Managed trade is back, and Australian agriculture is exposed

The Snapshot

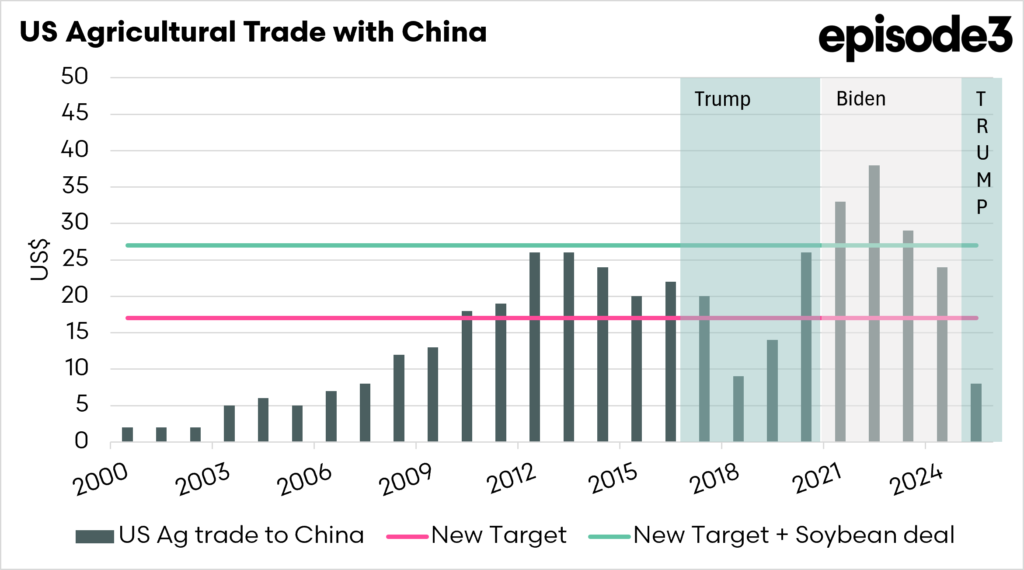

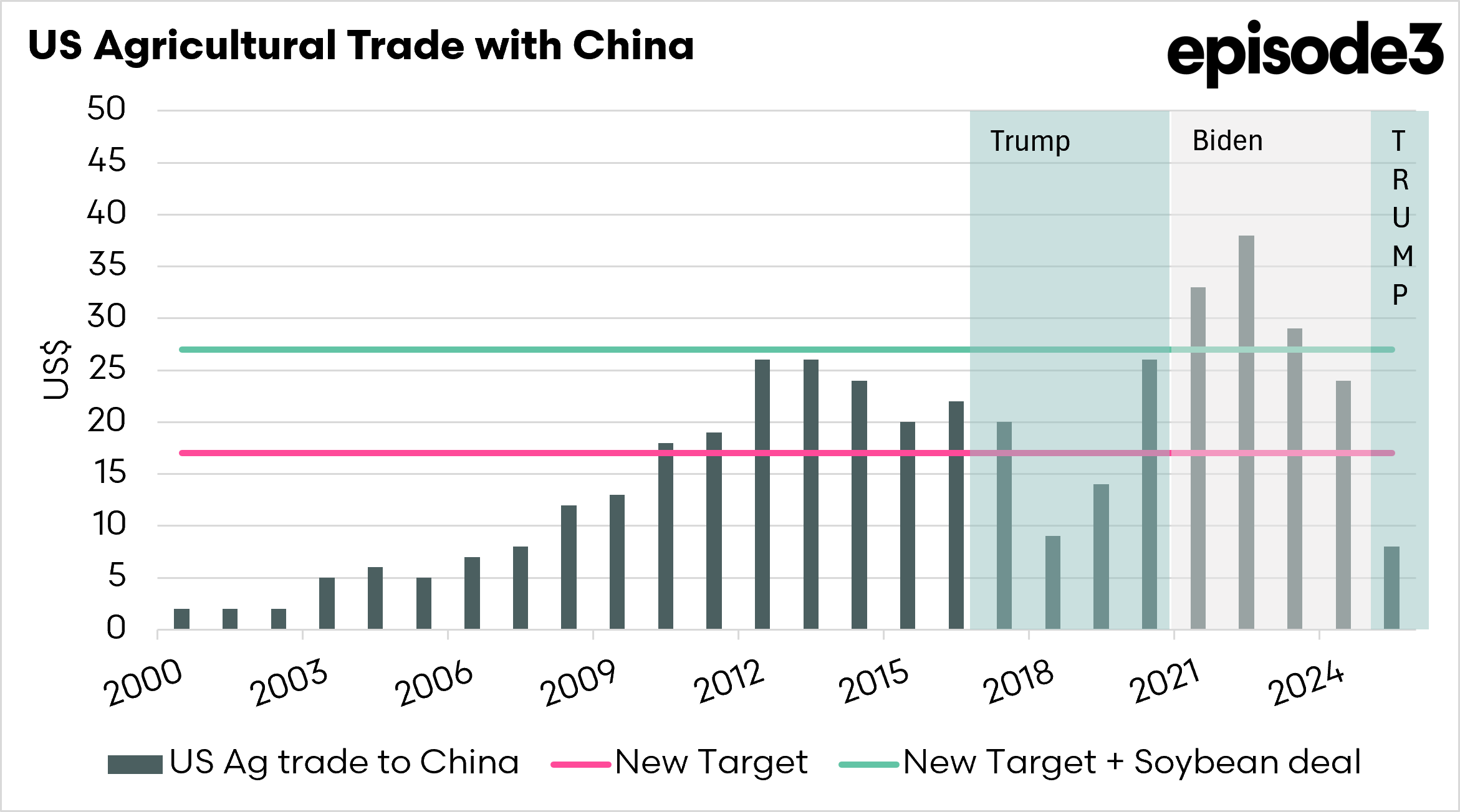

- China’s $17bn commitment is less impressive than it sounds; they were buying $24bn as recently as 2024

- Trade collapsed to $8bn in 2025, making the “recovery” look bigger than it is

- Add soybeans, and the real package is closer to $27bn, which is still not unprecedented levels.

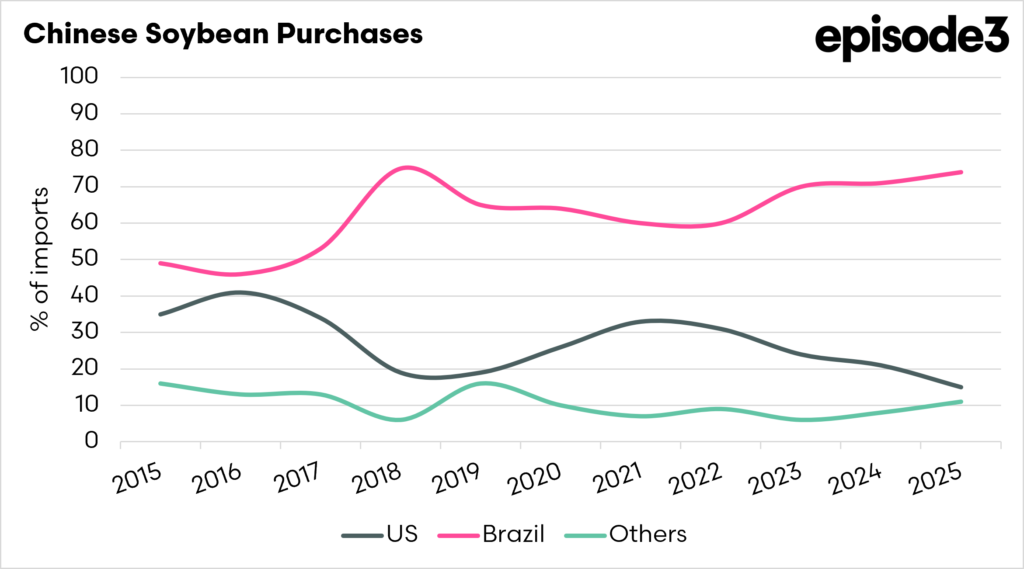

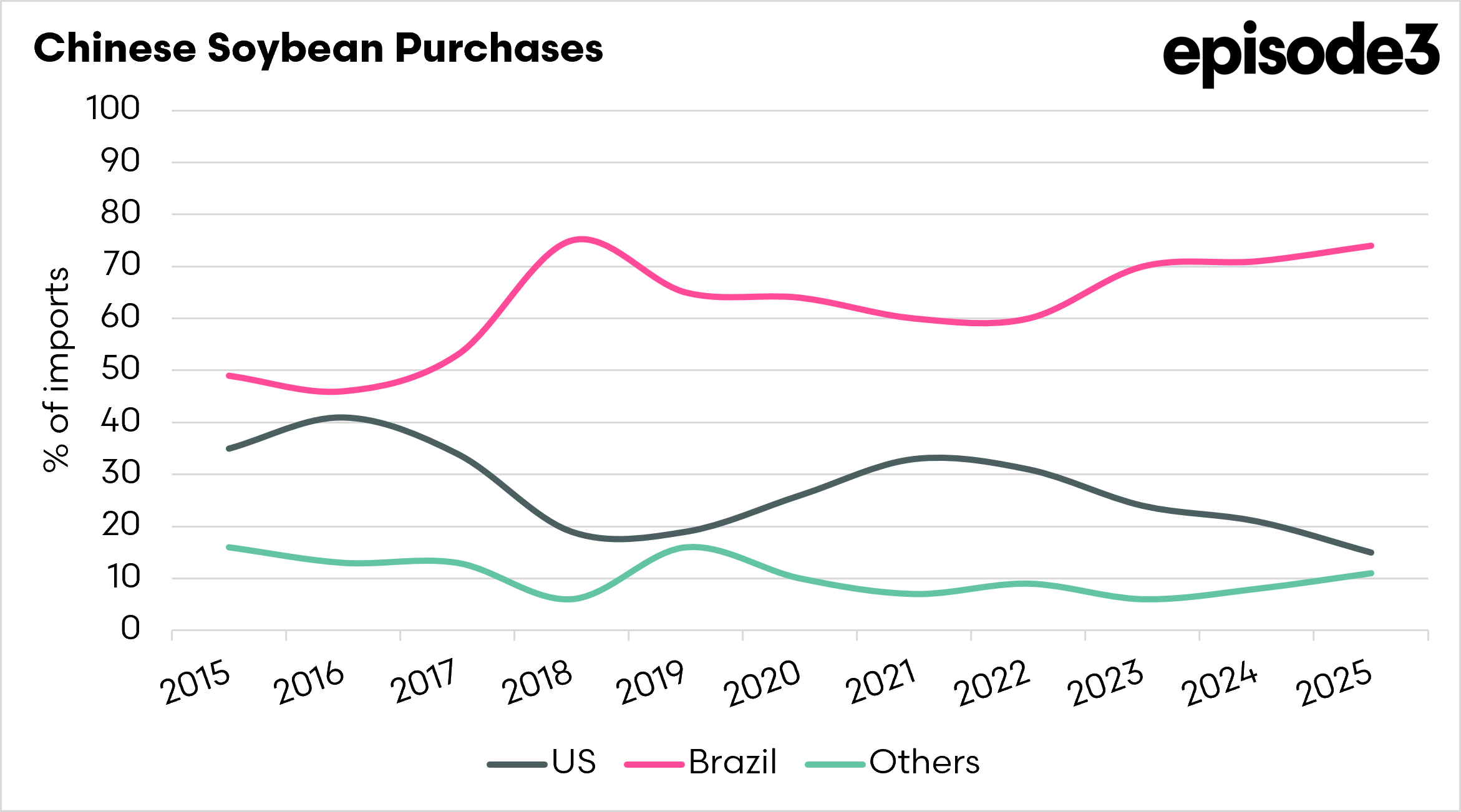

- Brazil took soybean market share from the US during the trade war years, and this deal is largely about clawing that back

- The real risk for Australia isn’t the volume China buys, it’s whether political deals decide who they buy it from

The Detail

Trump and his entourage have flown back to the USA with a deal for American farmers. An agreement by China to purchase US$17 bn worth of agricultural commodities.

China’s commitment to buy at least US$17 billion of US agricultural products each year in 2026, 2027 and 2028 looks like a major win for Donald Trump. It is a clean number, it is politically useful, and it gives the White House a simple message to take back to American farmers: the hard line on China has delivered.

Trade deals with our biggest market do impact us in Australia. It is the details that matter more than the headline. The US$17 billion figure is significant, but it is also not especially large when compared with recent China-US agricultural trade. Based on annual US agricultural export data, China has bought more than US$17 billion of US agricultural products in most years since 2010. It bought around US$20 billion in 2017, before the first Trump trade war properly disrupted flows. It bought US$26 billion in 2020, US$33 billion in 2021 and US$38 billion in 2022. Even in 2024, China still bought around US$24 billion of US agricultural products.

That context matters. The US$33 billion in purchases occurred in 2021 during the Phase One purchase period, although China still fell short of the full target. The US$38 billion bought in 2022 came after the formal Phase One purchase window had ended, but it still reflected the post-Phase One recovery in trade flows. In other words, the high-water marks in recent China-US agricultural trade were not normal, free-market years. They were shaped by the aftermath of managed trade.

The reason US$17 billion sounds dramatic now is that trade collapsed to around US$8 billion in 2025 after renewed tariff disruption. Measured against that very low base, it looks like a major recovery. Measured against the broader history of China-US agricultural trade, it looks more like a partial rebuilding of broken trade flows.

There is, however, one important caveat. The White House has said the US$17 billion commitment does not include the soybean purchase commitments China made in October 2025. That matters because soybeans are normally the biggest US agricultural export to China. If China honours that soybean commitment, it could add roughly another US$10 billion per year to the package. On that basis, the total agricultural commitment could be closer to US$27 billion annually once soybeans are included.

That makes the deal more meaningful than the US$17 billion headline alone. It moves it from being a modest recovery number into something closer to the stronger years of China-US agricultural trade. But even then, it is not unprecedented. China bought US$33 billion in 2021 during the Phase One period and US$38 billion in 2022, the post-Phase One recovery year. This is not China suddenly buying an extraordinary volume of American agriculture. It is China being pulled back toward US supply after several years in which trade flows shifted heavily away from the US. The biggest example is the change in trade flows with Soybeans, with Brazil moving from 56% of Chinese purchases the year prior to the first Trump administration to 74% in 2025.

The key issue is not whether China is buying more overall. The key issue is whether China is being encouraged, or required, to buy more of that food from the US.

Agricultural trade normally works on a mix of price, freight, quality, and availability. Buyers compare origins and purchase where the numbers make sense. Under a politically negotiated purchase agreement, that process becomes less clean. The marginal tonne may not necessarily go to the most competitive supplier. It may go to the supplier needed to satisfy a bilateral target.

That is where Australia needs to pay attention. China is a critical market for Australian agriculture, the United States is far more important for the Chinese economy.

This was the risk we found during the first Trump term. When the original Phase One deal was announced, the concern was not simply that China would buy more from the US. It was that China would be required to give preference to US agricultural commodities, potentially displacing other exporters. At the time, the EP3 analysts outlined several Australian sectors that could be exposed, including wine, beef, barley, dairy, almonds, crustaceans, wood products, skins and malt extract. Many of those sectors later experienced some form of trade disruption or restriction.

That does not mean every disruption was caused by Phase One. Trade politics is rarely that simple. But the broader lesson remains valid. When governments start managing agricultural flows, exporters can be displaced for reasons that have little to do with price, quality or competitiveness.

Beef will naturally attract attention, especially as China works to restore access to US beef facilities. That is relevant, but access does not automatically create volume. The US cattle herd is still tight, US cattle prices are historically high, and the US does not have a large pool of cheap surplus beef waiting to be redirected into China. The more important issue is not whether US beef suddenly floods China. It is whether access, combined with political purchase commitments, gives US farmers an advantage that they would not otherwise have on commercial terms.

For grains and oilseeds, the soybean commitment is the obvious centrepiece. China has reduced its reliance on US soybeans compared with the pre-trade-war period, with Brazil taking a much larger share of Chinese demand. A renewed commitment to buying large volumes of US soybeans is therefore less about creating new demand and more about clawing back market share from other origins. That could support US oilseed values and influence global pricing, but it also reinforces the broader risk: China’s buying pattern may be shaped by diplomatic obligations rather than the cheapest or most efficient supply chain.

For Australia, the conclusion is not that this deal is automatically bad. Higher US values can sometimes support global agricultural markets, and stronger Chinese demand is rarely a negative in a broad sense. But this is not a normal demand story. It is a managed trade story.

The US$17 billion headline is not historic on its own. Add an estimated US$10 billion of soybeans, and the package becomes more substantial, but still not unprecedented. The real issue is the structure of the agreement. If China is drawn into managed agricultural trade with the US again, Australia may not just be competing against another origin. It may be competing against a political obligation.

Australia needs to be very vigilant of preference deals. When China’s buying decisions are shaped by diplomatic obligations rather than commercial logic, competitive advantages built over decades lose their importance. Australia has spent years rebuilding agricultural access to China, and a deal like this could move us down the ranking of importance.

The risk now is not a sudden shock but a slow erosion of Australian market share quietly redirected, not because the Australian product is inferior, but because a deal with the United States is more beneficial to their economy.