Global cattle pricing update July 2026

Get short video updates on your phone

For quicker updates as markets move, follow @themeatwatcher on Instagram. I regularly post short summaries and charts breaking down what’s happening in meat proteins and broader ag markets so you can stay across the key moves without having to read through pages of analysis. If markets are moving quickly, that’s usually where the updates will land first.

Global cattle price update - July 2026

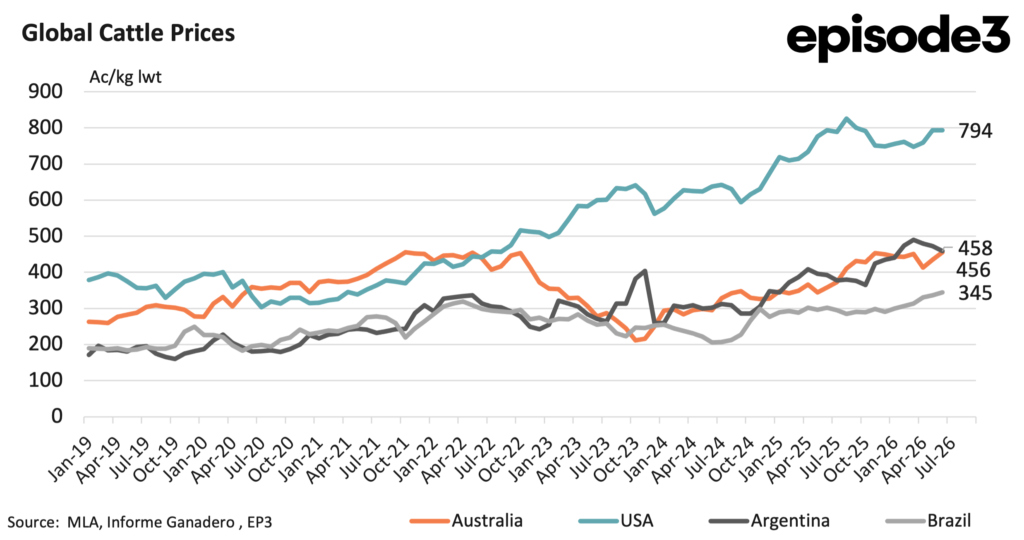

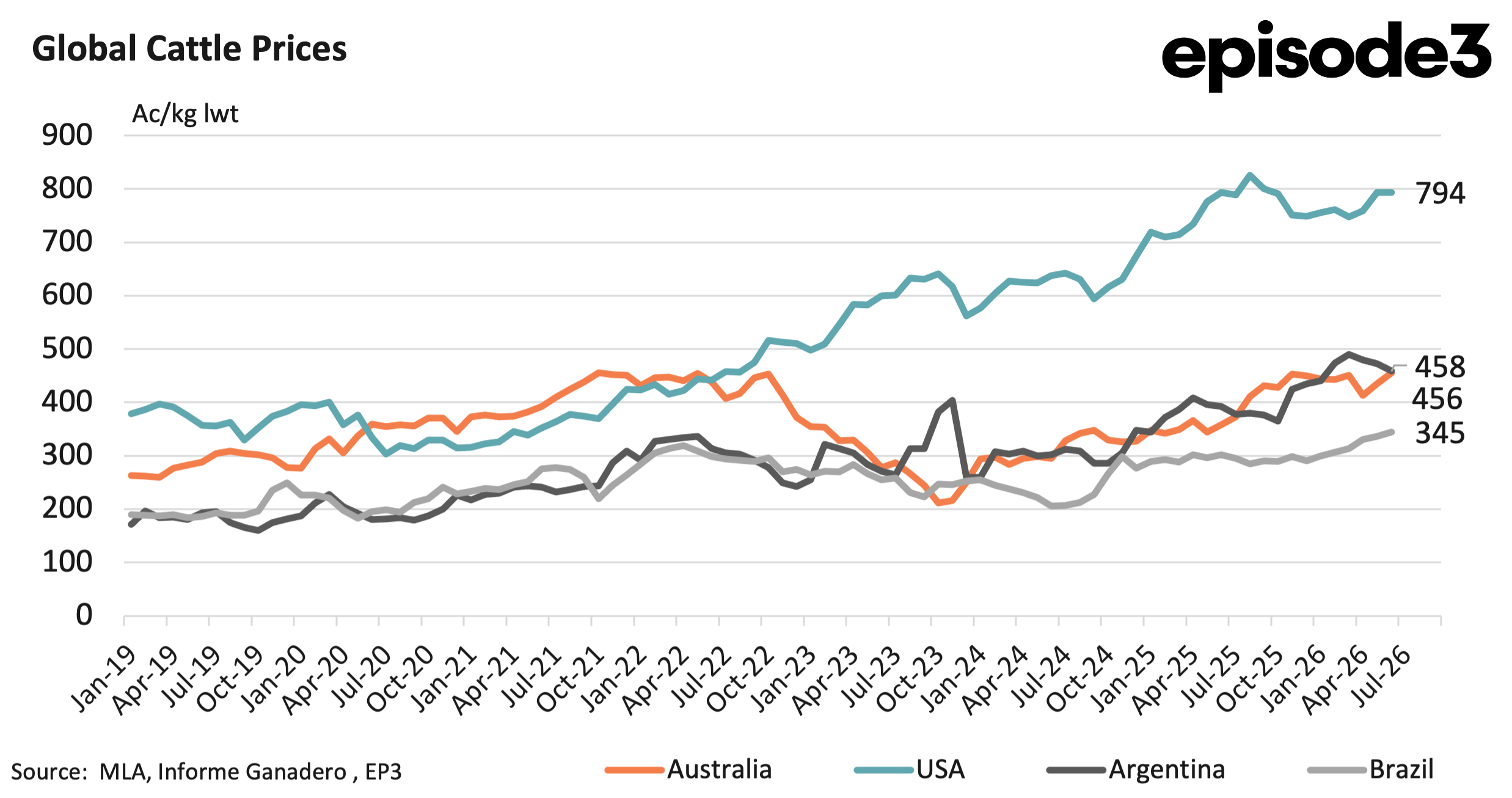

Global cattle prices continued to firm through June, but the bigger story is now shifting from livestock values alone to market access and tariff pressure. The latest EP3 global cattle price comparison shows Australian heavy steer prices lifting to 456Ac/kg lwt. That places Australia just under Argentina, well below the United States, and still clearly above Brazil.

Argentina is sitting at 458Ac/kg lwt in June. The US remained the higher priced option at 794Ac/kg lwt. Brazil lifted to 345Ac/kg lwt, but remains the cheapest of the four markets in the comparison.

For Australia, the June result continues the recovery seen through May. Australian heavy steer prices are now 32pc above Brazil, 43pc below the US, and only just under Argentina. That positioning is important as Australia remains materially cheaper than the US, and that continues to matter in key export markets where the two countries compete directly.

The US cattle market remains in a very different position to the rest of the world. At 794Ac/kg lwt, US heavy steer values are still almost twice Brazilian levels and well above both Australia and Argentina. The high US price structure reflects the ongoing tight supply situation after years of herd liquidation. That tightness continues to support cattle prices, but it also places pressure on US beef competitiveness.

For Australian exporters, this remains a useful buffer. Even as Australian cattle prices rise, the gap to the US remains large enough to keep Australian beef relatively attractive in a range of premium and mid-tier export channels.

Argentina is now effectively level with Australia. At 458Ac/kg lwt, Argentine cattle are only slightly above Australian heavy steer values. That suggests the relative price advantage Australia held against Argentina has largely narrowed. Argentina remains a key market to watch, particularly when policy settings, currency movements and export conditions allow it to push more aggressively into global beef trade.

Brazil remains the low-cost competitor and at 345Ac/kg lwt, Brazil is sitting 32pc below Australian levels. That price gap continues to explain Brazil’s strength in price sensitive markets, particularly where buyers are more focused on cost than brand, provenance or specification.

The challenge for Australia is that the price story is now being complicated by safeguard tariffs in North Asia. The Chinese safeguard was triggered earlier in June, meaning Australian beef entering China now attracts a 55pc tariff. That is a substantial increase in landed cost and will make trade into China more difficult through the safeguard period.

The South Korean safeguard is also now sitting around 90pc utilised, meaning it is likely to be triggered into July. Once that occurs, which is likely during July, the tariff on Australian beef into South Korea will rise from 5pc to 24pc. That increase is likely to see some softening in South Korean demand until the quota resets later in the year, most likely around November or December.

However, it does not mean Australian beef will stop flowing into South Korea. The key reason is that US product remains expensive. With US cattle prices still sitting at 794Ac/kg lwt and supply still tight, the competitiveness of US beef remains problematic, even with Australia facing a higher tariff.

This is where the global cattle price comparison becomes especially useful. Tariffs matter, and the increase into South Korea will hurt Australian competitiveness at the margin. But the underlying cost base of competing suppliers also matters. If US beef remains constrained by high cattle prices and tight supply, Australian beef can still hold a place in the South Korean market, even under a less favourable tariff setting.

For Australian producers, June was a positive month on the price front. Heavy steer values continued to lift and are now nearly level with Argentina. For exporters, the picture is more complicated. Australia remains well priced against the US, but safeguard tariffs into China and South Korea will test demand through the second half of the year.

The June update therefore shows two things at once. Australian cattle prices are improving. But the trade environment is becoming more difficult. The global pecking order remains intact, with the US at the top, Brazil at the bottom, and Australia sitting in the middle. The question now is whether Australia can keep lifting cattle prices while still holding export competitiveness as tariff pressure builds.