Forecast rain lifts confidence across eastern Australia

The Snapshot

- Rainfall forecasts have sharply improved sentiment across eastern Australian agriculture.

- Wheat markets remain firm despite easing geopolitical tensions and falling oil prices.

- Russian farmers are holding back wheat sales as a stronger ruble tightens exports.

- Canola markets weakened as crude oil prices dropped nearly 7pc during the week.

- Fertiliser and freight costs remain historically high despite recent easing in energy markets.

The Detail

Global grain markets spent the week pulling in two directions. Geopolitical sentiment improved, which should have been straightforwardly positive. Instead, markets spent most of the week sorting out what that actually means for energy, oilseeds and wheat, and the answers weren’t all the same.

The biggest single move was in crude oil. Brent dropped almost 7% after optimism emerged around US-Iran negotiations and the possibility that the Strait of Hormuz could eventually reopen. That’s a meaningful shift, and it hit agricultural markets quickly. I wouldn’t hold my breath for peace, as several previous negotiation attempts have broken down before reaching a final agreement.

ICE canola futures fell sharply as lower crude prices undercut the biofuel demand story that has been supporting oilseed values. Decent rainfall across parts of Western Canada didn’t help either, with improved crop sentiment adding to the selling pressure.

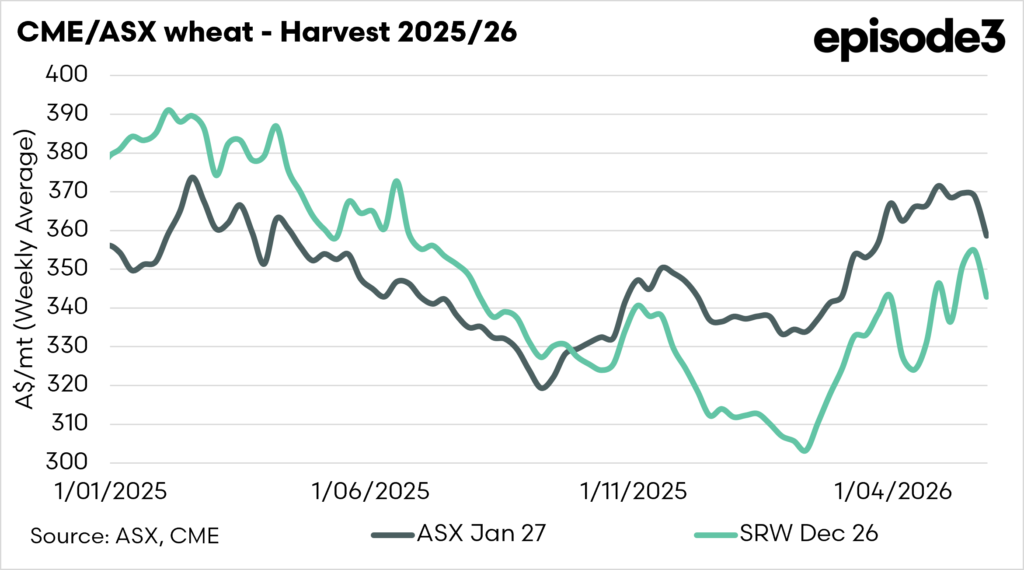

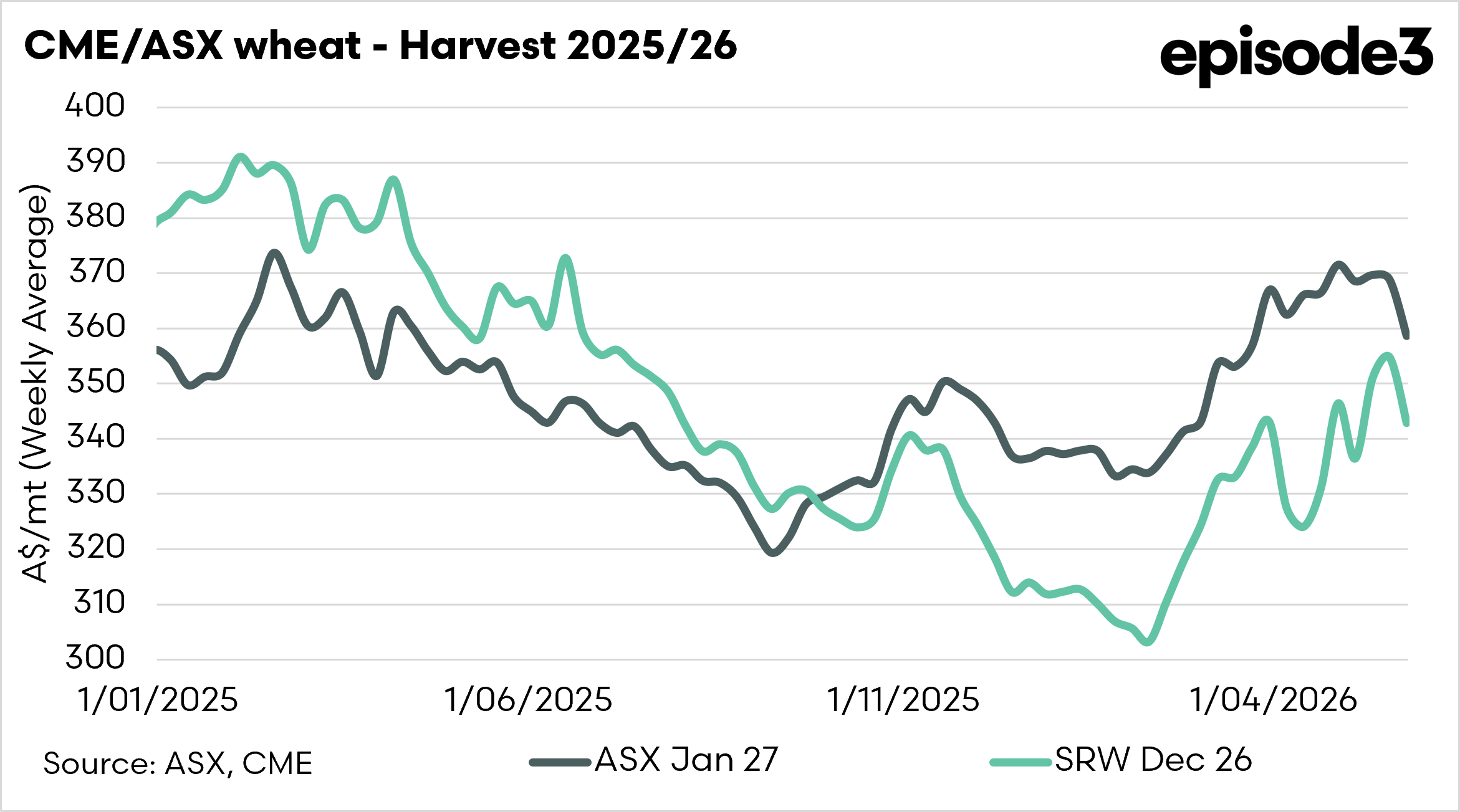

Wheat, though, held its ground. Russian export prices climbed again last week to around A$340/t FOB for 12.5% protein, the highest in roughly a year. The strengthening ruble is making exports less attractive, encouraging Russian farmers to sit on grain rather than sell. That matters more than it might sound. Russia has effectively been the world’s cheapest large-scale wheat supplier for the better part of two years. When Russian farmers pull back, the market loses its most aggressive source of pricing pressure, and values firm up elsewhere.

Russian spring sowing is running behind after cold weather earlier in the season, and crop potential there remains uncertain. In the US, dryness across parts of the Plains continues to keep the market cautious.

Argentina was another talking point. The government announced a gradual reduction in agricultural export taxes across soybeans, corn and wheat, designed to lift grower returns and eventually boost export volumes. The effect won’t be immediate, but for a country that dominates global soy trade, any policy shift that improves competitiveness is worth tracking.

Trade volumes were thin for much of the week, with the US Memorial Day holiday keeping participation down. Even so, markets held recent gains rather than giving them back, which says something about the underlying mood.

Closer to home, the seasonal picture in eastern Australia shifted considerably. Widespread rainfall is forecast across large parts of NSW, which has been desperately dry through autumn. Cattle prices have already moved in response, with some centres lifting strongly as graziers look to restock ahead of improved conditions. Winter crop establishment across NSW, Victoria and South Australia should also benefit if the rain delivers as forecast.

The rainfall outlook matters because conditions across parts of eastern Australia had become increasingly difficult after such a dry autumn. Many producers had already adjusted stocking decisions and crop expectations accordingly. That helps explain why the prospect of meaningful rainfall has been enough to quickly improve sentiment and lift cattle markets in some regions

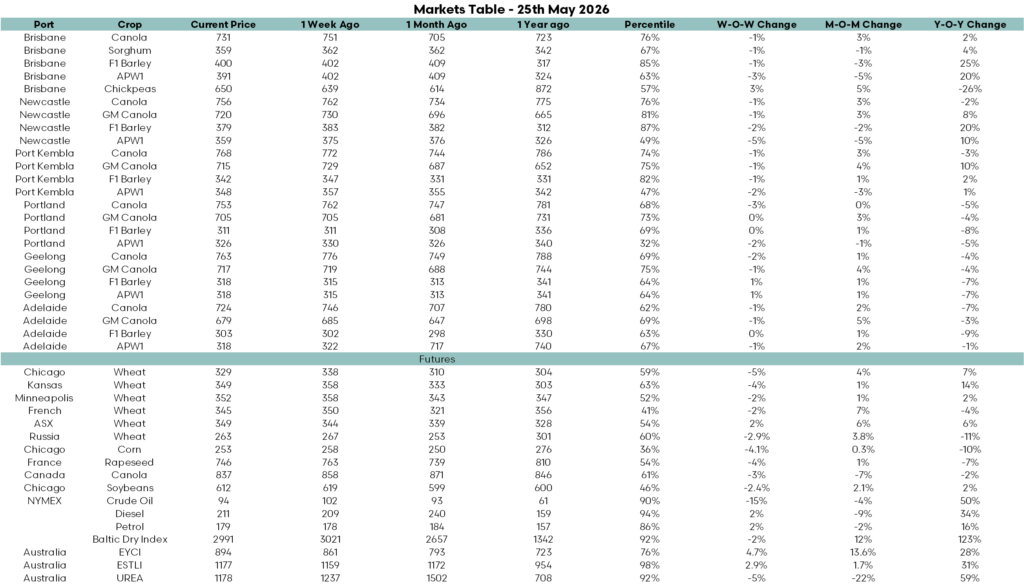

On the numbers, Chicago and Kansas wheat eased modestly after recent strength but remain well above year-ago levels. Northern Australian markets continue to hold firm, with Brisbane F1 barley in the 85th percentile and APW1 sitting nearly 20% above last year. Southern markets are softer. Canola weakened with global oilseeds. Urea has pulled back from recent highs, though fertiliser, fuel and freight costs remain high enough that margin pressure hasn’t gone away, even with grain prices where they are.