The acid squeeze behind higher phosphate prices

Market Morsel

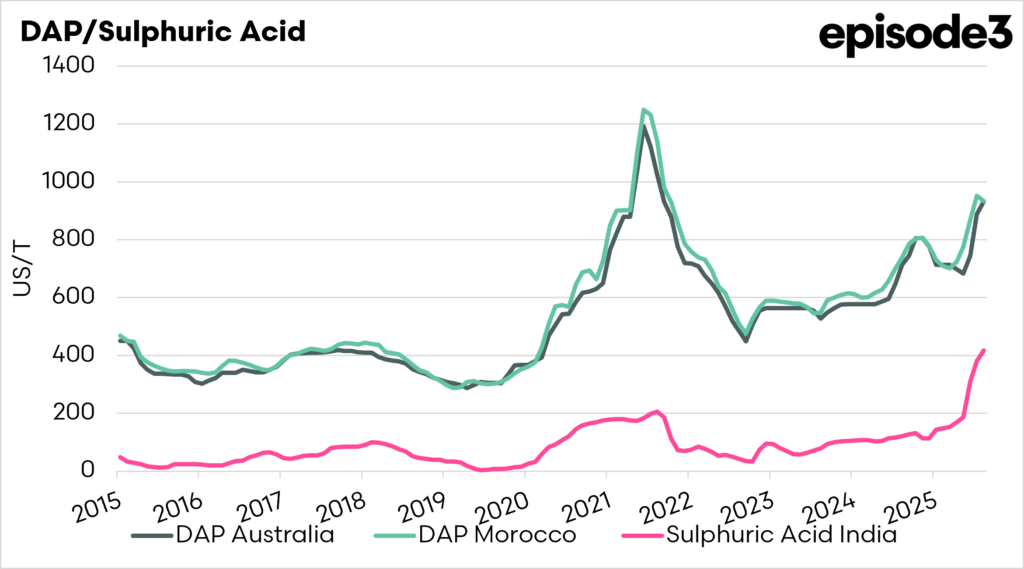

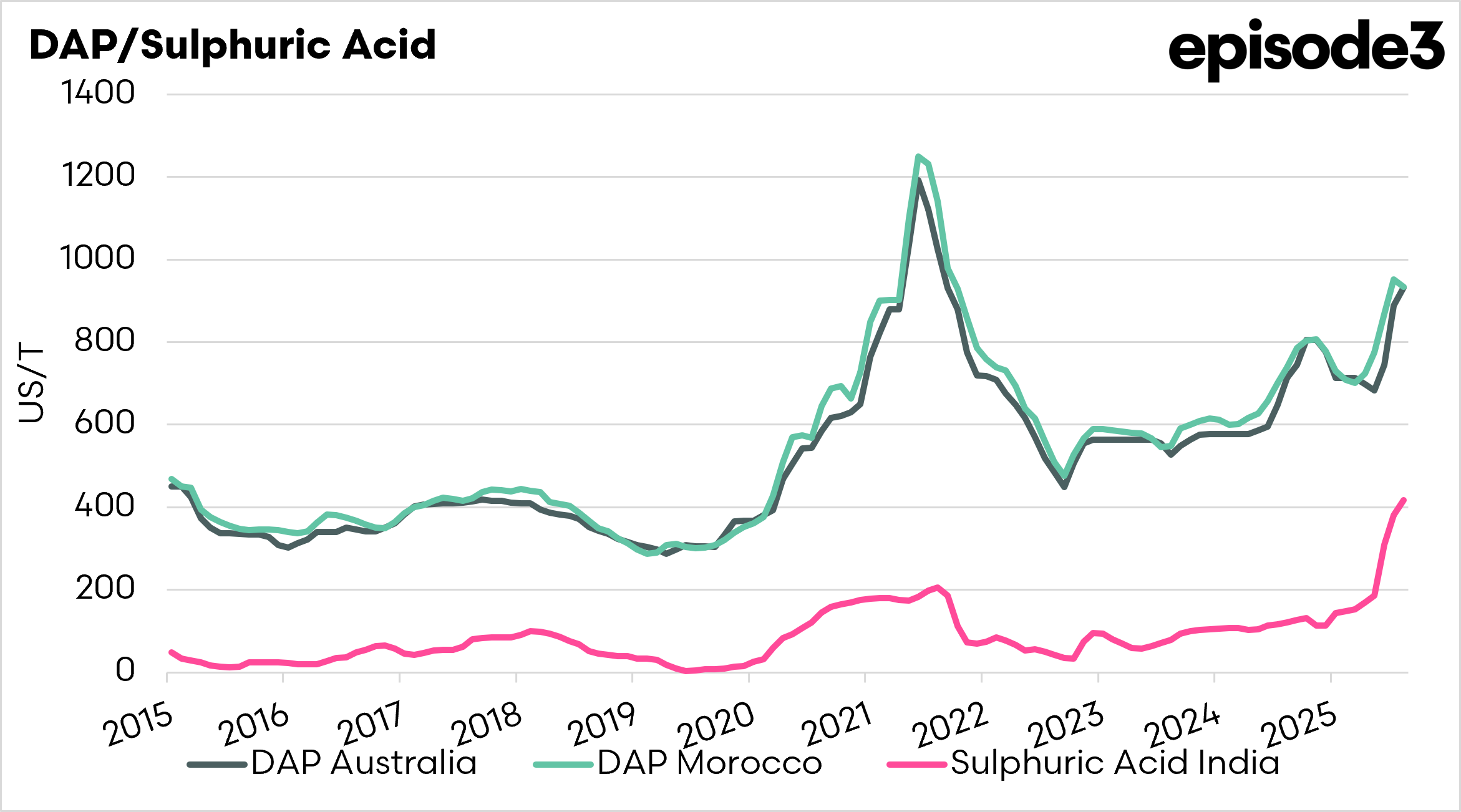

Australian growers watching MAP and DAP prices may need to keep one eye on a market they rarely talk about: sulphuric acid.

The price chart shows DAP values in Australia and Morocco back to 2015, alongside sulphuric acid (India). Over the long term, DAP Australia and DAP Morocco move in close tandem, as you would expect from two finished phosphate fertiliser benchmarks. Sulphuric acid does not move in perfect lockstep with DAP, but it is an important upstream signal. When acid prices lift sharply, it points to stress building further back in the phosphate production chain.

That matters because sulphuric acid is a key input in the manufacture of phosphate fertilisers. Phosphate rock is treated with sulphuric acid to produce phosphoric acid, which is then used to make MAP and DAP. Farmers do not need to buy sulphuric acid themselves to be exposed to the problem. If acid is unavailable, too expensive, or delayed by shipping disruptions, phosphate fertiliser producers may be forced to slow production, restrict offers, or raise prices.

The current market is a good example of why these matter. DAP prices are high, but sulphuric acid has moved even more aggressively. In the latest data, DAP Australia and DAP Morocco have climbed strongly from the levels seen through 2024 and 2025, but sulphuric acid has surged to levels well beyond those seen during the 2021-22 fertiliser spike. That suggests the risk is not just finished fertiliser being expensive today. The bigger concern is that an upstream supply squeeze could keep MAP and DAP replacement costs elevated for longer.

Fertiliser is the highest variable cost in broadacre cropping, and growers are again being asked to make purchasing decisions in a volatile global market. Australia is largely a price taker in phosphate fertiliser, so disruptions in sulphur, sulphuric acid or phosphoric acid can quickly flow through to local replacement costs.

There is a pathway to relief. If sulphur flows from the Middle East return to more normal levels once the conflict settles, that should help ease pressure on sulphuric acid availability and, in time, on phosphate fertiliser production. But that is a big “if”. The ceasefire remains fragile and has already looked stop-start. Until cargoes are moving reliably again, the acid squeeze remains a genuine risk for MAP and DAP prices.

The good thing is that we do have some time. This current crisis happened after the bulk of the DAP and MAP requirements were in place for Australia; it is a concern for next year if the conflict isn’t resolved. The chart shows DAP is already expensive. Sulphuric acid suggests the supply chain behind it is still under stress.