Lower procurement costs drive beef processor recovery

Beef Processor Trading Conditions - April 2026 update

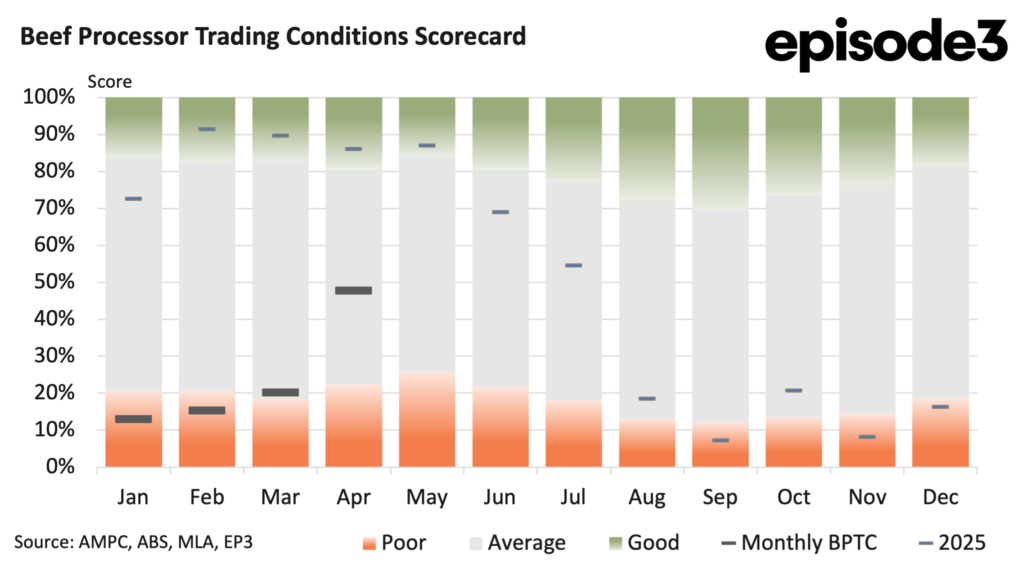

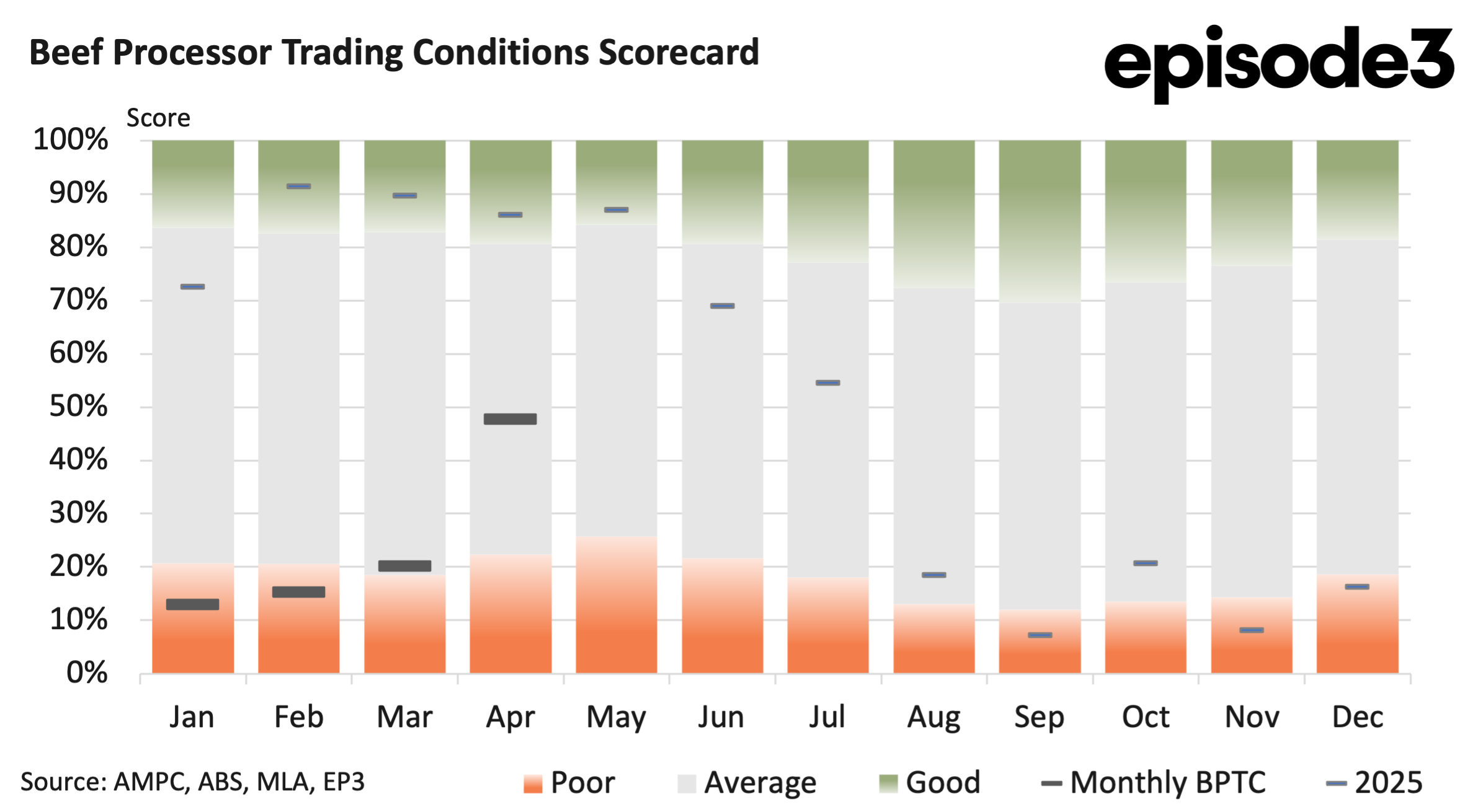

Beef processor trading conditions improved sharply through April 2026, with the Beef Processor Trading Conditions index lifting from 20pc in March to 48pc. The improvement represents the strongest monthly result recorded so far this year and lifts the annual average for 2026 to 24pc. Despite the sizeable recovery, the broader comparison remains challenging.

At the end of April last year, the BPTC annual average stood at 85pc. While processor margins have improved during recent months, they remain well below the exceptionally strong conditions experienced throughout the first part of 2025. The April improvement was largely driven by lower livestock procurement costs rather than stronger export demand.

Several public holidays during the month, including Easter and ANZAC Day, reduced processing capacity across the industry and disrupted normal cattle procurement patterns. The shorter operating weeks contributed to softer saleyard competition and lower livestock prices, providing processors with some welcome relief on their largest input cost.

Heavy steer prices declined by 8pc during April, meanwhile young cattle eased even further, falling 9.5pc over the month. Processor cow prices recorded the largest correction, declining by 14pc. These movements represent a meaningful improvement from a processor’s perspective.

Livestock purchases account for the largest share of processing costs, so any easing in cattle prices has a direct and immediate impact on operating margins. After a prolonged period of elevated procurement costs, April finally provided processors with some breathing room. However, the improvement in processor conditions cannot be attributed solely to lower cattle prices. The relationship between livestock values and export returns remains the critical determinant of processor profitability.

While cattle became cheaper to purchase, export markets generally offered little additional support. The United States continued to underpin Australian beef exports during April. Export values held steady at an average of almost $13.70/kg, maintaining the historically high returns that have characterised the market over recent months. Continued tight cattle supplies in North America and strong import demand have helped keep the United States as Australia’s highest value export destination.

China also recorded a modest improvement during April, with export values increasing by 1.1pc. While relatively small in monthly terms, the rise reinforces the resilience of demand into one of Australia’s most important beef markets despite ongoing economic uncertainty.

South Korea also edged higher, gaining 0.6pc over the month. The improvement was modest but nevertheless contributed to stable export performance across North Asia. Japan was the only one of the four major export destinations to move lower during April with export values slipping by 2pc, partially offsetting the gains recorded elsewhere.

When considered collectively, the result was a remarkably stable export market. Average export values across Australia’s four largest beef export destinations were effectively unchanged from March. This highlights an important feature of the April BPTC result. The improvement in processor margins was not driven by stronger revenue. Instead, it reflected lower cattle procurement costs while export returns remained largely stable.

Domestic market conditions were equally steady. Retail beef prices were unchanged from March, suggesting consumers have yet to experience any meaningful shift in pricing despite the recent volatility in livestock markets. The stability in retail pricing also reinforces the lag that often exists between movements in livestock markets and prices paid by consumers.

Changes in cattle values are not immediately reflected at the supermarket shelf, particularly when processors and retailers continue to absorb higher operating costs elsewhere in the supply chain. The April result therefore illustrates how quickly processor margins can improve when procurement costs ease, even if export values remain largely unchanged.

After several months where higher livestock prices compressed margins, processors have benefited from a temporary improvement in the spread between cattle costs and beef sale prices. Even so, the industry remains well below the profitability levels recorded a year ago. The annual average of 24pc sits dramatically below the 85pc recorded at the same point in 2025. That comparison demonstrates just how exceptional processor conditions were last year and how much the operating environment has changed.

There are already signs that April’s improvement may prove temporary. Seasonal rainfall across several key cattle producing regions has encouraged producers to hold cattle for longer, reducing immediate marketings. As processing plants returned to normal operating schedules following the Easter disruptions, competition for available cattle strengthened noticeably.

Recent market indicators have already shown cattle prices beginning to recover across several categories. If that trend continues, the improvement in processor margins recorded during April may prove difficult to sustain through the second quarter. The coming months are therefore likely to depend on whether cattle availability continues to improve or whether seasonal conditions once again tighten supply.

Export markets remain broadly supportive, but they are no longer providing the strong monthly gains that helped offset rising procurement costs during previous periods. For now, April represents a welcome improvement for Australia’s processing sector.