Processors chase cattle as yardings turn uneven

Market Morsel

Beef processors have pushed hard into the market through March, but the lift in activity is telling a more complicated story than a simple increase in cattle supply. The latest yarding and processing indices show a market that is shifting, fragmenting, and becoming increasingly uneven across regions.

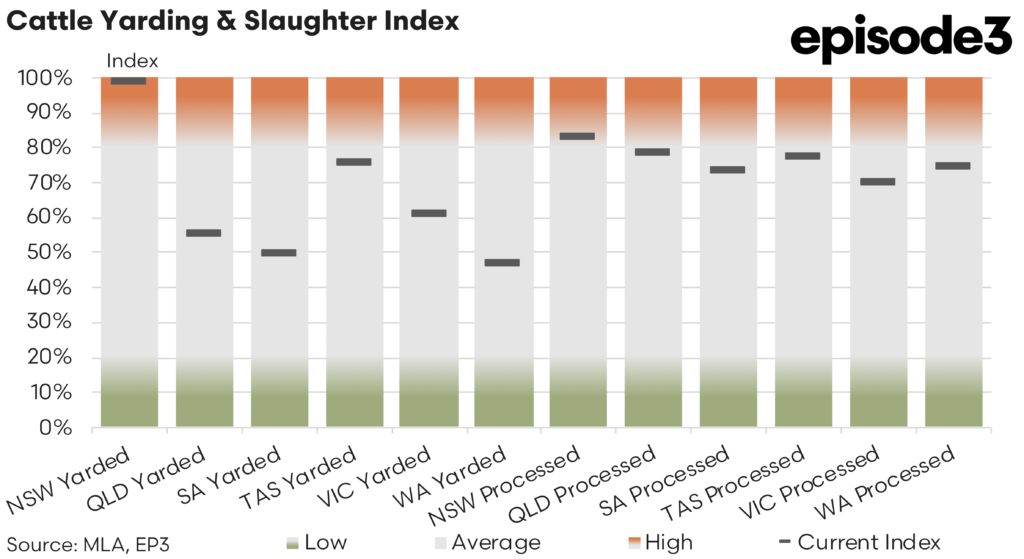

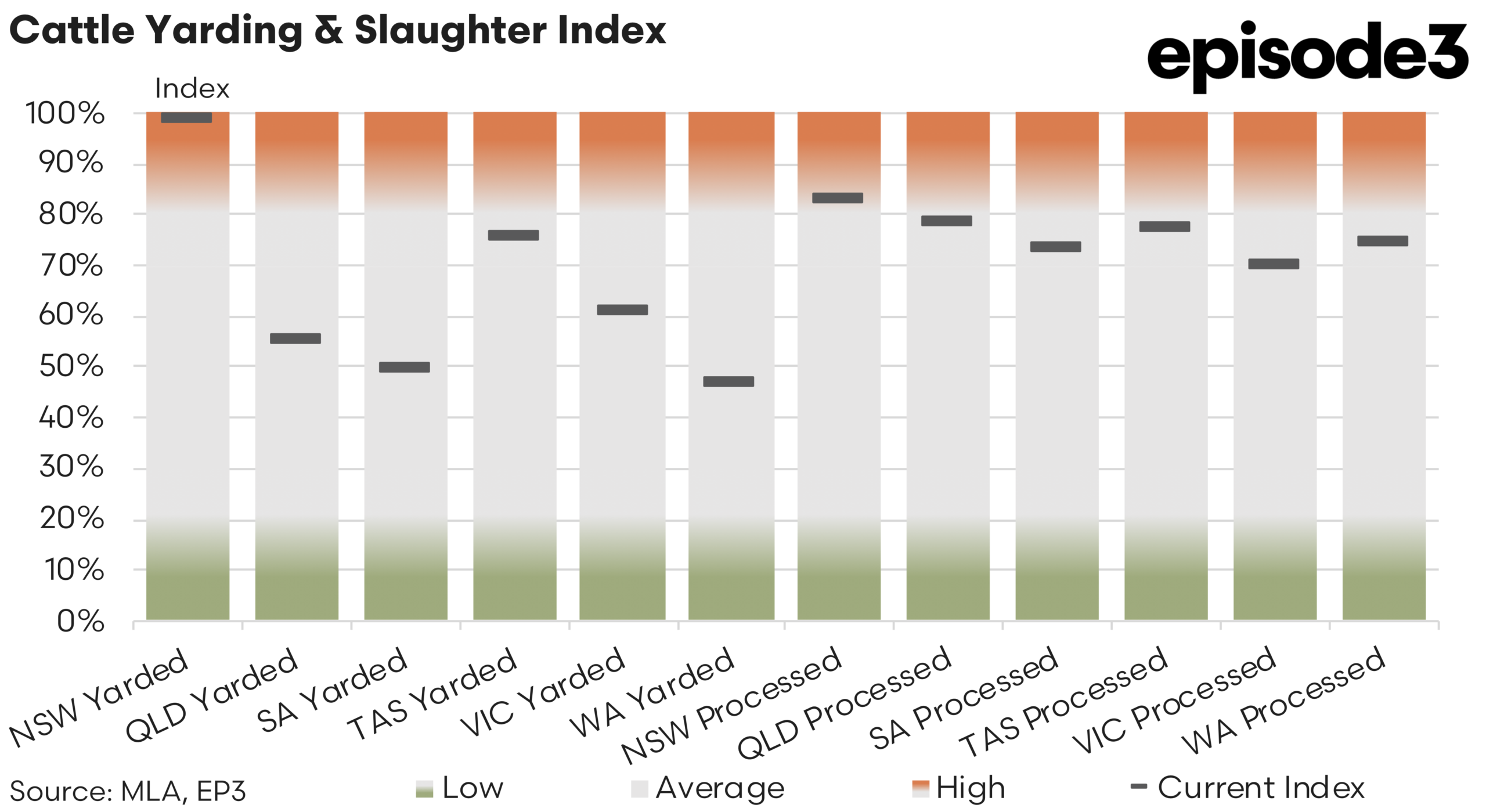

In New South Wales, yardings lifted from 95 percent to 99pc, pointing to a clear increase in cattle coming forward. Queensland followed a similar path, rising from 45pc to 55pc, signalling improving but still moderate supply. This lift in the eastern states has provided processors with the throughput needed to increase kills.

At the same time, the southern and western states told a different story. Victoria yardings fell from 76pc to 61pc, South Australia dropped from 78pc to 50pc, and Western Australia declined from 69pc to 47pc. This is not a national surge in cattle availability, it is a redistribution of supply, concentrated in the north and east. Processors have responded accordingly.

Processing activity in New South Wales surged from 53pc to 83pc, representing a significant ramp-up in throughput. Queensland also lifted from 68pc to 79pc, reinforcing the trend of increased activity where cattle are available.

Elsewhere, the picture softened. Processing in South Australia fell from 89pc to 74pc, Victoria eased from 76pc to 70pc, and Western Australia dropped from 86pc to 74pc.

This alignment between yardings and processing highlights a key feature of the current market. Processors are not operating uniformly across the country. They are chasing cattle where it exists and pulling back where it does not.

However, the shift in flows is only part of the story. External pressures are also beginning to shape how cattle move and how processors behave. Fuel availability and logistics constraints are starting to interfere with normal market function. Transport costs and uncertainty are limiting the efficient movement of stock, particularly across longer distances. This is likely contributing to the tightening seen in some regions, even as supply improves elsewhere. At the same time, trade dynamics are adding another layer of complexity.

The approach of export quota limits into key markets is encouraging processors to maximise throughput while conditions allow. This creates a short term incentive to lift kills, even in the face of emerging constraints. The result is a market that appears active, but not necessarily comfortable. Processors are pushing hard, but they are doing so within a narrowing window of opportunity.

The price signals over the past four weeks reinforce this interpretation. Processor cow prices have fallen sharply, down 61 cents over the last month. This is the clearest indication that supply has lifted meaningfully in the manufacturing beef channel. Cows are typically the first category to respond when availability increases, and that pattern is playing out here. Heavy steer prices have also declined, falling 65 cents over the same period. This suggests that finished cattle supply has improved too. There remains a level of competition for well finished stock, even as overall availability increases.

Producers are becoming more cautious, likely reflecting global uncertainty and rising cost pressures. This is consistent with the broader shift in slaughter patterns. The increase in throughput has been supported in part by greater cow availability, which has allowed processors to lift kills quickly. However, this does not equate to a fully supplied market. Yarding supply remains uneven, both geographically and by category.

The eastern states are carrying the bulk of the increase, while other regions remain constrained. At the same time, demand signals are becoming more complex, shaped by both export conditions and domestic factors. The combination of rising throughput, falling prices, and external constraints points to a market in transition. It is moving away from the extreme tightness seen previously, but it has not shifted into oversupply. Instead, the industry is entering a more volatile phase.

Supply is improving, but not evenly. Demand remains supportive, but is increasingly influenced by policy and logistics. Processor behaviour is active, but driven by opportunity rather than comfort. The net effect is a market that is harder to read and more sensitive to disruption. Small changes in supply, logistics, or trade settings are now having a larger impact on pricing and flows.