Global lamb pricing update

Lamb pricing update - March 2026

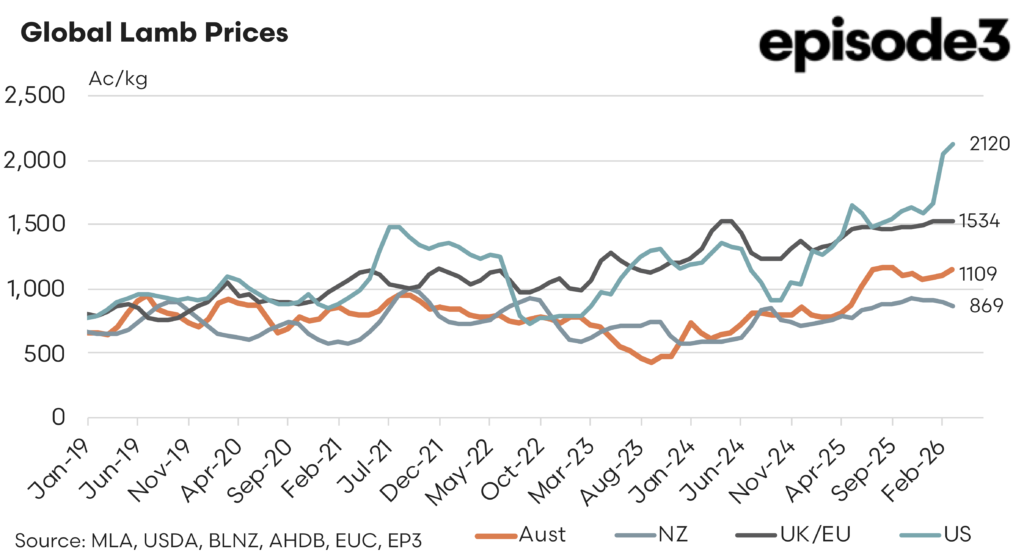

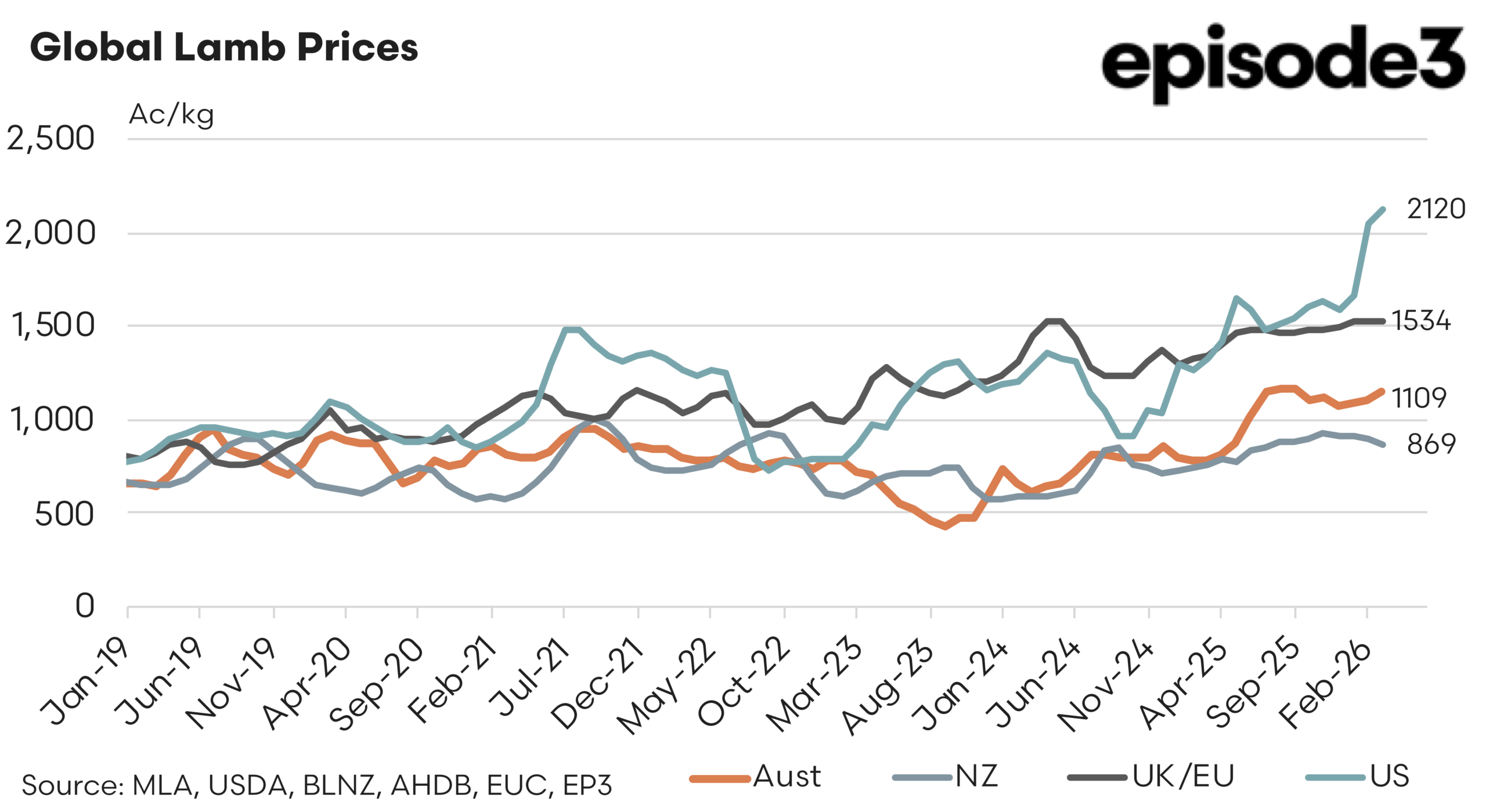

Global lamb markets have moved sharply over the past year, but not in unison, and the divergence between regions is now as important as the direction itself. Australian lamb prices have lifted strongly, rising 47 percent over the past twelve months, reflecting a combination of tightening supply, improved seasonal confidence, and stronger export demand across key markets.

As at March 2026, Australian lamb is trading at approximately 1109 A¢/kg, placing it firmly above recent historical averages but still well within the global pack. That lift has been meaningful, but it has not been unique. Across the Northern Hemisphere, UK and EU lamb prices have also trended higher, though at a more modest pace, gaining around 14pc over the same period.

Current UK and EU prices sit at around 1534 A¢/kg in March 2026, maintaining their position as one of the highest-priced lamb markets globally. New Zealand has followed a similar trajectory, also lifting by roughly 14pc, with prices supported by steady export demand but constrained by a more consistent supply profile. New Zealand lamb is currently trading at approximately 869 A¢/kg, reinforcing its role as a competitive export supplier relative to Australia.

The standout has been the United States, where lamb prices have surged 61pc over the past year, driven by a combination of reduced domestic production, strong consumer demand, and a structural reliance on imports that amplifies price movements when supply tightens.As at March 2026, US lamb prices are sitting near 2120 A¢/kg, well above all other major producing regions. This divergence in price momentum is now clearly visible in global spreads.

Australia, despite its strong rally, is sitting in the middle of the global pricing stack rather than leading it.

At present, Australian lamb is trading at a 32pc premium to New Zealand, highlighting the tighter domestic supply position and stronger demand pull into Australian product.That premium reflects both structural and cyclical factors, including flock dynamics, processor competition, and export market positioning.

At the same time, Australia remains at a 24pc discount to the UK and EU market. This gap has been relatively persistent, and it continues to reflect differences in market structure, including domestic consumption patterns, import protection, and shorter supply chains across Europe.

It also reinforces the role of the European market as a higher-priced, more insulated system compared to export-oriented suppliers like Australia and New Zealand.

The most striking differential, however, is against the United States. Australian lamb is currently trading at a 46pc discount to US levels, underlining just how aggressively the US market has moved.This spread is not simply a reflection of quality differences or product mix. It is a function of a structurally tight US supply base, strong retail demand, and the country’s dependence on imported lamb, which effectively imports global price volatility and then amplifies it.

From a global perspective, what we are seeing is not a single market moving higher, but a fragmentation of pricing signals. Australia has lifted strongly, but remains competitive in global terms. New Zealand has moved higher, but more gradually, maintaining its position as a lower-priced export supplier.