Market Morsel: The Russians are not coming.

Market Morsel

These days, when it comes to wheat markets, it’s really the black sea that matters. It’s where a huge chunk, over 30% of the global trade in wheat will come from. If the production in that region is good, then we will have poor prices and vice versa.

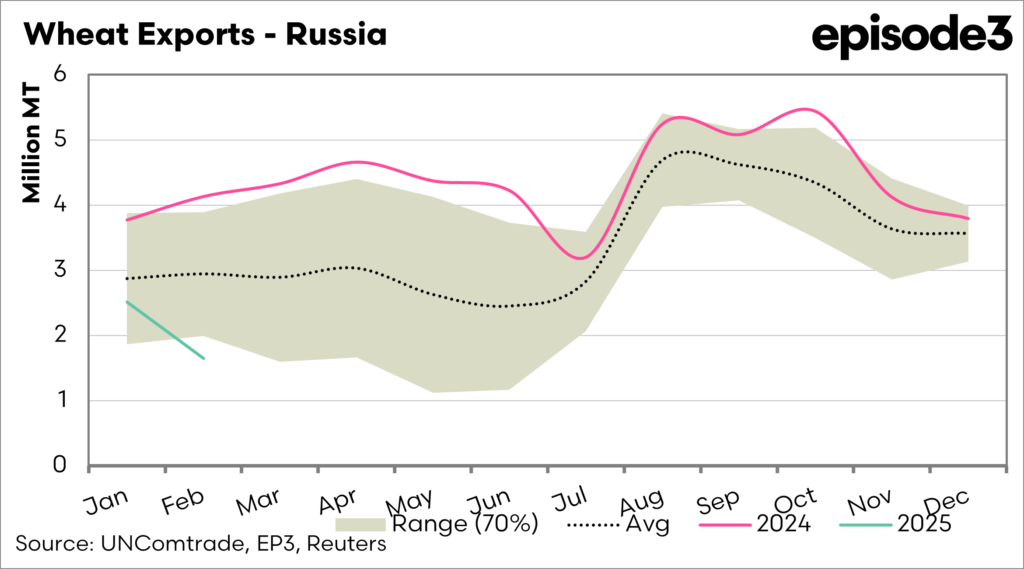

Let’s start with Russian exports. Russia tends to have its biggest export program from August to December. This is similar to Australia in that the biggest volumes get exported in the months immediately post-harvest. They then tend to dip in the January to June period.

We can see from the chart above that exports during January and February have been lower than average.

In December, Russia also amended the export quota on wheat from mid-February to June to 11mmt, increasing export tax. This has been done in order to prioritise the domestic market, and the cynic in me says to help support higher wheat pricing in overseas markets.

The result of this is that there will be less Russian wheat on the global market. Last year, according to Andrey Sizov, exports of wheat were 52.4mmt, and this year, the expectation is for 44.2mmt, a significant reduction.

The winter wheat crop in Russia is in strife, which we have discussed extensively over the past quarter. Russia will largely dictate our pricing, and if they cannot recover and projections continue as is, then they will have less to place on the market than they have in recent years.

As an analyst, I believe the market is probably at its most bullish since the Russian invasion of Ukraine. We just need to see a downward production in the black sea.

A lot will happen in this black sea space over the coming months, especially with the potential for peace to be negotiated. We’ll keep you updated on here and the AgWatchers podcast (click here).