Food inflation update Mar 2026

Food Inflation Update - Mar 2026

Australia’s food inflation story took a firmer turn through March, with the latest Consumer Price Index data showing a renewed lift in monthly price momentum alongside an already elevated annual backdrop.

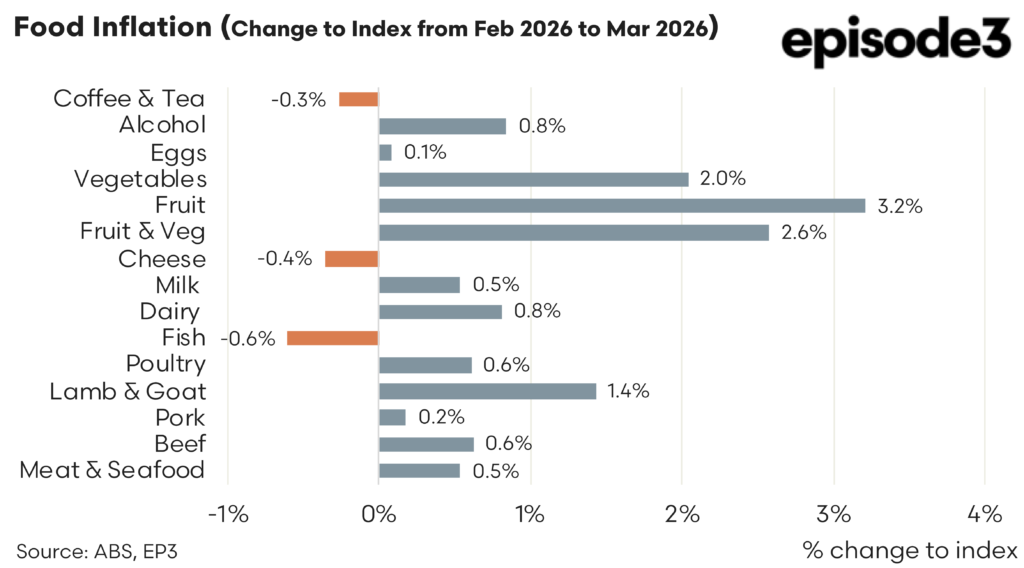

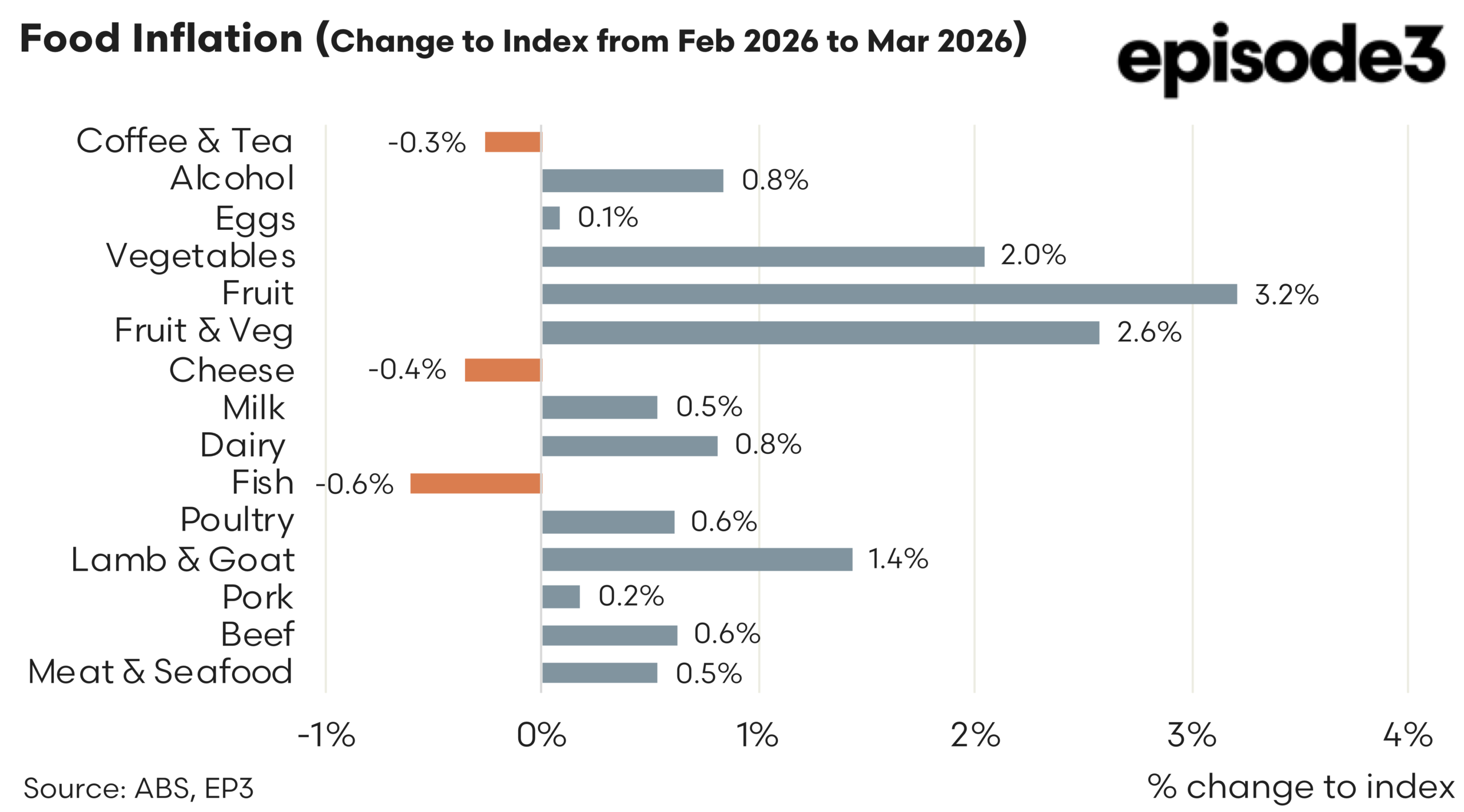

While the broader inflation cycle remains uneven, the March update highlights a shift, with fresh food prices rebounding and protein continuing to underpin the annual trend. The result is a food basket that is still diverging across categories, but with more areas now pushing higher rather than easing. The monthly movement from February to March shows a clear shift in short-term momentum, with fresh food providing the largest contribution to price increases.

Fruit prices rose sharply, lifting 3.2pc for the month, while vegetables increased 2.0pc. Combined fruit and vegetable prices climbed 2.6pc, marking a strong rebound after earlier softness and highlighting the ongoing volatility typical of seasonal produce.

Protein categories continued to edge higher. Lamb and goat prices increased 1.4pc over the month, while beef rose 0.6pc and poultry lifted 0.6pc. Pork recorded a smaller gain of 0.2pc. These movements reinforce the steady underlying strength in meat pricing, even as monthly volatility remains lower than in fresh produce.

Dairy prices moved modestly higher, with milk up 0.5pc and dairy overall rising 0.8pc. Cheese was slightly weaker, declining 0.4pc. Fish prices fell 0.6pc over the month, providing some offset within the broader protein category. Beverage movements were mixed. Alcohol prices rose 0.8pc in March, continuing gradual upward pressure, while coffee and tea declined slightly by 0.3pc after earlier gains.

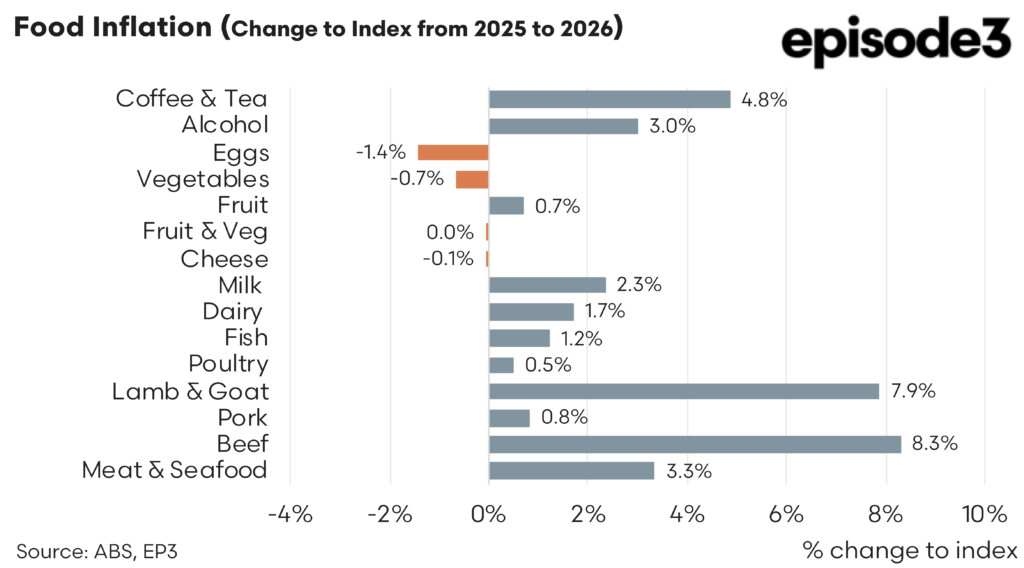

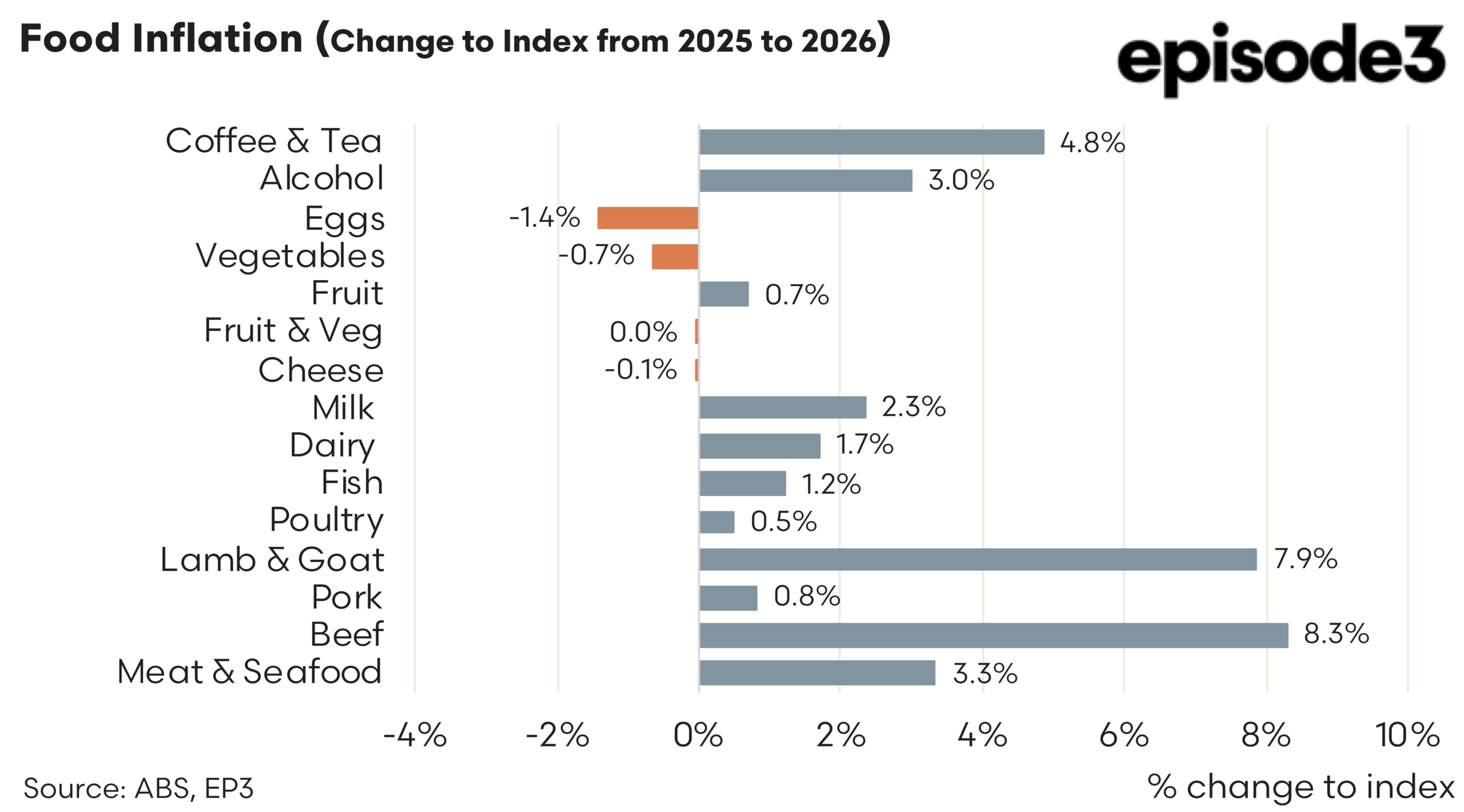

The annual picture into March 2026 continues to be dominated by protein and beverage categories.

Beef prices remain the standout mover, rising 8.3 percent over the year, reflecting ongoing tight cattle supply and strong export demand filtering into domestic pricing. Lamb and goat prices have also strengthened further, now up 7.9pc annually, reinforcing the impact of reduced flock numbers and steady global demand conditions. Together, these gains have pushed the broader meat and seafood category up 3.3pc over the year. Other proteins remain more subdued. Pork prices are up 0.8pc annually, while poultry has lifted just 0.5pc, indicating more balanced supply conditions in those sectors.

Beverages continue to contribute to inflation. Coffee and tea prices are up 4.8pc over the year, while alcohol has increased 3.0pc, reflecting a mix of global supply factors and ongoing cost pressures across production and retail.

Dairy prices remain moderate. Milk is up 2.3pc annually and dairy overall has lifted 1.7pc, while cheese is slightly negative at -0.1pc, suggesting stable conditions compared with the volatility seen in earlier years.

Fresh food remains the weakest part of the annual inflation story. Vegetables are down 0.7pc over the year and eggs have fallen 1.4pc, while fruit has edged just 0.7pc higher. Combined fruit and vegetable prices are effectively flat on the year, pointing to improved supply conditions and a normalisation after earlier disruptions.

The March data suggests food inflation is not reaccelerating in a broad sense, but it is becoming more widespread again after a period where easing in fresh food helped contain overall pressure. Protein markets remain structurally firm due to livestock supply cycles and export demand, while fresh food prices are proving volatile rather than consistently soft.

At the same time, beverages and some processed categories continue to reflect broader economic cost pressures. There is also a forward risk building, with any prolonged disruption through the Strait of Hormuz likely to push fuel and fertiliser costs higher, adding further upward pressure to food prices in the months ahead.