Global lamb pricing update May 2026

Lamb pricing update - May 2026

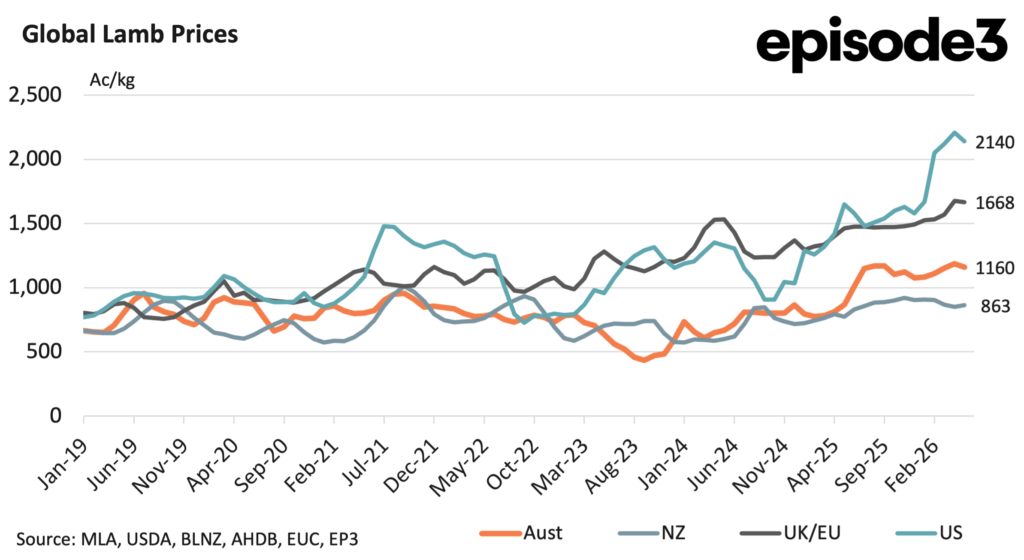

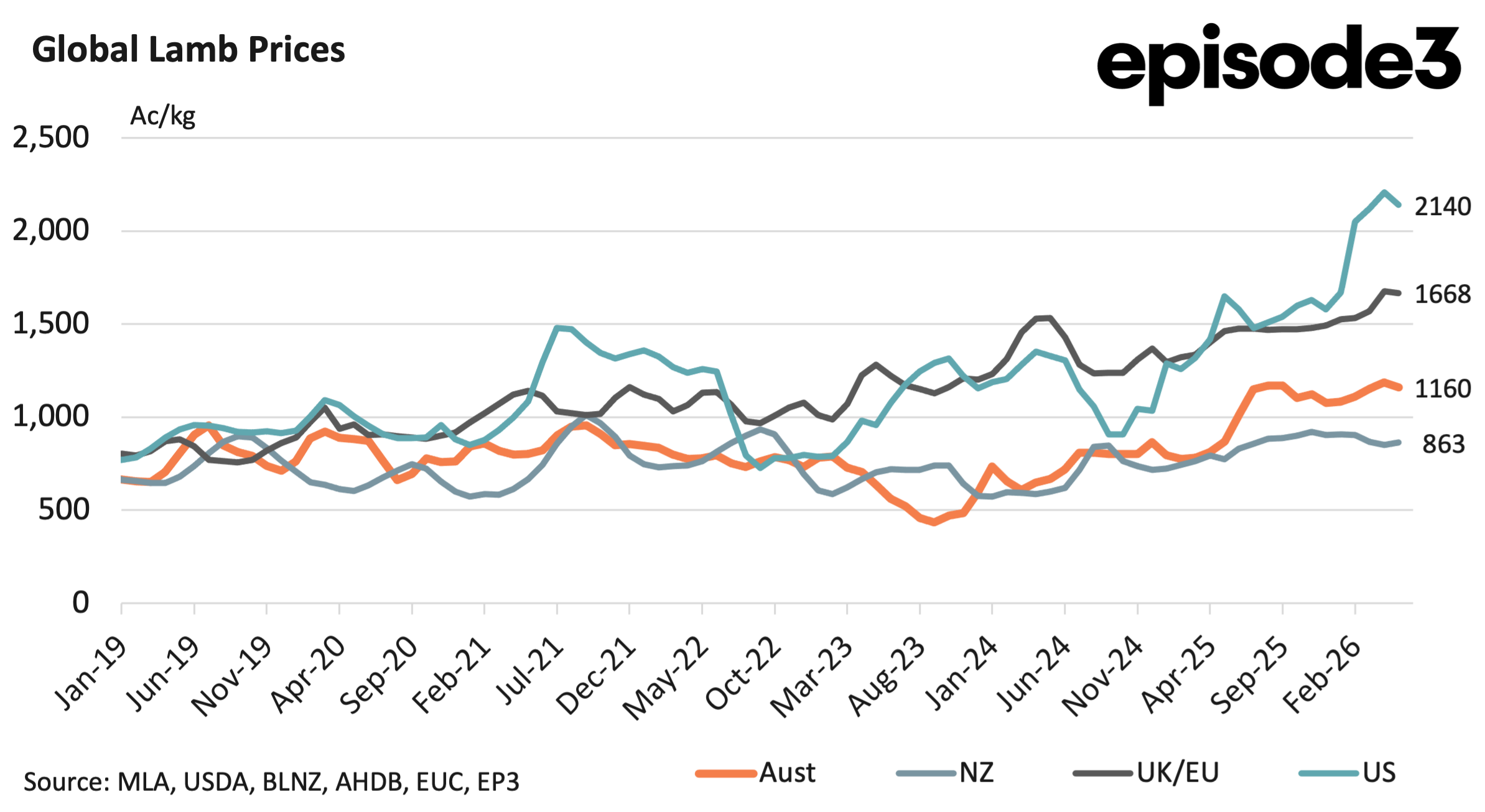

Global lamb markets have continued to diverge sharply since the beginning of 2026, with Northern Hemisphere markets extending their rally while Oceania remains comparatively subdued. The most notable development since March has been the continued strength in both the US and European markets, which have pushed further away from Australian and New Zealand pricing levels.

US lamb prices lifted from around 2050 A¢/kg in February to approximately 2120 A¢/kg during March before pushing higher again to roughly 2210 A¢/kg in April.While the market eased slightly during May to around 2140 A¢/kg, US values remain historically elevated and nearly double New Zealand pricing levels. The US market is currently trading at roughly a 46pc premium to Australian lamb values, highlighting the extreme tightness in US domestic supply and the country’s heavy reliance on imported lamb.

Europe has also strengthened materially during the same period. EU heavy lamb prices lifted from approximately 1544 A¢/kg during February to around 1628 A¢/kg in March before surging to 1732 A¢/kg during April. The market softened only marginally during May to approximately 1725 A¢/kg. That leaves EU lamb pricing around 33pc above Australian levels.

The UK market has followed a similar trend. British lamb prices lifted from approximately 1523 A¢/kg in February to around 1511 A¢/kg in March before rallying strongly to approximately 1620 A¢/kg during April. Prices eased only slightly in May to roughly 1610 A¢/kg.

The broader UK/EU benchmark therefore lifted from around 1534 A¢/kg in February to approximately 1676 A¢/kg during April before easing modestly to around 1668 A¢/kg in May. That leaves Australian lamb trading at around a 30pc discount to the broader UK and EU complex.

In contrast, New Zealand pricing has remained comparatively soft through autumn. NZ lamb values eased from around 903 A¢/kg during February to approximately 869 A¢/kg in March and then softened further to around 850 A¢/kg during April before recovering slightly to approximately 863 A¢/kg during May. That relatively weak performance has widened the spread between Australia and New Zealand considerably. Australian lamb was trading at a 23pc premium to NZ values during February.

By April that premium had widened to around 40pc before easing slightly back to approximately 34pc during May. Australia itself has continued to strengthen steadily during 2026. Australian lamb values lifted from around 1109 A¢/kg during February to approximately 1153 A¢/kg in March before rising further to around 1188 A¢/kg during April.

The market softened marginally during May to approximately 1160 A¢/kg but remains well above year earlier levels. Importantly, Australia now appears to be occupying a middle position within the global lamb market structure. New Zealand remains the lowest priced major exporter globally.

However, Australia remains well below the pricing levels currently prevailing in Europe and the United States. That pricing structure continues to reinforce Australia’s export competitiveness. Despite the strong rally in Australian lamb prices over the past year, Australian product remains attractively priced relative to Northern Hemisphere markets.

The US market continues to reflect structural supply shortages and extremely strong consumer pricing. Europe remains elevated due to tighter regional supply and resilient domestic demand. Meanwhile Oceania continues to operate as the globally competitive export supply base.

For Australian producers, the current market structure remains broadly supportive. Australian prices are high enough to significantly improve producer returns compared to the lows of 2023 and early 2024, while remaining competitive into global export channels. That balance is likely to remain critical as the global protein market moves through the second half of 2026.