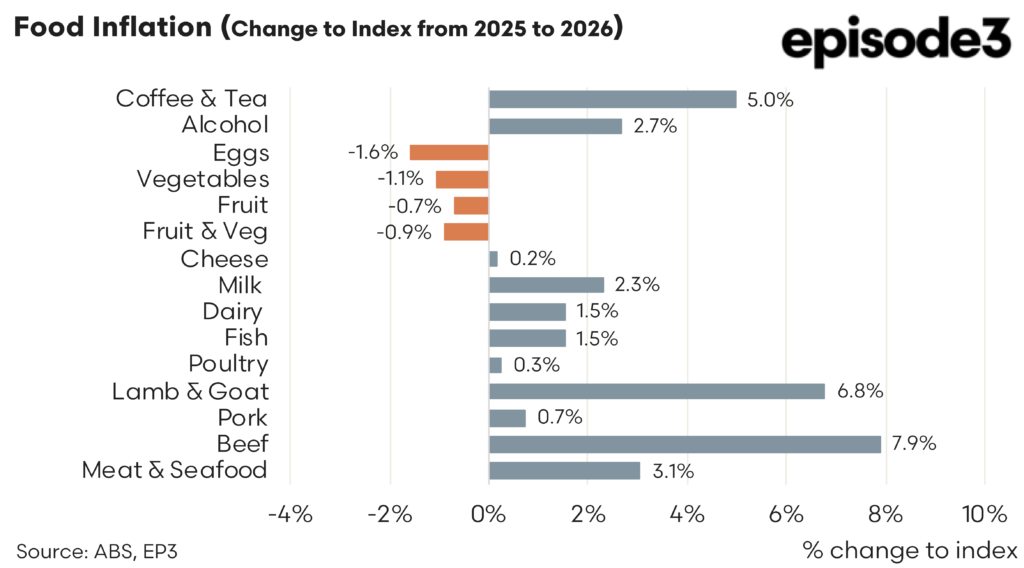

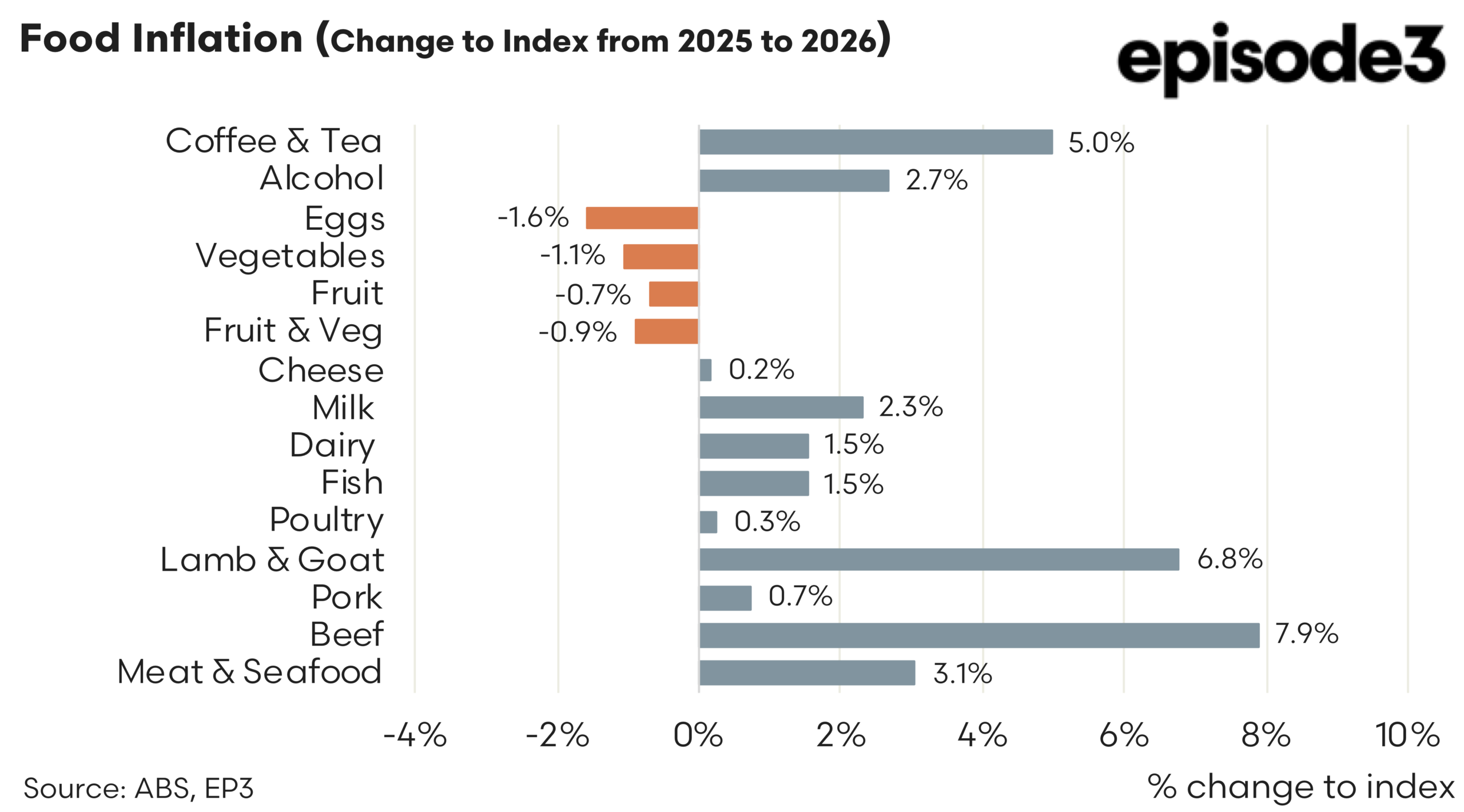

On an annual basis, meat remains the dominant driver. Beef has accelerated further, now up 7.9pc, while lamb and goat sit at 6.8pc, both reflecting tighter supply and sustained export demand. The aggregate meat and seafood category is up 3.1pc, masking the divergence within it, where red meat is doing the heavy lifting while other proteins lag behind.

Outside of meat, inflation is far less consistent. Coffee and tea remain elevated at 5.0pc, continuing to reflect global supply constraints rather than domestic conditions. Alcohol is up 2.7pc, while dairy is more subdued, with milk up 2.3pc and the broader dairy category up 1.5pc. Fish is also sitting at 1.5pc, while poultry and pork remain relatively flat, reinforcing the idea that not all proteins are moving together.

Fresh food tells a very different story. Eggs are down 1.6pc year on year, vegetables down 1.1pc, fruit down 0.7pc, and combined fruit and veg down 0.9pc. This reflects improved seasonal supply and highlights how quickly inflation can reverse in categories driven by production cycles.

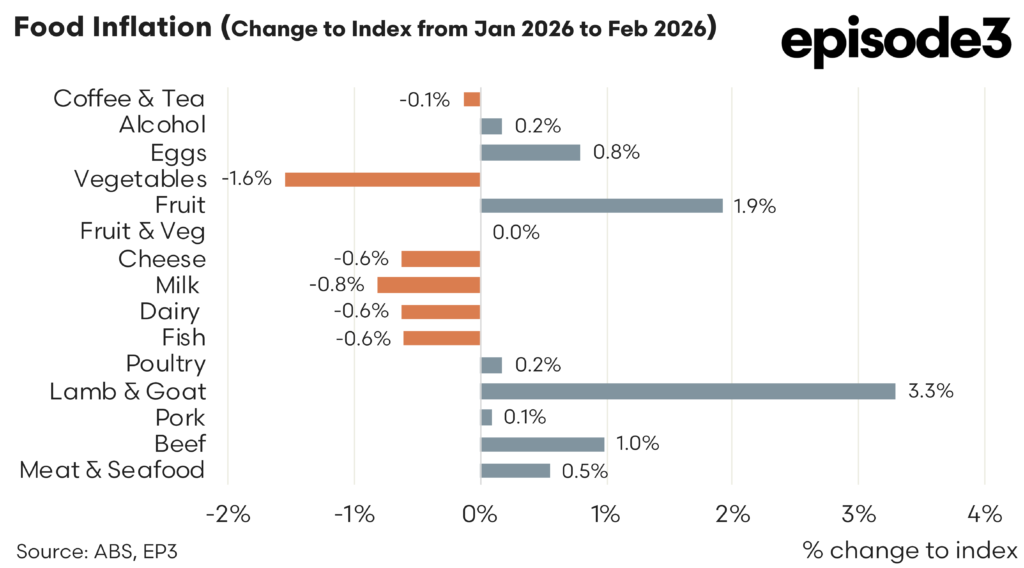

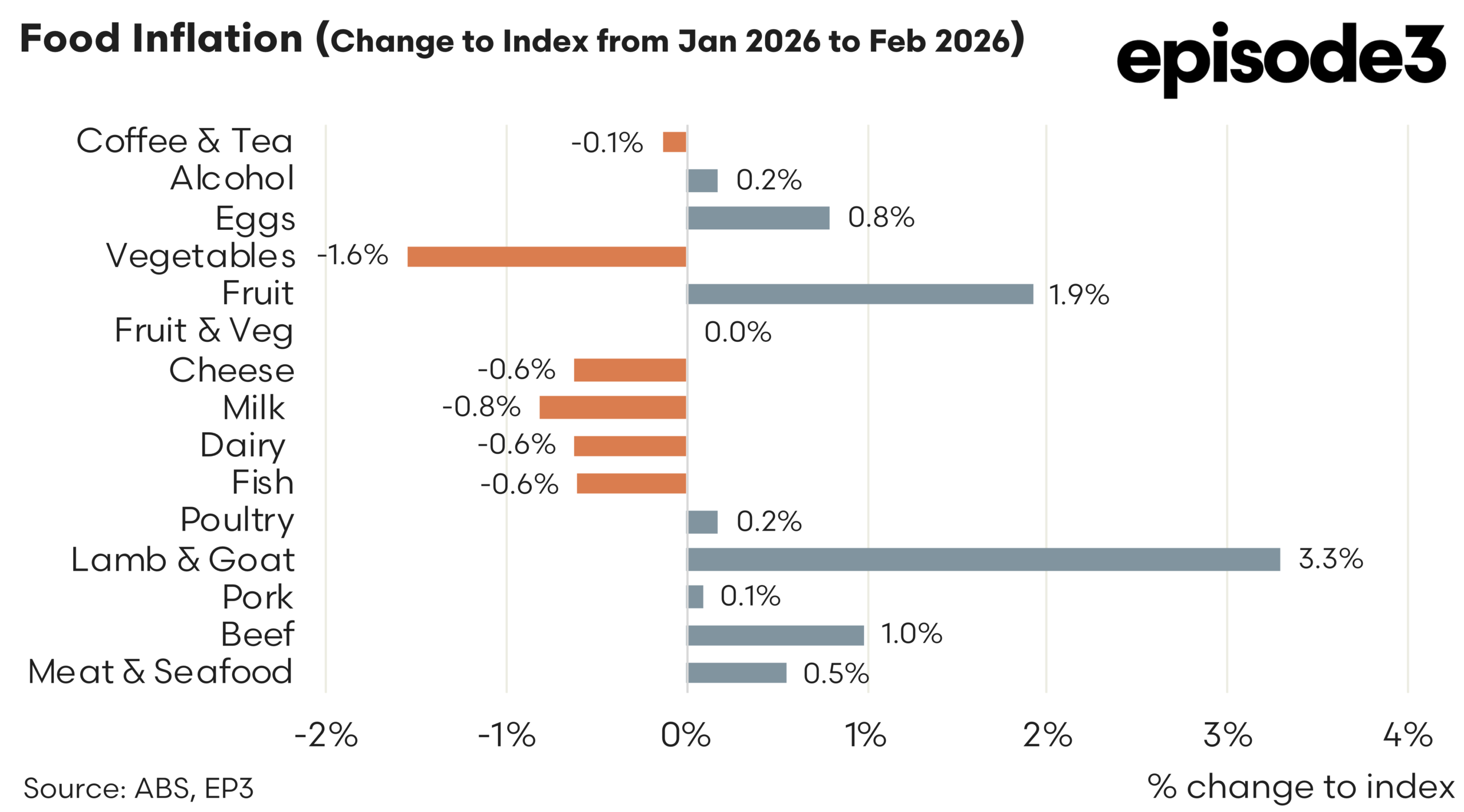

The monthly data for February adds another layer to the story. Lamb and goat recorded a sharp 3.3pc rise in the month, standing out as the key mover. Beef also pushed higher, up 1.0pc, while fruit rose 1.9pc, showing short-term volatility despite the softer annual trend.

In contrast, vegetables fell 1.6pc over the month, and dairy categories broadly declined, with milk down 0.8pc and cheese, dairy and fish all down 0.6pc. Coffee and tea were slightly negative on the month, while most other categories showed only marginal movement.

The key takeaway is that food inflation is no longer a single narrative. Red meat remains structurally supported and continues to push higher, while fresh food is easing and highly reactive to seasonal conditions. At the same time, globally influenced categories like coffee are holding firm, creating a patchwork of inflation outcomes rather than a uniform trend.

For consumers and producers alike, this means the focus needs to shift from headline inflation to the underlying drivers within each category. The era of everything rising together has passed. What matters now is which commodities are tight, which are recovering, and how quickly those cycles are turning.