Global cattle pricing update

Get short video updates on your phone

For quicker updates as markets move, follow @themeatwatcher on Instagram. I regularly post short summaries and charts breaking down what’s happening in meat proteins and broader ag markets so you can stay across the key moves without having to read through pages of analysis. If markets are moving quickly, that’s usually where the updates will land first.

Global cattle price update - March 2026

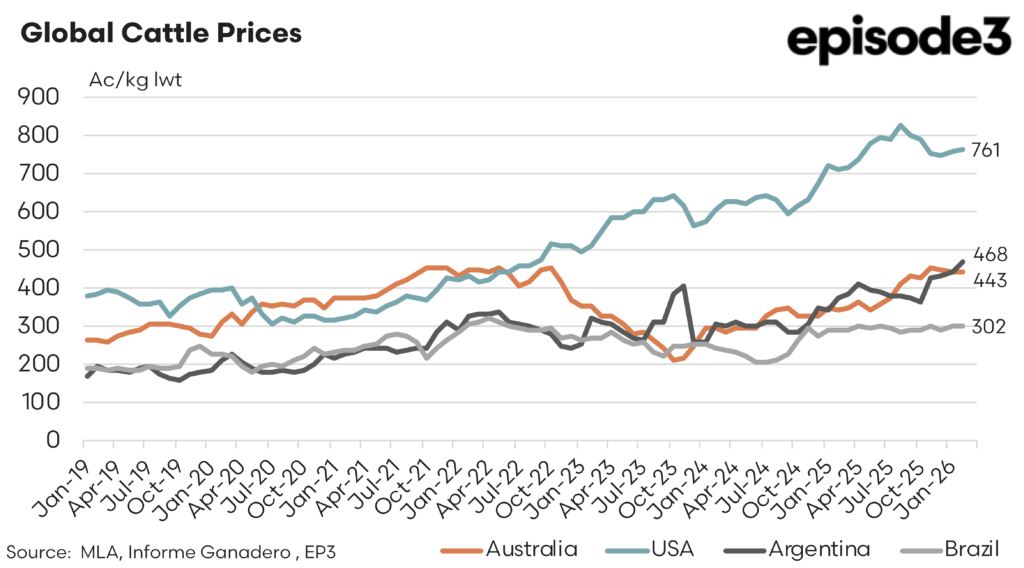

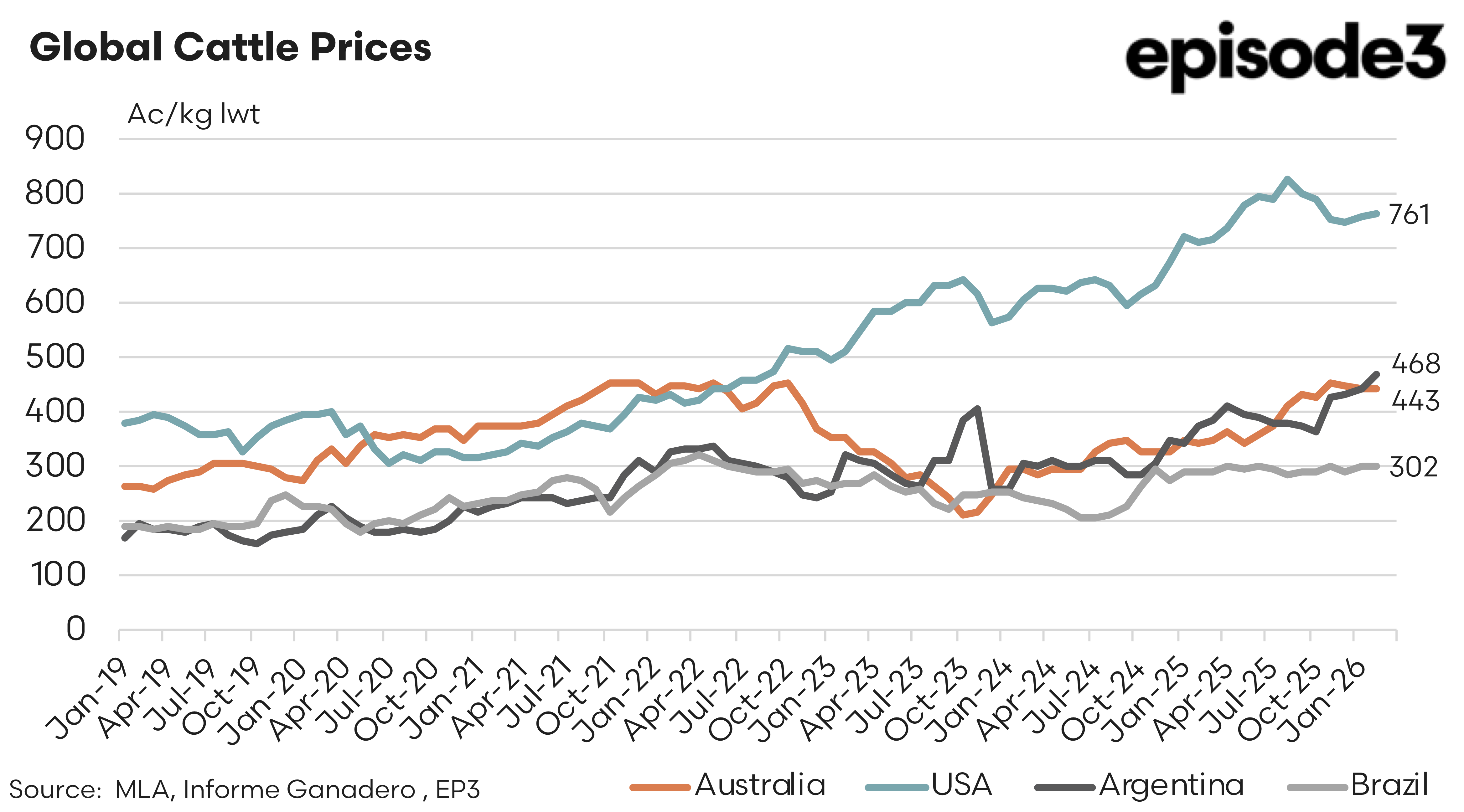

Recent analysis of global cattle prices highlights the widening divergence between major beef producing nations, with equivalent heavy steer values across Australia, the United States, Argentina and Brazil converted into Australian dollars per kilogram live weight to enable a direct comparison.

The chart provides a clear view of how each market is currently positioned relative to one another, illustrating both the variation in underlying supply cycles and the changing competitiveness of key exporting countries.

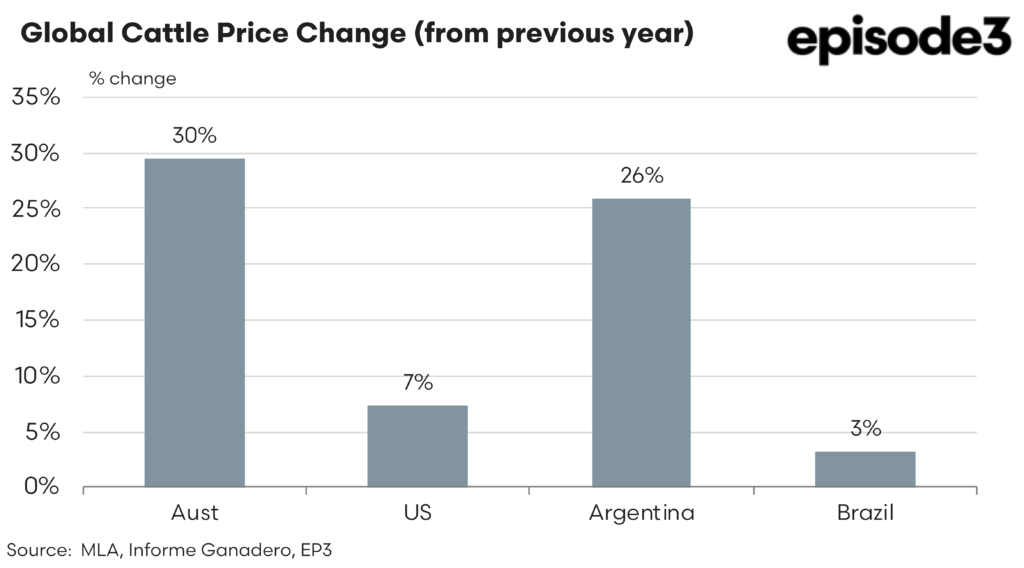

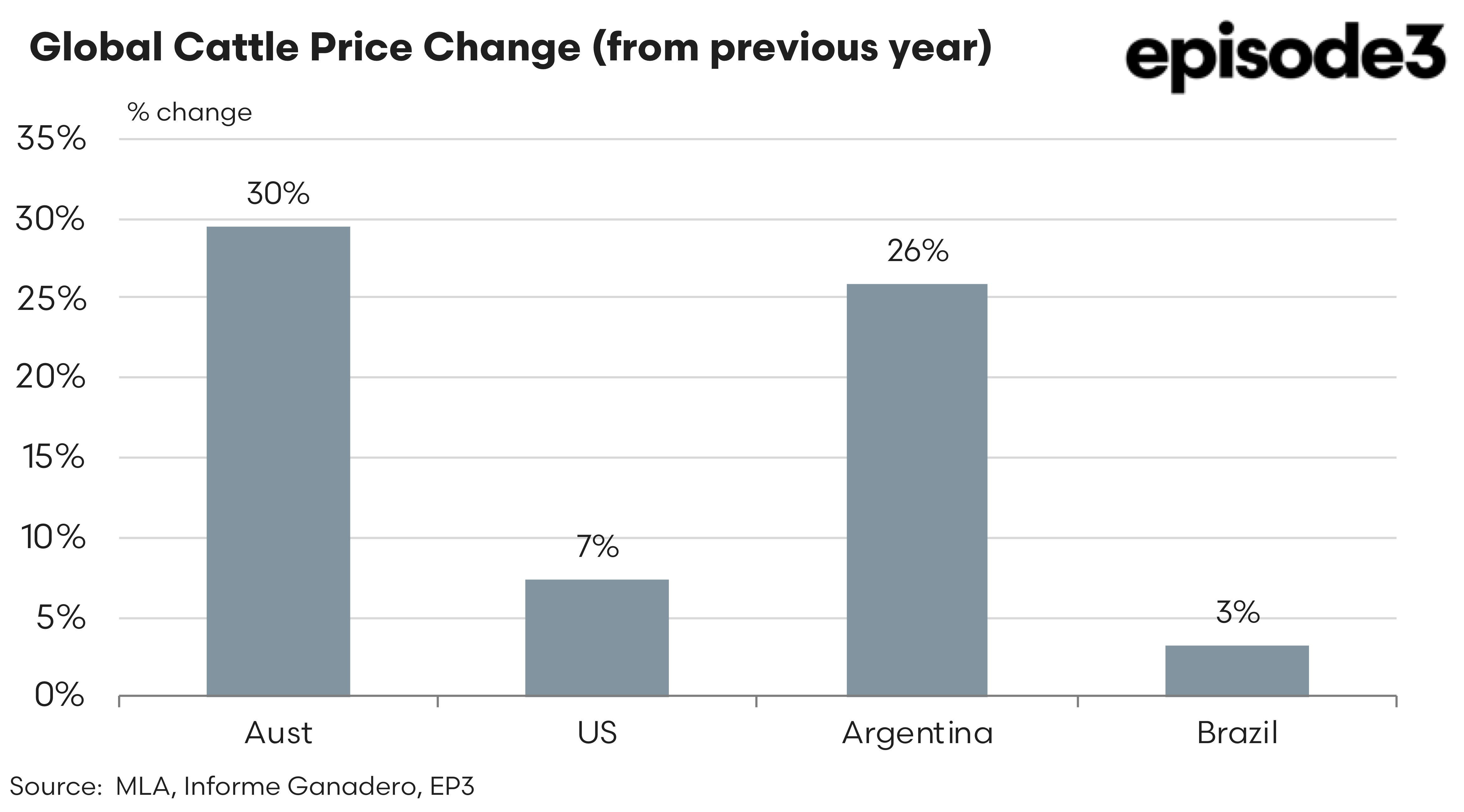

The United States remains the clear price leader. Heavy steer values have lifted steadily since early 2024 and now sit around 761¢/kg live weight. This represents the continuation of a multi-year rally driven by tight cattle supplies following aggressive herd liquidation during drought conditions earlier in the decade. The US herd remains historically low and slaughter availability constrained, which has kept domestic cattle prices elevated despite softer consumer demand signals at times. Over the past year alone, US cattle prices have risen approximately 7 percent, a modest annual increase compared with earlier gains but still enough to maintain a substantial premium over competing exporters.

Australian heavy steer values now sit near 443¢/kg live weight, marking an annual increase of roughly 30 percent. This strong rebound reflects improved processor competition and solid export demand that has remained relatively supportive for prices, while still remaining at levels that are competitive internationally.

Argentina has also recorded a significant lift in pricing over the past year, with heavy steer values climbing to approximately 468¢/kg live weight, up around 26 percent year on year. Currency adjustments and domestic economic reforms have played a major role in reshaping Argentine cattle pricing when expressed in Australian dollar terms. While volatility remains a feature of that market, the overall trend has been upward as inflationary pressures and policy shifts flow through production costs and farm gate pricing. Argentina now sits slightly above Australia in absolute price terms, a reversal from periods where its cattle traded at a deeper discount.

Brazil continues to occupy the lower end of the global pricing spectrum. Heavy steer values are currently around 302¢/kg live weight, rising only about 3 percent over the past year. Brazil’s large cattle herd, ongoing productivity gains and relatively lower cost production base continue to anchor prices below those seen in other major exporters. Stable supply growth and a competitive currency have reinforced Brazil’s role as the global price setter for commodity beef markets.

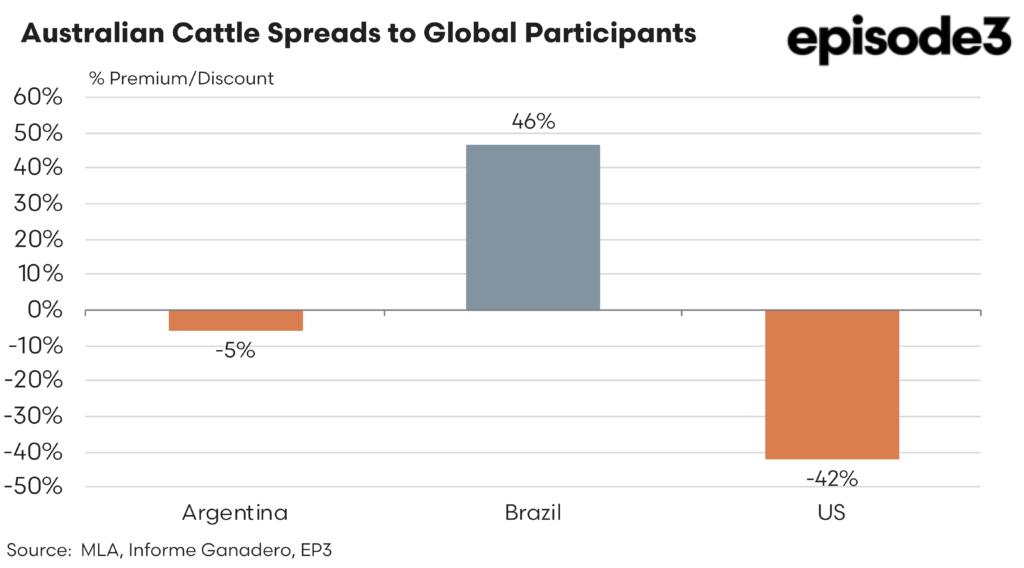

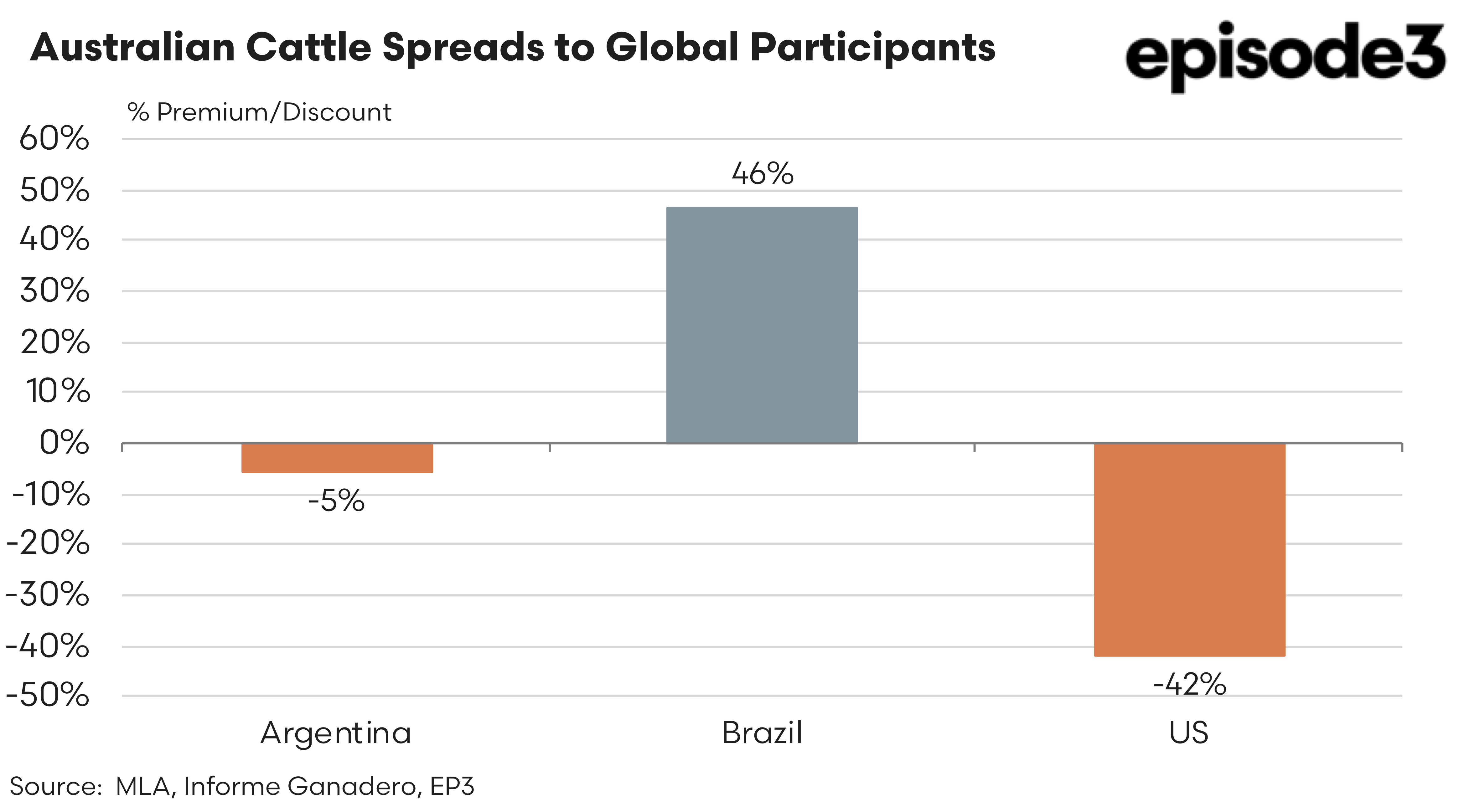

These differing price paths translate directly into the current premium and discount structure between exporting nations. Australian cattle are trading at roughly a 46 percent discount to US cattle, underlining the extraordinary tightness of American supply. Against Argentina, Australian cattle sit near parity but still hold a small discount of around 5 percent. In contrast, Australian cattle command a significant premium of approximately 46 percent over Brazilian cattle, reflecting higher production costs and differing market positioning.

For global beef trade, these relationships matter as much as absolute price direction. Australia is still competitively priced relative to the US, which is our main competitor on key export markets like Japan, China and South Korea. How long that positioning holds will depend largely on seasonal conditions, herd dynamics and whether the US begins a meaningful rebuild that eventually narrows the large cattle price discount that Australia currently enjoys.