Processors return, but cattle numbers don’t

Market Morsel

The cattle market has taken another turn through May, with processor demand strengthening noticeably just as supply in several key regions begins to tighten. The latest Cattle Yarding and Slaughter Index figures suggest the Easter disruption that dominated April has now largely passed, with processors returning to much higher operating rates across the country. The most significant shift during May has occurred on the processing side of the ledger.

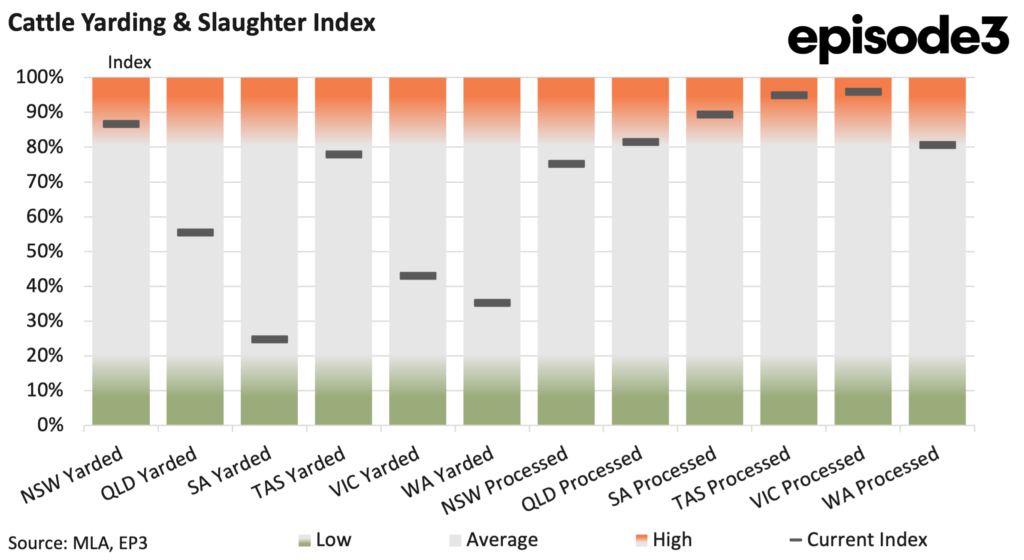

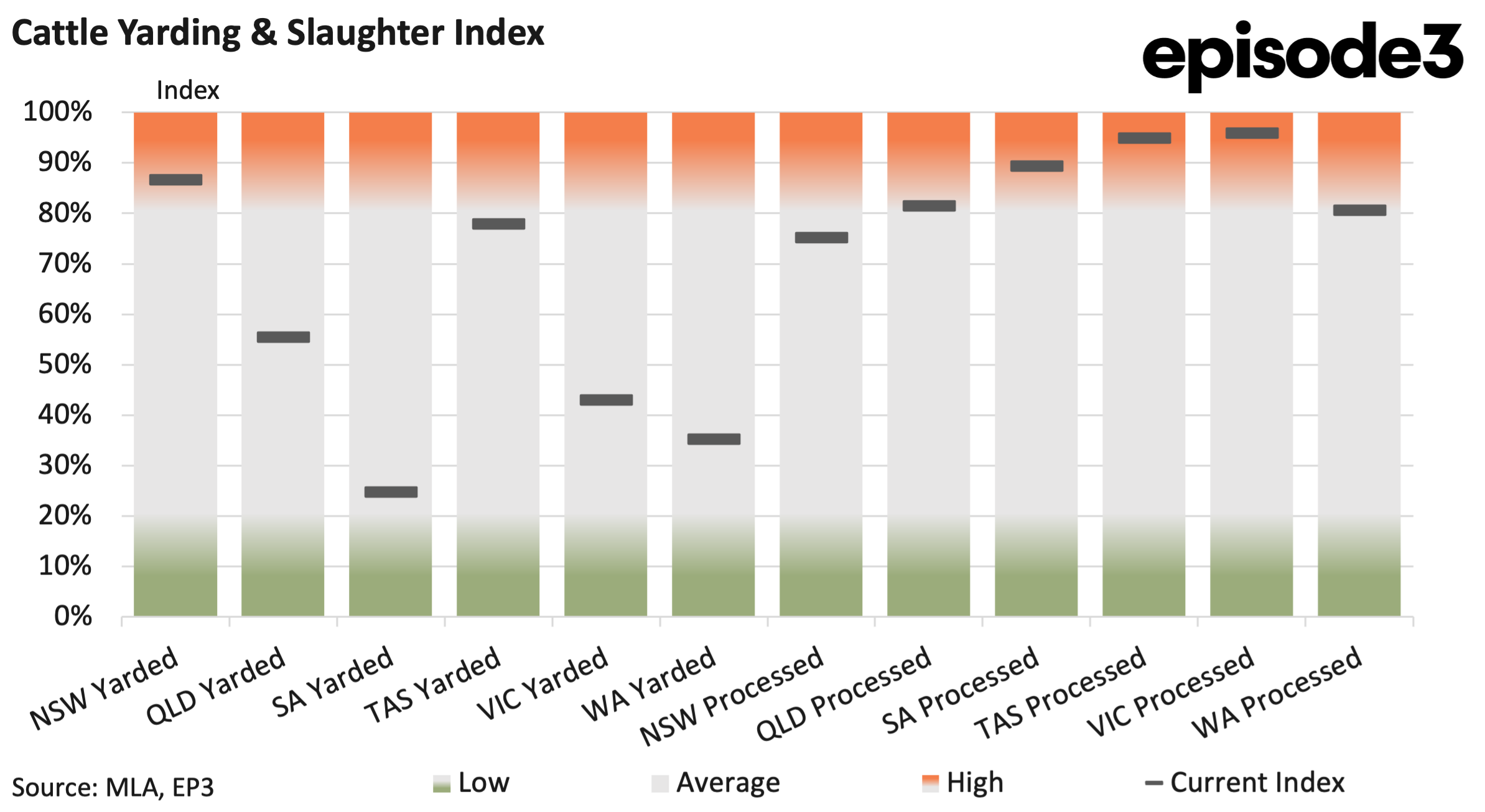

New South Wales processing activity lifted from 48pc to 75pc and Queensland increased from 57pc to 81pc. South Australia rose from 67pc to 89pc, meanwhile Tasmania surged from 57pc to 95pc. Victoria climbed from 60pc to 96pc, while Western Australia improved from 68pc to 81pc.

The consistency of these increases across every state confirms that the sharp decline recorded in April was largely the result of shortened Easter operating weeks rather than a collapse in processor demand. With plants returning to normal operating schedules, throughput has rebounded strongly. However, the supply side is telling a different story.

Yarding levels eased across the major eastern cattle producing states during May. New South Wales declined from 93pc to 87pc and Queensland fell from 69pc to 55pc. South Australia slipped from 36pc to 25pc, while at the same time, Victoria, Tasmania and Western Australia all recorded improvements. Victoria lifted from 37pc to 43pc, Tasmania increased from 69pc to 78pc and Western Australia rose from 25pc to 35pc.

The overall picture is one of tightening supply in the larger eastern cattle producing regions, partially offset by improved availability elsewhere. This is a very different scenario to the one that existed through March and April when rising cattle availability was putting widespread pressure on prices.

The latest MLA indicators suggest the market has responded accordingly. Processor cow prices have increased by 57 cents over the past four weeks and

heavy steer prices have lifted by 11 cents. These moves point to a change in market sentiment. Only a month ago the conversation centred on growing supply, weaker prices and processors regaining leverage. The latest data suggests that dynamic has reversed.

Rainfall across many key cattle producing areas has played an important role. Improved seasonal conditions have reduced the urgency for producers to market stock and increased confidence among restockers. The result has been fewer cattle coming forward while processors have returned to higher operating levels.

That combination tends to create competition and the May figures suggest exactly that has occurred. The shift in market conditions highlights how quickly cattle markets can change when supply and seasonal factors move together. Only a few weeks ago the market appeared to be loosening. Today the indicators point to tightening availability and stronger buyer competition.

That does not necessarily mean the broader supply outlook has fundamentally changed. National cattle numbers remain significantly larger than they were several years ago and slaughter rates are still running at elevated levels.

What has changed is the willingness of producers to sell cattle today versus holding them for tomorrow. The processing sector now finds itself operating in a very different environment to the one that existed during March and April. Plants have returned to high operating rates, but cattle are becoming harder to source in some of the key producing regions.

The May 2026 Cattle Yarding and Slaughter Index data therefore points to a market that has tightened since April. Supply has not disappeared, but it has become less accessible. At the same time, processor demand has strengthened as normal operating conditions have returned. The result is a cattle market that has regained momentum.

Prices are moving higher, competition has intensified, and the balance of power has shifted away from buyers and back towards producers. Whether that trend continues through winter will depend heavily on seasonal conditions and the willingness of producers to market cattle. For now, however, the May data shows a market that looks considerably tighter than it did just a month ago.